Advertisement

- India

- /

- Auto Components

- /

- NSEI:JTEKTINDIA

These 4 Measures Indicate That JTEKT India (NSE:JTEKTINDIA) Is Using Debt Reasonably Well

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that JTEKT India Limited (NSE:JTEKTINDIA) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for JTEKT India

How Much Debt Does JTEKT India Carry?

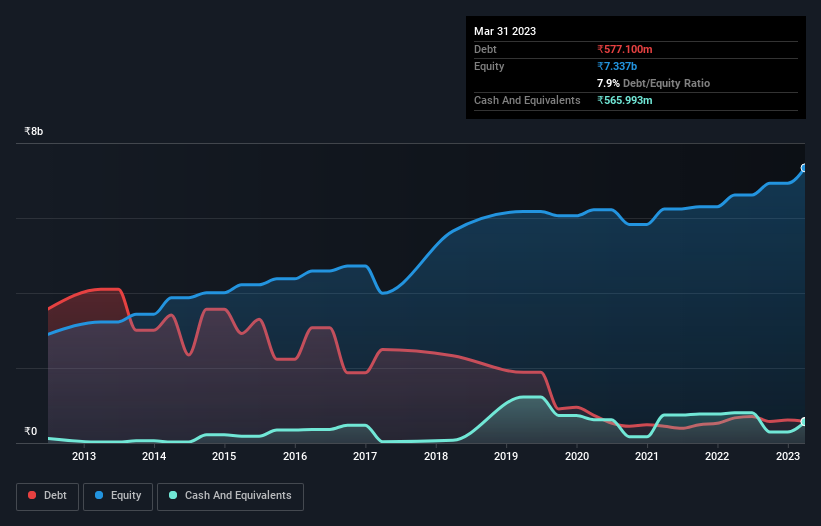

As you can see below, JTEKT India had ₹577.1m of debt at March 2023, down from ₹669.9m a year prior. However, it also had ₹566.0m in cash, and so its net debt is ₹11.1m.

How Healthy Is JTEKT India's Balance Sheet?

We can see from the most recent balance sheet that JTEKT India had liabilities of ₹2.95b falling due within a year, and liabilities of ₹451.3m due beyond that. Offsetting these obligations, it had cash of ₹566.0m as well as receivables valued at ₹2.82b due within 12 months. So its total liabilities are just about perfectly matched by its shorter-term, liquid assets.

Having regard to JTEKT India's size, it seems that its liquid assets are well balanced with its total liabilities. So it's very unlikely that the ₹33.9b company is short on cash, but still worth keeping an eye on the balance sheet. Carrying virtually no net debt, JTEKT India has a very light debt load indeed.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

JTEKT India has very little debt (net of cash), and boasts a debt to EBITDA ratio of 0.0057 and EBIT of 25.8 times the interest expense. Indeed relative to its earnings its debt load seems light as a feather. Better yet, JTEKT India grew its EBIT by 116% last year, which is an impressive improvement. If maintained that growth will make the debt even more manageable in the years ahead. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine JTEKT India's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, JTEKT India created free cash flow amounting to 19% of its EBIT, an uninspiring performance. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Our View

JTEKT India's interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. But truth be told we feel its conversion of EBIT to free cash flow does undermine this impression a bit. Looking at the bigger picture, we think JTEKT India's use of debt seems quite reasonable and we're not concerned about it. After all, sensible leverage can boost returns on equity. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of JTEKT India's earnings per share history for free.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:JTEKTINDIA

JTEKT India

Engages in the manufacture and sale of steering systems and auto components for the passenger car and utility vehicle manufacturers in the automobile sector in India.

Excellent balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor