Advertisement

We're Interested To See How Photomyne (TLV:PHTM) Uses Its Cash Hoard To Grow

Just because a business does not make any money, does not mean that the stock will go down. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

So, the natural question for Photomyne (TLV:PHTM) shareholders is whether they should be concerned by its rate of cash burn. In this report, we will consider the company's annual negative free cash flow, henceforth referring to it as the 'cash burn'. The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

View our latest analysis for Photomyne

How Long Is Photomyne's Cash Runway?

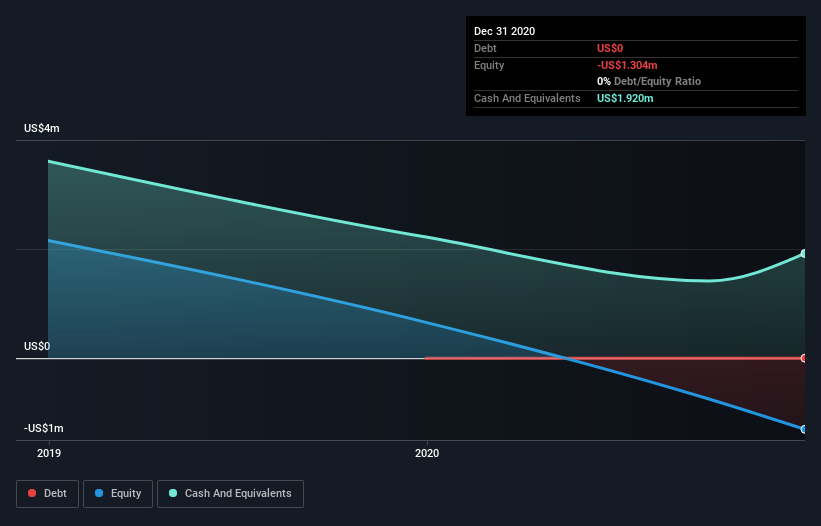

A company's cash runway is calculated by dividing its cash hoard by its cash burn. As at December 2020, Photomyne had cash of US$1.9m and no debt. In the last year, its cash burn was US$188k. That means it had a cash runway of very many years as of December 2020. While this is only one measure of its cash burn situation, it certainly gives us the impression that holders have nothing to worry about. You can see how its cash balance has changed over time in the image below.

How Well Is Photomyne Growing?

Photomyne managed to reduce its cash burn by 86% over the last twelve months, which is extremely promising, when it comes to considering its need for cash. Pleasingly, this was achieved with the help of a 43% boost to revenue. Considering these factors, we're fairly impressed by its growth trajectory. Of course, we've only taken a quick look at the stock's growth metrics, here. You can take a look at how Photomyne is growing revenue over time by checking this visualization of past revenue growth.

How Hard Would It Be For Photomyne To Raise More Cash For Growth?

We are certainly impressed with the progress Photomyne has made over the last year, but it is also worth considering how costly it would be if it wanted to raise more cash to fund faster growth. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

Photomyne's cash burn of US$188k is about 0.3% of its US$57m market capitalisation. That means it could easily issue a few shares to fund more growth, and might well be in a position to borrow cheaply.

Is Photomyne's Cash Burn A Worry?

It may already be apparent to you that we're relatively comfortable with the way Photomyne is burning through its cash. For example, we think its cash burn reduction suggests that the company is on a good path. And even its revenue growth was very encouraging. Looking at all the measures in this article, together, we're not worried about its rate of cash burn, which seems to be under control. Taking a deeper dive, we've spotted 3 warning signs for Photomyne you should be aware of, and 1 of them is significant.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies insiders are buying, and this list of stocks growth stocks (according to analyst forecasts)

When trading stocks or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TASE:PHTM

Flawless balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor