Advertisement

- Hong Kong

- /

- Marine and Shipping

- /

- SEHK:2343

What Can We Learn About Pacific Basin Shipping's (HKG:2343) CEO Compensation?

Mats Berglund became the CEO of Pacific Basin Shipping Limited (HKG:2343) in 2012, and we think it's a good time to look at the executive's compensation against the backdrop of overall company performance. This analysis will also evaluate the appropriateness of CEO compensation when taking into account the earnings and shareholder returns of the company.

Check out our latest analysis for Pacific Basin Shipping

How Does Total Compensation For Mats Berglund Compare With Other Companies In The Industry?

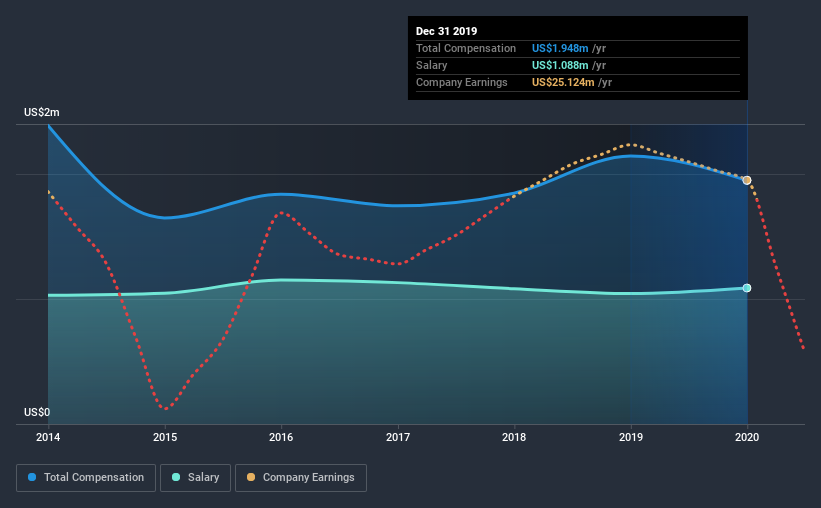

At the time of writing, our data shows that Pacific Basin Shipping Limited has a market capitalization of HK$5.9b, and reported total annual CEO compensation of US$1.9m for the year to December 2019. Notably, that's a decrease of 9.1% over the year before. Notably, the salary which is US$1.09m, represents most of the total compensation being paid.

For comparison, other companies in the same industry with market capitalizations ranging between HK$3.1b and HK$12b had a median total CEO compensation of US$1.0m. This suggests that Mats Berglund is paid more than the median for the industry. What's more, Mats Berglund holds HK$20m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2019 | 2018 | Proportion (2019) |

| Salary | US$1.1m | US$1.0m | 56% |

| Other | US$860k | US$1.1m | 44% |

| Total Compensation | US$1.9m | US$2.1m | 100% |

Talking in terms of the industry, salary represented approximately 85% of total compensation out of all the companies we analyzed, while other remuneration made up 15% of the pie. In Pacific Basin Shipping's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Pacific Basin Shipping Limited's Growth Numbers

Over the last three years, Pacific Basin Shipping Limited has shrunk its earnings per share by 40% per year. In the last year, its revenue is down 4.0%.

The decline in EPS is a bit concerning. This is compounded by the fact revenue is actually down on last year. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Pacific Basin Shipping Limited Been A Good Investment?

With a three year total loss of 28% for the shareholders, Pacific Basin Shipping Limited would certainly have some dissatisfied shareholders. So shareholders would probably want the company to be lessto generous with CEO compensation.

To Conclude...

As we noted earlier, Pacific Basin Shipping pays its CEO higher than the norm for similar-sized companies belonging to the same industry. Disappointingly, share price gains over the last three years have failed to materialize. To make matters worse, EPS growth has also been negative during this period. Understandably, the company's shareholders might have some questions about the CEO's remuneration, given the disappointing performance.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 1 warning sign for Pacific Basin Shipping that investors should think about before committing capital to this stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you’re looking to trade Pacific Basin Shipping, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About SEHK:2343

Pacific Basin Shipping

An investment holding company, engages in the provision of dry bulk shipping services in Hong Kong and internationally.

Flawless balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|24.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|13.5% overvalued

DA

Community Contributor