- Hong Kong

- /

- Gas Utilities

- /

- SEHK:3

The Hong Kong and China Gas Company Limited (HKG:3): What Can We Expect In The Future?

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

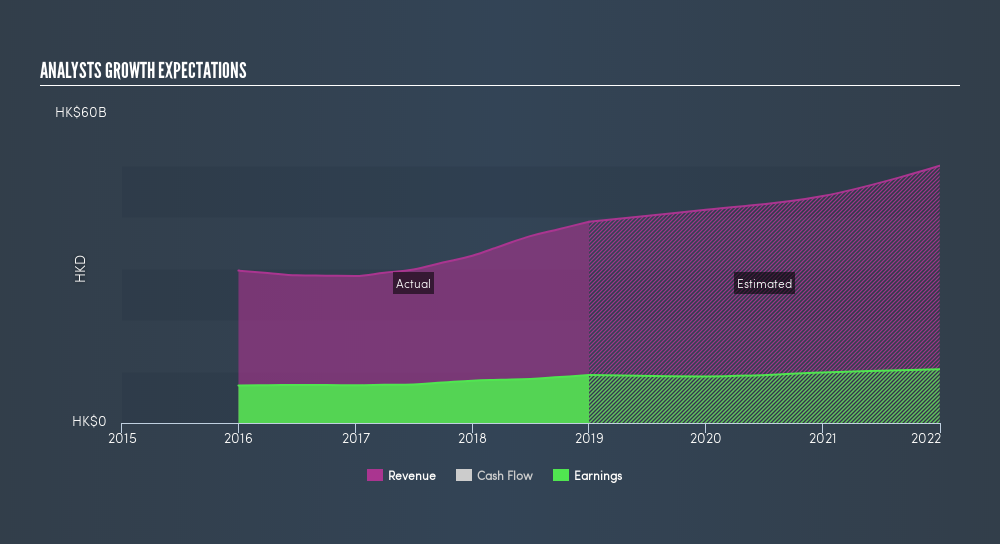

Based on The Hong Kong and China Gas Company Limited's (HKG:3) recently announced earnings update on 31 December 2018, the consensus outlook from analysts appear pessimistic, as a -2.9% fall in profits is expected in the upcoming year compared with the past 5-year average growth rate of 4.8%. Presently, with latest-twelve-month earnings at HK$9.3b, we should see this fall to HK$9.0b by 2020. I will provide a brief commentary around the figures and analyst expectations in the near term. For those interested in more of an analysis of the company, you can research its fundamentals here.

Check out our latest analysis for Hong Kong and China Gas

How will Hong Kong and China Gas perform in the near future?

The longer term expectations from the 11 analysts of 3 is tilted towards the positive sentiment. Generally, broker analysts tend to make predictions for up to three years given the lack of visibility beyond this point. I've plotted out each year's earnings expectations and inserted a line of best fit to calculate an annual growth rate from the slope in order to understand the overall trajectory of 3's earnings growth over these next few years.

From the current net income level of HK$9.3b and the final forecast of HK$10b by 2022, the annual rate of growth for 3’s earnings is 4.1%. EPS reaches HK$0.68 in the final year of forecast compared to the current HK$0.61 EPS today. As revenues is expected to outpace earnings, analysts expect margins to contract from the current 24% to 21% by the end of 2022.

Next Steps:

Future outlook is only one aspect when you're building an investment case for a stock. For Hong Kong and China Gas, there are three relevant aspects you should look at:

- Financial Health: Does it have a healthy balance sheet? Take a look at our free balance sheet analysis with six simple checks on key factors like leverage and risk.

- Valuation: What is Hong Kong and China Gas worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether Hong Kong and China Gas is currently mispriced by the market.

- Other High-Growth Alternatives : Are there other high-growth stocks you could be holding instead of Hong Kong and China Gas? Explore our interactive list of stocks with large growth potential to get an idea of what else is out there you may be missing!

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About SEHK:3

Hong Kong and China Gas

Produces, distributes, and markets gas, water supply and energy services in Hong Kong and Mainland China.

Proven track record second-rate dividend payer.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Meta’s Bold Bet on AI Pays Off

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Visa Stock: The Toll Booth at the Center of Global Commerce

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion