Advertisement

- Hong Kong

- /

- Infrastructure

- /

- SEHK:576

Zhejiang Expressway Co., Ltd. (HKG:576) On An Uptrend: Could Fundamentals Be Driving The Stock?

Most readers would already know that Zhejiang Expressway's (HKG:576) stock increased by 7.9% over the past three months. Given that stock prices are usually aligned with a company's financial performance in the long-term, we decided to investigate if the company's decent financials had a hand to play in the recent price move. Specifically, we decided to study Zhejiang Expressway's ROE in this article.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

See our latest analysis for Zhejiang Expressway

How To Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Zhejiang Expressway is:

9.1% = CN¥3.3b ÷ CN¥36b (Based on the trailing twelve months to September 2020).

The 'return' is the amount earned after tax over the last twelve months. That means that for every HK$1 worth of shareholders' equity, the company generated HK$0.09 in profit.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

A Side By Side comparison of Zhejiang Expressway's Earnings Growth And 9.1% ROE

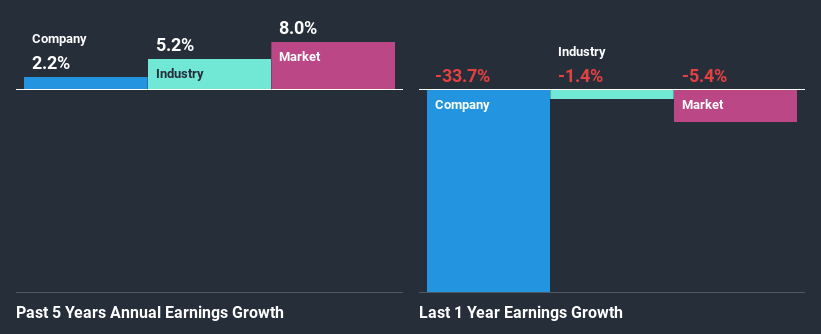

On the face of it, Zhejiang Expressway's ROE is not much to talk about. However, the fact that the company's ROE is higher than the average industry ROE of 5.7%, is definitely interesting. Still, Zhejiang Expressway's net income growth of 2.2% over the past five years was mediocre at best. Remember, the company's ROE is quite low to begin with, just that it is higher than the industry average. Therefore, the low growth in earnings could also be the result of this.

Next, on comparing with the industry net income growth, we found that Zhejiang Expressway's reported growth was lower than the industry growth of 5.2% in the same period, which is not something we like to see.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. Is Zhejiang Expressway fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Zhejiang Expressway Using Its Retained Earnings Effectively?

Despite having a normal three-year median payout ratio of 46% (or a retention ratio of 54% over the past three years, Zhejiang Expressway has seen very little growth in earnings as we saw above. So there might be other factors at play here which could potentially be hampering growth. For example, the business has faced some headwinds.

Additionally, Zhejiang Expressway has paid dividends over a period of at least ten years, which means that the company's management is determined to pay dividends even if it means little to no earnings growth. Upon studying the latest analysts' consensus data, we found that the company is expected to keep paying out approximately 38% of its profits over the next three years. However, Zhejiang Expressway's ROE is predicted to rise to 16% despite there being no anticipated change in its payout ratio.

Summary

Overall, we feel that Zhejiang Expressway certainly does have some positive factors to consider. However, while the company does have a decent ROE and a high profit retention, its earnings growth number is quite disappointing. This suggests that there might be some external threat to the business, that's hampering growth. With that said, the latest industry analyst forecasts reveal that the company's earnings are expected to accelerate. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

If you’re looking to trade Zhejiang Expressway, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Expressway might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About SEHK:576

Zhejiang Expressway

An investment holding company, invests, develops, maintains, and operates roads in the People’s Republic of China.

Excellent balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.8% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|22.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.8% overvalued

LI

Community Contributor