Advertisement

- Israel

- /

- Telecom Services and Carriers

- /

- TASE:BEZQ

Bezeq (TASE:BEZQ): Assessing Valuation After Profitability Jumps in Latest Quarterly Results

Simply Wall St

Reviewed by Simply Wall St

Bezeq The Israel Telecommunication (TASE:BEZQ) released its third quarter results, revealing a year-over-year decline in sales but a notable jump in net income and earnings per share. This shift points to enhanced profitability and has caught investors’ attention.

See our latest analysis for Bezeq The Israel Telecommunication.

Bezeq’s shares have held steady near ₪6.50, but investors have been rewarded far beyond recent headlines, with a one-year total shareholder return of nearly 34% and a strong 120% gain over five years. Momentum appears to be building as profitability improves, which is drawing even more attention from the market.

If improved earnings and strong returns have you thinking bigger, now is a great time to broaden your investing horizons and discover fast growing stocks with high insider ownership

With Bezeq’s share price trading below analyst targets and profitability climbing, is the recent rally just the beginning, or is the market already factoring in all the growth ahead?

Price-to-Earnings of 13x: Is it justified?

Bezeq is currently priced at a price-to-earnings (P/E) ratio of 13 times earnings, a figure that stands out against peers and hints at relative undervaluation. With the latest closing price at ₪6.50, the stock appears attractively valued by this popular metric.

The P/E ratio compares a company's share price to its per-share earnings, offering investors an easy way to gauge how much they are paying for a slice of recent profits. For Bezeq, this number is notably lower than the peer average. This suggests investors might be underappreciating the company's earnings potential given its recent surge in profitability.

Compared to both the industry average of 16.9x and broader market benchmarks, Bezeq’s P/E presents a compelling value. Investors are currently paying less for each unit of Bezeq’s earnings than they would for most competitors. This could mean the company's improved performance and earnings growth profile are being underestimated.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 13x (UNDERVALUED)

However, investors should note that slowing revenue growth or shifts in industry competition could quickly alter Bezeq’s current valuation picture.

Find out about the key risks to this Bezeq The Israel Telecommunication narrative.

Another Perspective: Discounted Cash Flow

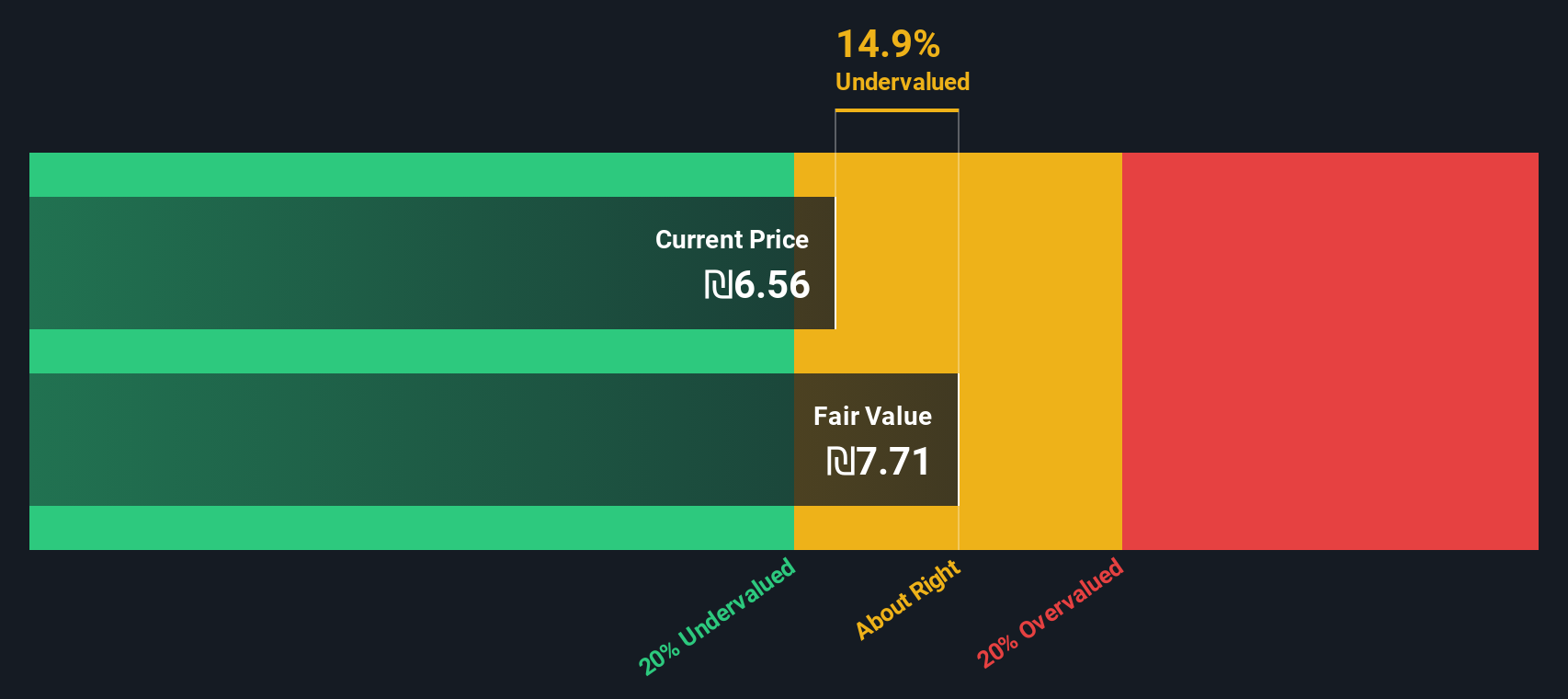

While Bezeq’s price-to-earnings ratio suggests the stock is undervalued compared to peers, our SWS DCF model also finds the company is trading around 28% below its fair value estimate of ₪9.02. This alternative view reinforces the earlier undervaluation signal. However, the question remains: will the market bridge this gap?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Bezeq The Israel Telecommunication for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 870 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Bezeq The Israel Telecommunication Narrative

If you want to take a different view or put your own research to the test, it only takes a few minutes to shape your own perspective and Do it your way.

A great starting point for your Bezeq The Israel Telecommunication research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Take charge of your portfolio by uncovering stocks with untapped potential, dynamic growth, or steady returns using Simply Wall Street’s free screeners.

- Capture value by targeting these 870 undervalued stocks based on cash flows that the market may be overlooking. This may give you a shot at greater upside.

- Tap into game-changing medical innovation with these 31 healthcare AI stocks, which is transforming how healthcare is delivered and advancing patient care.

- Boost your portfolio’s income stream by selecting these 15 dividend stocks with yields > 3% offering attractive yields above 3% for consistent cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bezeq The Israel Telecommunication might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TASE:BEZQ

Bezeq The Israel Telecommunication

Provides communications services to business and private customers in Israel.

Solid track record and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor