- Hong Kong

- /

- Electronic Equipment and Components

- /

- SEHK:2166

Smart-Core Holdings (HKG:2166) Has A Rock Solid Balance Sheet

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Smart-Core Holdings Limited (HKG:2166) makes use of debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Smart-Core Holdings

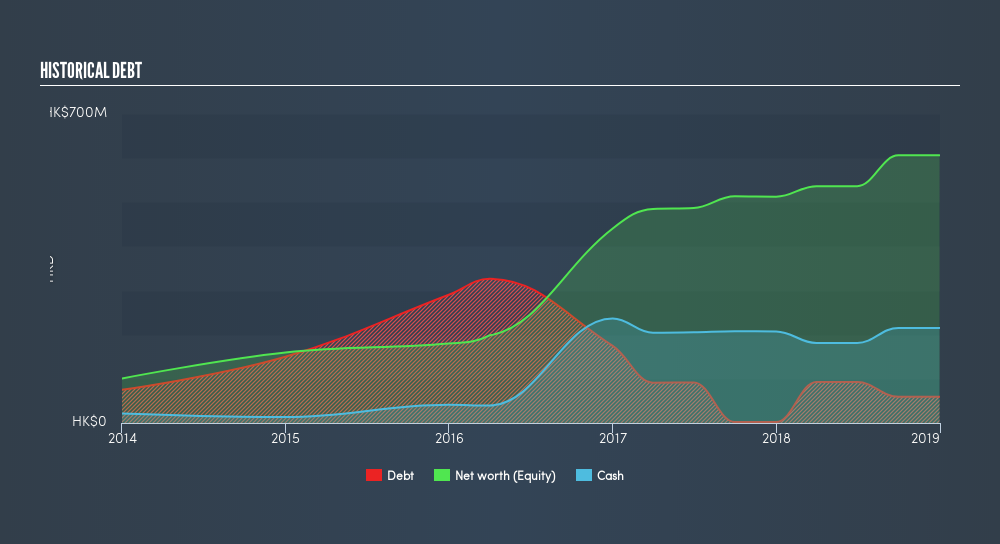

What Is Smart-Core Holdings's Debt?

The image below, which you can click on for greater detail, shows that at December 2018 Smart-Core Holdings had debt of HK$59.3m, up from HK$2.13m in one year. However, its balance sheet shows it holds HK$215.5m in cash, so it actually has HK$156.2m net cash.

How Healthy Is Smart-Core Holdings's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Smart-Core Holdings had liabilities of HK$584.2m due within 12 months and liabilities of HK$955.0k due beyond that. Offsetting these obligations, it had cash of HK$215.5m as well as receivables valued at HK$471.0m due within 12 months. So it can boast HK$101.3m more liquid assets than total liabilities.

It's good to see that Smart-Core Holdings has plenty of liquidity on its balance sheet, suggesting conservative management of liabilities. Because it has plenty of assets, it is unlikely to have trouble with its lenders. Simply put, the fact that Smart-Core Holdings has more cash than debt is arguably a good indication that it can manage its debt safely.

We note that Smart-Core Holdings grew its EBIT by 27% in the last year, and that should make it easier to pay down debt, going forward. When analysing debt levels, the balance sheet is the obvious place to start. But it is Smart-Core Holdings's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Smart-Core Holdings may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, Smart-Core Holdings actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that Smart-Core Holdings has net cash of HK$156m, as well as more liquid assets than liabilities. The cherry on top was that in converted 132% of that EBIT to free cash flow, bringing in HK$70m. So is Smart-Core Holdings's debt a risk? It doesn't seem so to us. Another factor that would give us confidence in Smart-Core Holdings would be if insiders have been buying shares: if you're conscious of that signal too, you can find out instantly by clicking this link.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About SEHK:2166

Smart-Core Holdings

An investment holding company, distributes integrated circuits and other electronic components in the Hong Kong, People’s Republic of China, Singapore, Japan, and internationally.

Slight risk and fair value.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion