Advertisement

- India

- /

- Auto Components

- /

- NSEI:NDRAUTO

NDR Auto Components (NSE:NDRAUTO) Might Have The Makings Of A Multi-Bagger

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. So on that note, NDR Auto Components (NSE:NDRAUTO) looks quite promising in regards to its trends of return on capital.

What Is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for NDR Auto Components, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.084 = ₹196m ÷ (₹3.1b - ₹745m) (Based on the trailing twelve months to December 2022).

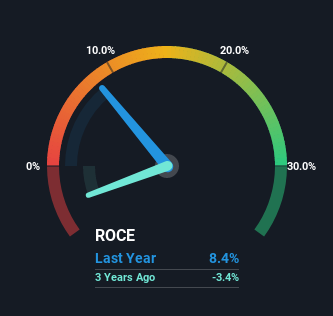

Therefore, NDR Auto Components has an ROCE of 8.4%. Ultimately, that's a low return and it under-performs the Auto Components industry average of 14%.

Check out our latest analysis for NDR Auto Components

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating NDR Auto Components' past further, check out this free graph of past earnings, revenue and cash flow.

What The Trend Of ROCE Can Tell Us

We're delighted to see that NDR Auto Components is reaping rewards from its investments and is now generating some pre-tax profits. Shareholders would no doubt be pleased with this because the business was loss-making three years ago but is is now generating 8.4% on its capital. In addition to that, NDR Auto Components is employing 39% more capital than previously which is expected of a company that's trying to break into profitability. This can tell us that the company has plenty of reinvestment opportunities that are able to generate higher returns.

For the record though, there was a noticeable increase in the company's current liabilities over the period, so we would attribute some of the ROCE growth to that. The current liabilities has increased to 24% of total assets, so the business is now more funded by the likes of its suppliers or short-term creditors. It's worth keeping an eye on this because as the percentage of current liabilities to total assets increases, some aspects of risk also increase.

Our Take On NDR Auto Components' ROCE

Long story short, we're delighted to see that NDR Auto Components' reinvestment activities have paid off and the company is now profitable. Since the stock has returned a solid 71% to shareholders over the last year, it's fair to say investors are beginning to recognize these changes. In light of that, we think it's worth looking further into this stock because if NDR Auto Components can keep these trends up, it could have a bright future ahead.

If you'd like to know about the risks facing NDR Auto Components, we've discovered 2 warning signs that you should be aware of.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

Valuation is complex, but we're here to simplify it.

Discover if NDR Auto Components might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:NDRAUTO

NDR Auto Components

Manufactures, fabricates, assembles, sells, and trades in automotive components for passenger cars and utility vehicles in India.

Flawless balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor