Advertisement

- India

- /

- Auto Components

- /

- NSEI:ASAL

Automotive Stampings and Assemblies Limited (NSE:ASAL) Soars 34% But It's A Story Of Risk Vs Reward

Despite an already strong run, Automotive Stampings and Assemblies Limited (NSE:ASAL) shares have been powering on, with a gain of 34% in the last thirty days. The last month tops off a massive increase of 180% in the last year.

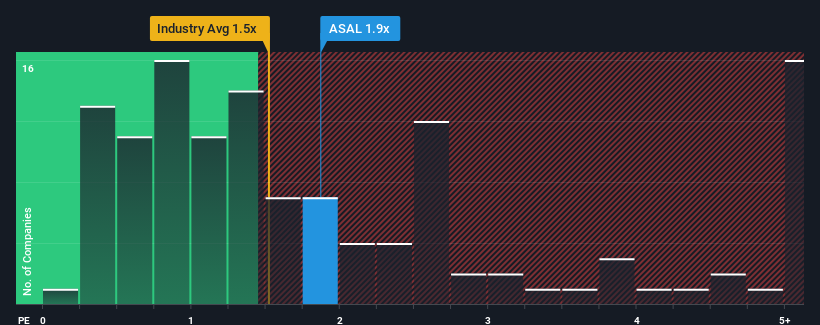

Even after such a large jump in price, you could still be forgiven for feeling indifferent about Automotive Stampings and Assemblies' P/S ratio of 1.9x, since the median price-to-sales (or "P/S") ratio for the Auto Components industry in India is also close to 1.5x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

See our latest analysis for Automotive Stampings and Assemblies

What Does Automotive Stampings and Assemblies' P/S Mean For Shareholders?

The recent revenue growth at Automotive Stampings and Assemblies would have to be considered satisfactory if not spectacular. One possibility is that the P/S is moderate because investors think this good revenue growth might only be parallel to the broader industry in the near future. If not, then at least existing shareholders probably aren't too pessimistic about the future direction of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Automotive Stampings and Assemblies will help you shine a light on its historical performance.What Are Revenue Growth Metrics Telling Us About The P/S?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Automotive Stampings and Assemblies' to be considered reasonable.

If we review the last year of revenue growth, the company posted a worthy increase of 6.3%. This was backed up an excellent period prior to see revenue up by 160% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenues over that time.

Comparing that recent medium-term revenue trajectory with the industry's one-year growth forecast of 11% shows it's noticeably more attractive.

With this information, we find it interesting that Automotive Stampings and Assemblies is trading at a fairly similar P/S compared to the industry. Apparently some shareholders believe the recent performance is at its limits and have been accepting lower selling prices.

The Final Word

Automotive Stampings and Assemblies appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

To our surprise, Automotive Stampings and Assemblies revealed its three-year revenue trends aren't contributing to its P/S as much as we would have predicted, given they look better than current industry expectations. There could be some unobserved threats to revenue preventing the P/S ratio from matching this positive performance. It appears some are indeed anticipating revenue instability, because the persistence of these recent medium-term conditions would normally provide a boost to the share price.

You should always think about risks. Case in point, we've spotted 3 warning signs for Automotive Stampings and Assemblies you should be aware of, and 2 of them make us uncomfortable.

If you're unsure about the strength of Automotive Stampings and Assemblies' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:ASAL

Automotive Stampings and Assemblies

Designs, develops, manufactures, assembles, and sells sheet metal stampings, welded assemblies, and modules for passenger and commercial vehicles, and tractors in India.

Low risk with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor