Advertisement

- Israel

- /

- Electronic Equipment and Components

- /

- TASE:TEDE

Tedea Technological Development and Automation (TLV:TEDE) Shareholders Will Want The ROCE Trajectory To Continue

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. Speaking of which, we noticed some great changes in Tedea Technological Development and Automation's (TLV:TEDE) returns on capital, so let's have a look.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for Tedea Technological Development and Automation:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

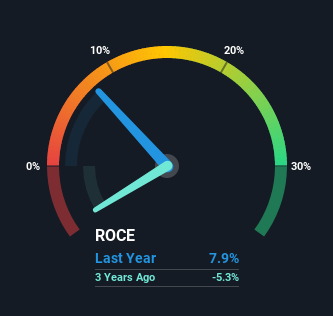

0.079 = ₪4.7m ÷ (₪115m - ₪56m) (Based on the trailing twelve months to December 2020).

Thus, Tedea Technological Development and Automation has an ROCE of 7.9%. Ultimately, that's a low return and it under-performs the Electronic industry average of 11%.

View our latest analysis for Tedea Technological Development and Automation

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you want to delve into the historical earnings, revenue and cash flow of Tedea Technological Development and Automation, check out these free graphs here.

What The Trend Of ROCE Can Tell Us

Like most people, we're pleased that Tedea Technological Development and Automation is now generating some pretax earnings. The company was generating losses five years ago, but now it's turned around, earning 7.9% which is no doubt a relief for some early shareholders. At first glance, it seems the business is getting more proficient at generating returns, because over the same period, the amount of capital employed has reduced by 46%. The reduction could indicate that the company is selling some assets, and considering returns are up, they appear to be selling the right ones.

For the record though, there was a noticeable increase in the company's current liabilities over the period, so we would attribute some of the ROCE growth to that. Essentially the business now has suppliers or short-term creditors funding about 48% of its operations, which isn't ideal. And with current liabilities at those levels, that's pretty high.

The Key Takeaway

In the end, Tedea Technological Development and Automation has proven it's capital allocation skills are good with those higher returns from less amount of capital. And a remarkable 134% total return over the last five years tells us that investors are expecting more good things to come in the future. Therefore, we think it would be worth your time to check if these trends are going to continue.

One more thing, we've spotted 2 warning signs facing Tedea Technological Development and Automation that you might find interesting.

While Tedea Technological Development and Automation may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Tedea Technological Development and Automation might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TASE:TEDE

Tedea Technological Development and Automation

Through its subsidiaries, manufactures, imports, markets, and sells building products in Israel.

Moderate risk with worrying balance sheet.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Optimi Health ·

The Only Psychedelic Company Already Selling MDMA and Psilocybin to Real Patients, Yet Priced Like It Doesn’t Exist

Fair Value:US$1156.8% undervalued

34 followersusers have followed this narrative

2 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7721.5% undervalued

54 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9219.7% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$19010.1% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

ES

Esteban on Mastercard ·

Capital-light, high-return payment network that is successfully expanding into high-margin security and data services faster than its peers.

Fair Value:US$395.534.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JM

JM7 on Soluna Holdings ·

Soluna: Powering Renewable AI, Funding the Risk

Fair Value:US$985.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on RENOVA ·

Empowering the future with “new energy”

Fair Value:JP¥690.0941.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.8% undervalued

70 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.919.1% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23038.1% overvalued

90 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative