Advertisement

- Israel

- /

- Real Estate

- /

- TASE:BOTI

Improved Revenues Required Before Bonei Hatichon Civil Engineering & Infrastructures Ltd. (TLV:BOTI) Stock's 26% Jump Looks Justified

Bonei Hatichon Civil Engineering & Infrastructures Ltd. (TLV:BOTI) shareholders have had their patience rewarded with a 26% share price jump in the last month. The last 30 days bring the annual gain to a very sharp 53%.

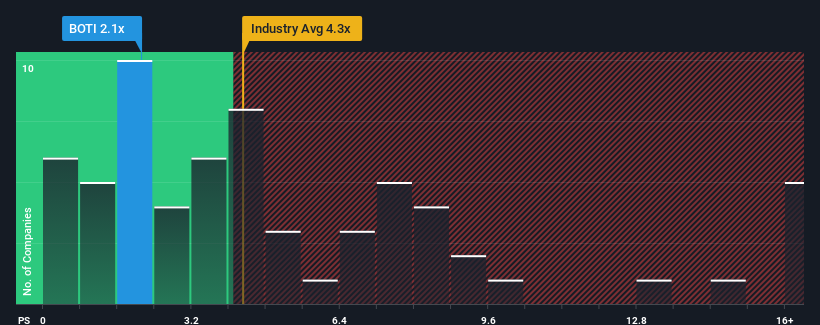

Although its price has surged higher, Bonei Hatichon Civil Engineering & Infrastructures may still look like a strong buying opportunity at present with its price-to-sales (or "P/S") ratio of 2.1x, considering almost half of all companies in the Real Estate industry in Israel have P/S ratios greater than 4.3x and even P/S higher than 8x aren't out of the ordinary. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

See our latest analysis for Bonei Hatichon Civil Engineering & Infrastructures

What Does Bonei Hatichon Civil Engineering & Infrastructures' P/S Mean For Shareholders?

For example, consider that Bonei Hatichon Civil Engineering & Infrastructures' financial performance has been poor lately as its revenue has been in decline. Perhaps the market believes the recent revenue performance isn't good enough to keep up the industry, causing the P/S ratio to suffer. Those who are bullish on Bonei Hatichon Civil Engineering & Infrastructures will be hoping that this isn't the case so that they can pick up the stock at a lower valuation.

Although there are no analyst estimates available for Bonei Hatichon Civil Engineering & Infrastructures, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Do Revenue Forecasts Match The Low P/S Ratio?

Bonei Hatichon Civil Engineering & Infrastructures' P/S ratio would be typical for a company that's expected to deliver very poor growth or even falling revenue, and importantly, perform much worse than the industry.

Retrospectively, the last year delivered a frustrating 6.1% decrease to the company's top line. This means it has also seen a slide in revenue over the longer-term as revenue is down 36% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

In contrast to the company, the rest of the industry is expected to grow by 54% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

In light of this, it's understandable that Bonei Hatichon Civil Engineering & Infrastructures' P/S would sit below the majority of other companies. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. Even just maintaining these prices could be difficult to achieve as recent revenue trends are already weighing down the shares.

The Bottom Line On Bonei Hatichon Civil Engineering & Infrastructures' P/S

Even after such a strong price move, Bonei Hatichon Civil Engineering & Infrastructures' P/S still trails the rest of the industry. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Bonei Hatichon Civil Engineering & Infrastructures revealed its shrinking revenue over the medium-term is contributing to its low P/S, given the industry is set to grow. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises either. Given the current circumstances, it seems unlikely that the share price will experience any significant movement in either direction in the near future if recent medium-term revenue trends persist.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Bonei Hatichon Civil Engineering & Infrastructures (at least 1 which makes us a bit uncomfortable), and understanding them should be part of your investment process.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Bonei Hatichon Civil Engineering & Infrastructures might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TASE:BOTI

Bonei Hatichon Civil Engineering & Infrastructures

Bonei Hatichon Civil Engineering & Infrastructures Ltd.

Slightly overvalued with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor