Advertisement

- India

- /

- Auto Components

- /

- NSEI:JTEKTINDIA

Earnings Update: Here's Why Analysts Just Lifted Their JTEKT India Limited (NSE:JTEKTINDIA) Price Target To ₹192

Shareholders might have noticed that JTEKT India Limited (NSE:JTEKTINDIA) filed its quarterly result this time last week. The early response was not positive, with shares down 3.3% to ₹150 in the past week. It was a workmanlike result, with revenues of ₹5.8b coming in 2.3% ahead of expectations, and statutory earnings per share of ₹3.33, in line with analyst appraisals. The analyst typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We thought readers would find it interesting to see the analyst latest (statutory) post-earnings forecasts for next year.

Check out our latest analysis for JTEKT India

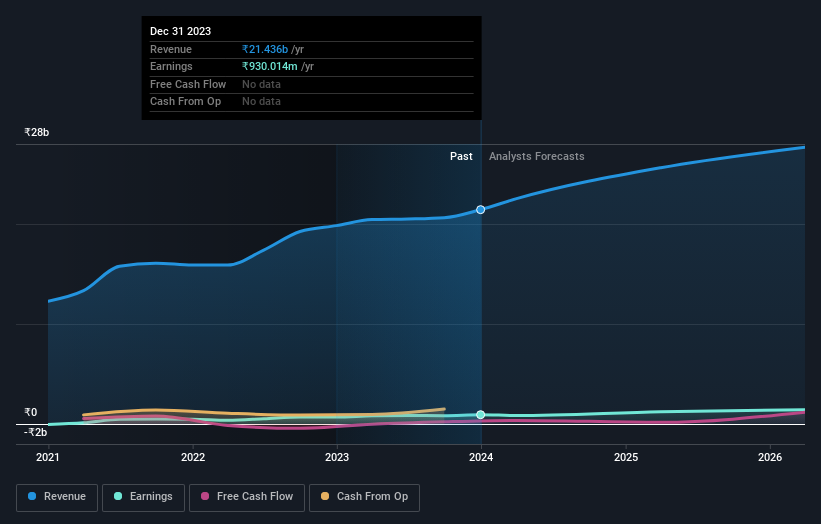

Taking into account the latest results, the most recent consensus for JTEKT India from solitary analyst is for revenues of ₹22.5b in 2024. If met, it would imply a credible 5.1% increase on its revenue over the past 12 months. Statutory earnings per share are forecast to decrease 4.3% to ₹3.50 in the same period. In the lead-up to this report, the analyst had been modelling revenues of ₹23.6b and earnings per share (EPS) of ₹3.80 in 2024. It's pretty clear that pessimism has reared its head after the latest results, leading to a weaker revenue outlook and a small dip in earnings per share estimates.

What's most unexpected is that the consensus price target rose 17% to ₹192, strongly implying the downgrade to forecasts is not expected to be more than a temporary blip.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. It's clear from the latest estimates that JTEKT India's rate of growth is expected to accelerate meaningfully, with the forecast 11% annualised revenue growth to the end of 2024 noticeably faster than its historical growth of 7.7% p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 11% annually. JTEKT India is expected to grow at about the same rate as its industry, so it's not clear that we can draw any conclusions from its growth relative to competitors.

The Bottom Line

The biggest concern is that the analyst reduced their earnings per share estimates, suggesting business headwinds could lay ahead for JTEKT India. Sadly, they also downgraded their revenue forecasts, but the business is still expected to grow at roughly the same rate as the industry itself. We note an upgrade to the price target, suggesting that the analyst believes the intrinsic value of the business is likely to improve over time.

With that in mind, we wouldn't be too quick to come to a conclusion on JTEKT India. Long-term earnings power is much more important than next year's profits. We have analyst estimates for JTEKT India going out as far as 2026, and you can see them free on our platform here.

However, before you get too enthused, we've discovered 2 warning signs for JTEKT India that you should be aware of.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:JTEKTINDIA

JTEKT India

Engages in the manufacture and sale of steering systems and auto components for the passenger car and utility vehicle manufacturers in the automobile sector in India.

Excellent balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.8% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|22.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.8% overvalued

LI

Community Contributor