Advertisement

- Israel

- /

- Oil and Gas

- /

- TASE:ORL

Oil Refineries (TASE:ORL) Returns to Profit in Q3, Dividend Coverage Concerns Persist

Simply Wall St

Reviewed by Simply Wall St

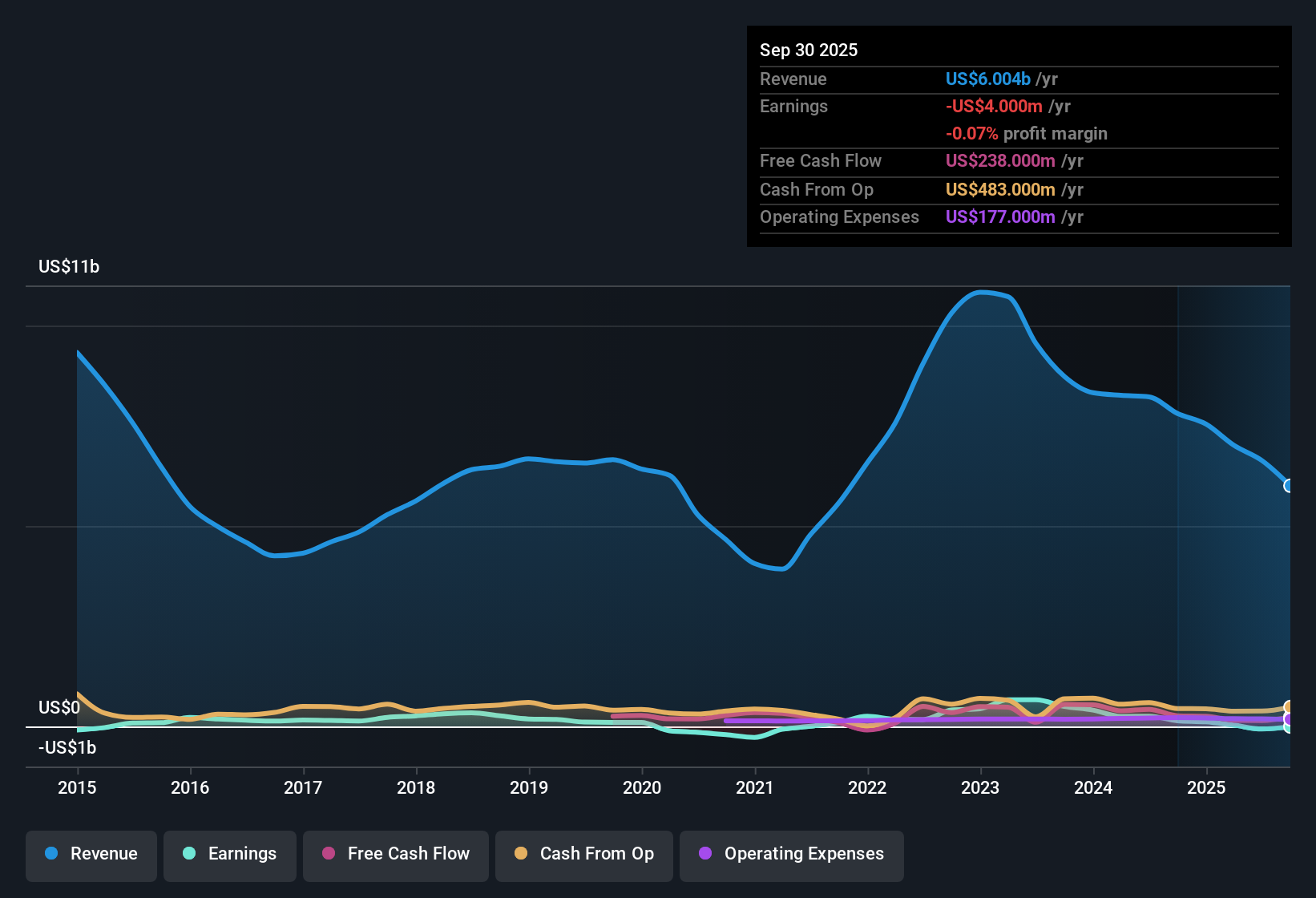

Oil Refineries (TASE:ORL) has just released its Q3 2025 financials, reporting revenue of $1.2 billion and net income of $46 million, with basic EPS coming in at $0.015. Looking back, the company has seen quarterly revenue shift from $1.85 billion in Q2 2024 to $1.47 billion in Q2 2025, while EPS moved from $0.02 to -$0.012 over the same timeline. Unprofitable on a trailing twelve month basis, ORL’s profit margins remain under pressure, keeping investors focused on what is driving the numbers beneath the surface.

See our full analysis for Oil Refineries.Let’s put these latest results next to the current market narratives to see how the headlines compare with the stories investors are telling.

Curious how numbers become stories that shape markets? Explore Community Narratives

Losses Shrink, But Profitability Elusive

- Trailing twelve-month net income stands at -$4 million, a significant narrowing compared to -$65 million from just one quarter earlier. However, the company remains unprofitable overall.

- Even with a lower net loss over time, the current negative profit margin challenges the idea that diversification into chemicals, fuels, and infrastructure guarantees steady cash flow.

- Despite revenue reach of $6.0 billion over the last twelve months, earnings have not turned positive, testing claims of “defensive” resilience emphasized in market analysis.

- Declining losses at a 15% annual rate suggest gradual improvement. Still, with no return to consistent profitability, bulls face lingering doubts about a turnaround.

High Dividend Yield Faces Coverage Risk

- ORL’s 8.36% dividend yield outpaces industry norms, but recent earnings have not covered payouts. This poses a sustainability risk that should not be ignored.

- Bears often question whether such a high yield can persist when the company posts negative trailing net income.

- Dividend concerns become more pressing as cash flows fluctuate, especially with net income staying negative across the latest twelve months.

- Payment of a rich dividend may appeal to yield-seekers, but it creates tension with prudent capital management if profits stay under pressure.

Trading Deep Below DCF Fair Value

- Shares are currently trading at $1.00, a steep 69.1% discount to the DCF fair value of $3.24. This positions ORL as one of the more deeply discounted names relative to both peers and the sector average price-to-sales ratio.

