Advertisement

- Hong Kong

- /

- Transportation

- /

- SEHK:306

Kwoon Chung Bus Holdings' (HKG:306) Upcoming Dividend Will Be Larger Than Last Year's

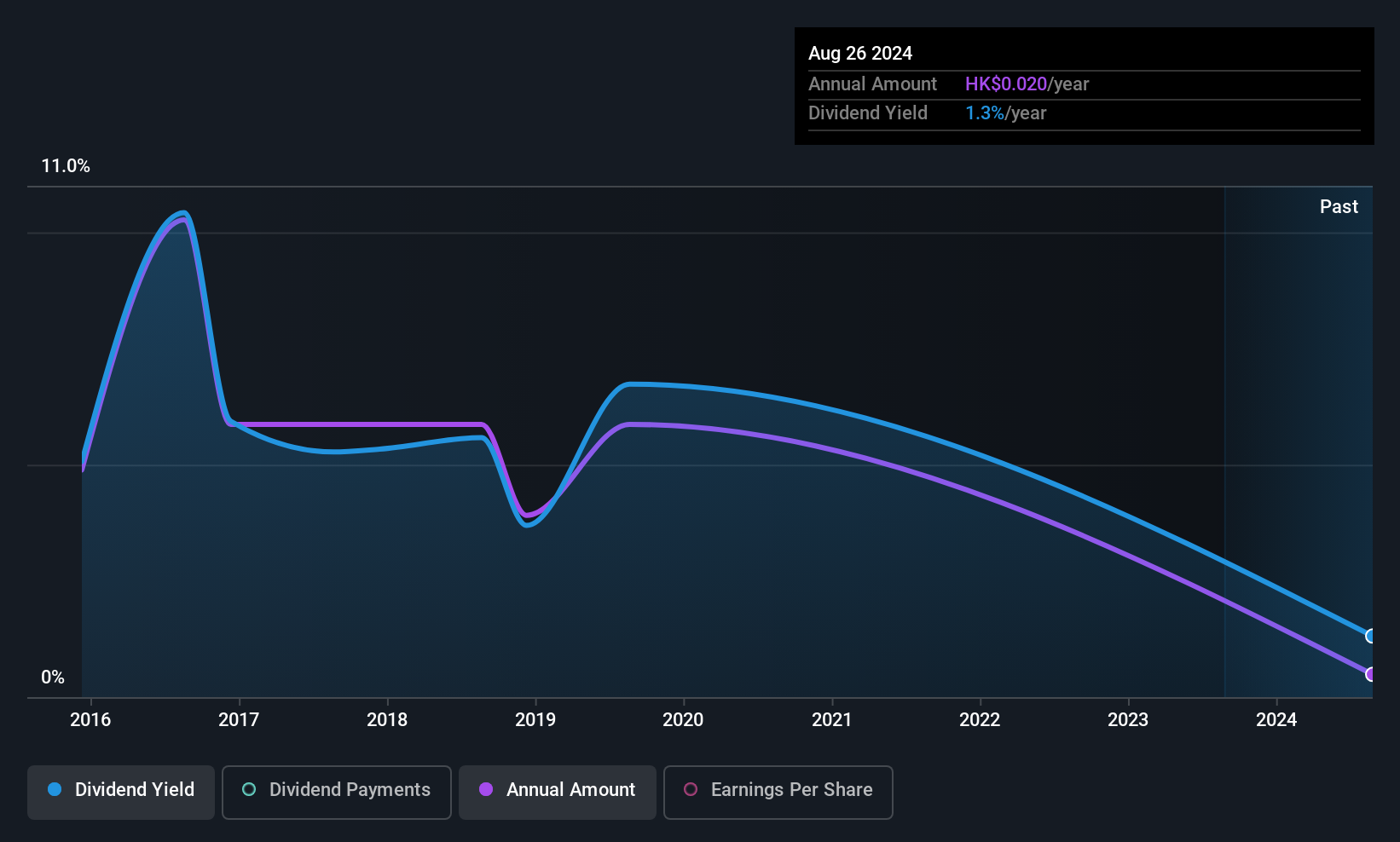

Kwoon Chung Bus Holdings Limited (HKG:306) will increase its dividend from last year's comparable payment on the 15th of September to HK$0.04. Even though the dividend went up, the yield is still quite low at only 1.7%.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that Kwoon Chung Bus Holdings' stock price has increased by 68% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

Kwoon Chung Bus Holdings' Projected Earnings Seem Likely To Cover Future Distributions

While yield is important, another factor to consider about a company's dividend is whether the current payout levels are feasible. However, Kwoon Chung Bus Holdings' earnings easily cover the dividend. This means that most of what the business earns is being used to help it grow.

If the trend of the last few years continues, EPS will grow by 44.1% over the next 12 months. If the dividend continues along recent trends, we estimate the payout ratio will be 9.1%, which is in the range that makes us comfortable with the sustainability of the dividend.

Check out our latest analysis for Kwoon Chung Bus Holdings

Dividend Volatility

While the company has been paying a dividend for a long time, it has cut the dividend at least once in the last 10 years. The dividend has gone from an annual total of HK$0.20 in 2015 to the most recent total annual payment of HK$0.04. The dividend has fallen 80% over that period. Generally, we don't like to see a dividend that has been declining over time as this can degrade shareholders' returns and indicate that the company may be running into problems.

The Dividend Looks Likely To Grow

Given that the track record hasn't been stellar, we really want to see earnings per share growing over time. Kwoon Chung Bus Holdings has impressed us by growing EPS at 44% per year over the past five years. Rapid earnings growth and a low payout ratio suggest this company has been effectively reinvesting in its business. Should that continue, this company could have a bright future.

Kwoon Chung Bus Holdings Looks Like A Great Dividend Stock

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. The company is easily earning enough to cover its dividend payments and it is great to see that these earnings are being translated into cash flow. All of these factors considered, we think this has solid potential as a dividend stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For example, we've identified 2 warning signs for Kwoon Chung Bus Holdings (1 is a bit unpleasant!) that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Kwoon Chung Bus Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:306

Kwoon Chung Bus Holdings

An investment holding company, provides bus and bus-related services in Hong Kong, Macau, and Mainland China.

Good value with proven track record.

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|50.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|8.5% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|18.4% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|51.6% overvalued

RO

Community Contributor