Bank Leumi le-Israel B.M (TASE:LUMI) has delivered a 7% revenue increase over the past year, catching investors’ attention. The stock is also up nearly 10% in the past month, and this continues a strong upward trend.

Building on this momentum, Bank Leumi le-Israel B.M’s share price has gained an impressive 9.5% over the past month, with a year-to-date share price return of nearly 58%. Long-term investors have seen even greater rewards, as the total shareholder return has soared more than 330% over five years. This reflects consistent performance and growing confidence in the bank’s outlook.

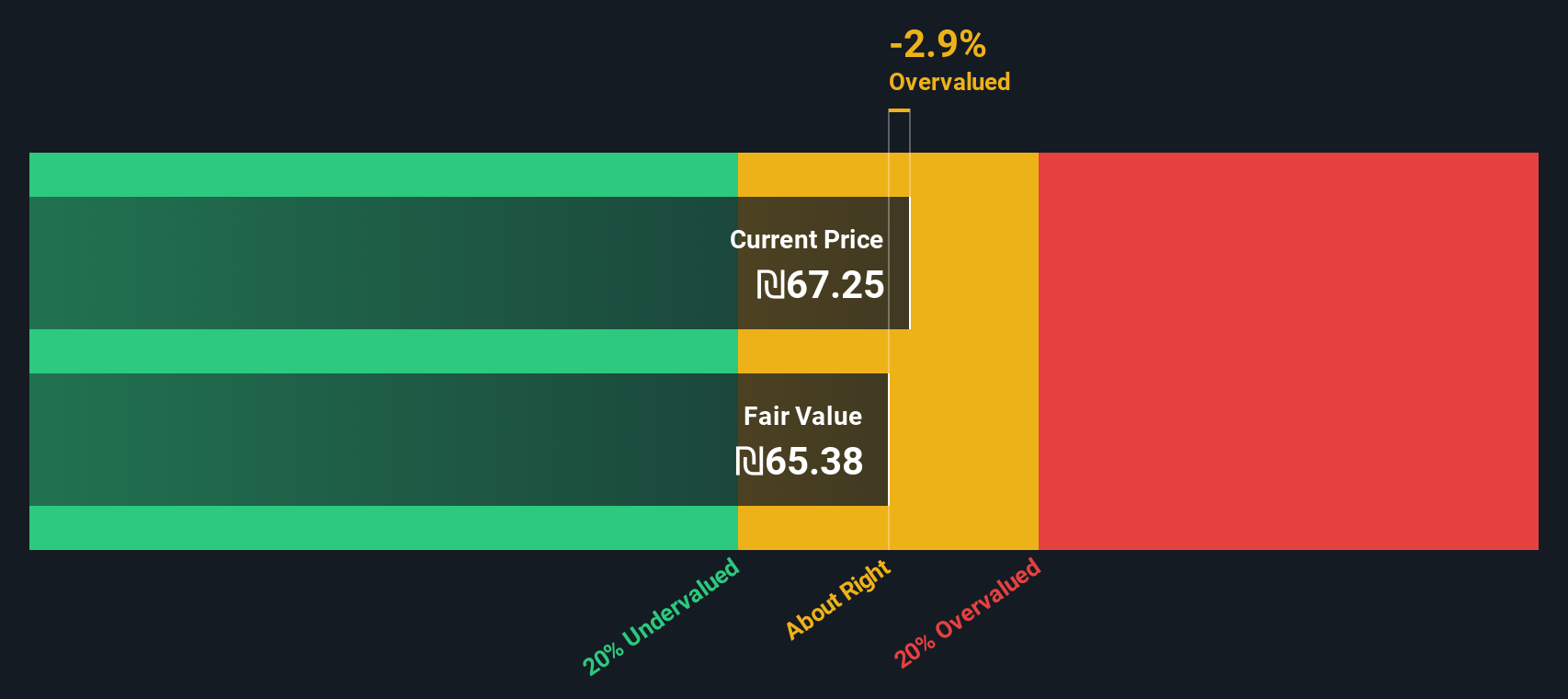

With shares still trading at a modest discount to analyst price targets, the key question for investors is whether Bank Leumi le-Israel B.M is genuinely undervalued, or if the market has already taken its impressive growth prospects into account.

Advertisement

Price-to-Earnings of 10.1x: Is it justified?

Bank Leumi le-Israel B.M is trading at a price-to-earnings (P/E) ratio of 10.1x. This means investors are paying 10.1 times the company's earnings per share to own a stake at the last close price of ₪69.15. This is a widely used measure to determine whether a company's shares are expensive or attractively priced relative to its earnings.

The P/E ratio is especially relevant for banks like Leumi, since it captures how the market values the profit-generating power of its core business. A higher multiple can suggest optimism about future growth or profitability, while a lower multiple may point to concerns about earnings sustainability or sector headwinds.

Currently, Leumi's P/E of 10.1x is higher than the Asian Banks industry average of 9.3x. This signals the market is assigning a premium to Leumi over regional peers, potentially reflecting recent growth momentum and robust earnings quality. In contrast, against its peer average of 10.3x, Leumi appears modestly priced.

While Bank Leumi le-Israel B.M currently looks pricey based on its price-to-earnings ratio, our DCF model tells a different story. According to the SWS DCF model, the shares are trading about 9.5% below our fair value estimate. This suggests some upside could still be on the table. Can the fundamentals back this up, or is it just market optimism?

If you have a different perspective, or would rather dig into the numbers yourself, you can build your own analysis in just minutes. Do it your way

A great starting point for your Bank Leumi le-Israel B.M research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Take your strategy to the next level by tapping into powerful stock picks that others might miss. Give yourself every advantage before your next big move.

Spot the latest tech breakthroughs and position yourself early by targeting these 25 AI penny stocks, which are creating waves in artificial intelligence innovation and automation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bank Leumi le-Israel B.M might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Provides banking and financial services for households, small and medium enterprises, and corporations in Israel, the United Kingdom, and internationally.