- Prevailing market view holds that such a low Price-to-Sales ratio, at 0.2x versus the industry’s 0.8x, could be a double-edged sword. It signals strong valuation appeal but may also reflect persistent doubts about earnings recovery.

- Compared to an industry average P/S of 0.8x and a peer average of 2.6x, ORL’s market value builds in a margin of safety for value-focused investors. However, the absence of positive profit trends keeps many on the sidelines.

- The share price’s distance from DCF-based valuation draws attention to future catalysts. Unless profitability returns, this discount may persist longer than the bulls hope.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Oil Refineries's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Persistently negative trailing net income and inconsistent profit trends raise real concerns about the sustainability of Oil Refineries’ high dividend payouts.

If you want confidence your future income is backed by robust earnings, check out these 1940 dividend stocks with yields > 3% to find companies offering attractive yields that are actually covered by profits.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TASE:ORL

Oil Refineries

Produces and sells fuel products, intermediate materials, and aromatic products in Israel and internationally.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

FA

FAI on Arabian Internet and Communication Services ·

Solutions by stc: 34% Upside in Saudi's Digital Transformation Leader

Fair Value:ر.س342.2335.5% undervalued

10 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

RO

RobertoAllende on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.9% undervalued

28 followersusers have followed this narrative

28 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Recently Updated Narratives

TA

Talos on NVIDIA ·

Not a Bubble, But the "Industrial Revolution 4.0" Engine

Fair Value:US$294.9239.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Advanced Micro Devices ·

The "David vs. Goliath" AI Trade – Why Second Place is Worth Billions

Fair Value:US$416.4647.2% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on PayPal Holdings ·

The "Sleeping Giant" Wakes Up – Efficiency & Monetization

Fair Value:US$174.9264.2% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

111 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.1% undervalued

945 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.4% undervalued

146 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative