Advertisement

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Tianjin Tianbao Energy Co., Ltd. (HKG:1671) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Tianjin Tianbao Energy

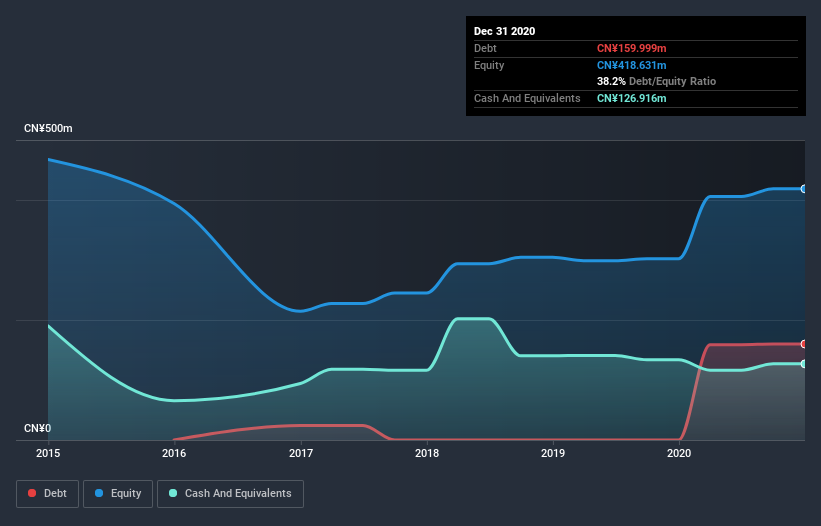

What Is Tianjin Tianbao Energy's Debt?

The image below, which you can click on for greater detail, shows that at December 2020 Tianjin Tianbao Energy had debt of CN¥160.0m, up from none in one year. However, it does have CN¥126.9m in cash offsetting this, leading to net debt of about CN¥33.1m.

A Look At Tianjin Tianbao Energy's Liabilities

We can see from the most recent balance sheet that Tianjin Tianbao Energy had liabilities of CN¥276.4m falling due within a year, and liabilities of CN¥115.2m due beyond that. Offsetting this, it had CN¥126.9m in cash and CN¥39.7m in receivables that were due within 12 months. So it has liabilities totalling CN¥225.0m more than its cash and near-term receivables, combined.

When you consider that this deficiency exceeds the company's CN¥161.6m market capitalization, you might well be inclined to review the balance sheet intently. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While Tianjin Tianbao Energy's low debt to EBITDA ratio of 0.44 suggests only modest use of debt, the fact that EBIT only covered the interest expense by 4.4 times last year does give us pause. But the interest payments are certainly sufficient to have us thinking about how affordable its debt is. Notably, Tianjin Tianbao Energy's EBIT launched higher than Elon Musk, gaining a whopping 156% on last year. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Tianjin Tianbao Energy will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the most recent three years, Tianjin Tianbao Energy recorded free cash flow worth 52% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

Tianjin Tianbao Energy's EBIT growth rate was a real positive on this analysis, as was its net debt to EBITDA. But truth be told its level of total liabilities had us nibbling our nails. It's also worth noting that Tianjin Tianbao Energy is in the Electric Utilities industry, which is often considered to be quite defensive. When we consider all the factors mentioned above, we do feel a bit cautious about Tianjin Tianbao Energy's use of debt. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 4 warning signs for Tianjin Tianbao Energy (of which 1 is a bit concerning!) you should know about.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you’re looking to trade Tianjin Tianbao Energy, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Tianjin Tianbao Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1671

Tianjin Tianbao Energy

Generates and supplies power in the People's Republic of China.

Proven track record with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|8.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.6% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor