Advertisement

- India

- /

- Auto Components

- /

- NSEI:RICOAUTO

Rico Auto Industries (NSE:RICOAUTO) Hasn't Managed To Accelerate Its Returns

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. Although, when we looked at Rico Auto Industries (NSE:RICOAUTO), it didn't seem to tick all of these boxes.

Return On Capital Employed (ROCE): What Is It?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. To calculate this metric for Rico Auto Industries, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.093 = ₹920m ÷ (₹20b - ₹10b) (Based on the trailing twelve months to September 2022).

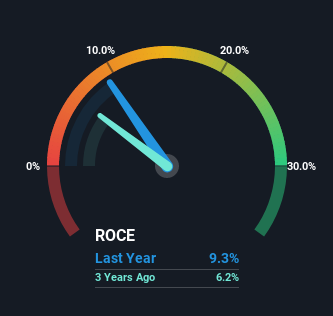

Thus, Rico Auto Industries has an ROCE of 9.3%. In absolute terms, that's a low return and it also under-performs the Auto Components industry average of 13%.

Check out our latest analysis for Rico Auto Industries

Historical performance is a great place to start when researching a stock so above you can see the gauge for Rico Auto Industries' ROCE against it's prior returns. If you want to delve into the historical earnings, revenue and cash flow of Rico Auto Industries, check out these free graphs here.

What Does the ROCE Trend For Rico Auto Industries Tell Us?

There are better returns on capital out there than what we're seeing at Rico Auto Industries. The company has employed 56% more capital in the last five years, and the returns on that capital have remained stable at 9.3%. Given the company has increased the amount of capital employed, it appears the investments that have been made simply don't provide a high return on capital.

On another note, while the change in ROCE trend might not scream for attention, it's interesting that the current liabilities have actually gone up over the last five years. This is intriguing because if current liabilities hadn't increased to 50% of total assets, this reported ROCE would probably be less than9.3% because total capital employed would be higher.The 9.3% ROCE could be even lower if current liabilities weren't 50% of total assets, because the the formula would show a larger base of total capital employed. Additionally, this high level of current liabilities isn't ideal because it means the company's suppliers (or short-term creditors) are effectively funding a large portion of the business.

Our Take On Rico Auto Industries' ROCE

In summary, Rico Auto Industries has simply been reinvesting capital and generating the same low rate of return as before. And investors appear hesitant that the trends will pick up because the stock has fallen 19% in the last five years. On the whole, we aren't too inspired by the underlying trends and we think there may be better chances of finding a multi-bagger elsewhere.

One more thing: We've identified 3 warning signs with Rico Auto Industries (at least 2 which are potentially serious) , and understanding them would certainly be useful.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:RICOAUTO

Rico Auto Industries

An engineering company, manufactures and supplies high precision fully machined aluminum, and ferrous components and assemblies to original equipment manufacturers worldwide.

Proven track record second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor