Stock Analysis

- Hong Kong

- /

- Capital Markets

- /

- SEHK:6608

High Insider Ownership Growth Companies On SEHK With Earnings Growth Up To 73%

Reviewed by Simply Wall St

As global markets navigate through varying economic signals, with some regions showing signs of cooling while others maintain growth, investors are keenly watching for opportunities that align with these shifting dynamics. In Hong Kong, the SEHK has shown resilience amidst global uncertainties, making it a noteworthy arena for exploring growth companies with high insider ownership—a factor often linked to strong corporate governance and alignment of interests between shareholders and management.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

| Name | Insider Ownership | Earnings Growth |

| iDreamSky Technology Holdings (SEHK:1119) | 20.2% | 104.1% |

| Pacific Textiles Holdings (SEHK:1382) | 11.2% | 37.7% |

| Fenbi (SEHK:2469) | 32.8% | 43% |

| Tian Tu Capital (SEHK:1973) | 34% | 70.5% |

| Adicon Holdings (SEHK:9860) | 22.4% | 28.3% |

| Zhejiang Leapmotor Technology (SEHK:9863) | 15% | 73.4% |

| DPC Dash (SEHK:1405) | 38.2% | 90.2% |

| Beijing Airdoc Technology (SEHK:2251) | 28.7% | 83.9% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 13.9% | 100.1% |

| Ocumension Therapeutics (SEHK:1477) | 23.1% | 93.7% |

We'll examine a selection from our screener results.

Kingdee International Software Group (SEHK:268)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Kingdee International Software Group Company Limited operates as an investment holding company focused on enterprise resource planning software, with a market capitalization of approximately HK$27.61 billion.

Operations: The company's revenue is primarily derived from two segments: Cloud Service Business generating CN¥4.50 billion and ERP Business contributing CN¥1.17 billion.

Insider Ownership: 19.7%

Earnings Growth Forecast: 46.5% p.a.

Kingdee International Software Group, a notable entity in the Hong Kong software sector, recently initiated a share repurchase program, enhancing shareholder value through potential earnings per share increases. Despite past shareholder dilution and a low forecasted return on equity of 6.2%, Kingdee is trading at an 11.4% discount to its estimated fair value and shows promising growth prospects with expected earnings growth of 46.52% annually. Analyst consensus suggests a significant potential stock price increase of 76.9%.

- Unlock comprehensive insights into our analysis of Kingdee International Software Group stock in this growth report.

- In light of our recent valuation report, it seems possible that Kingdee International Software Group is trading behind its estimated value.

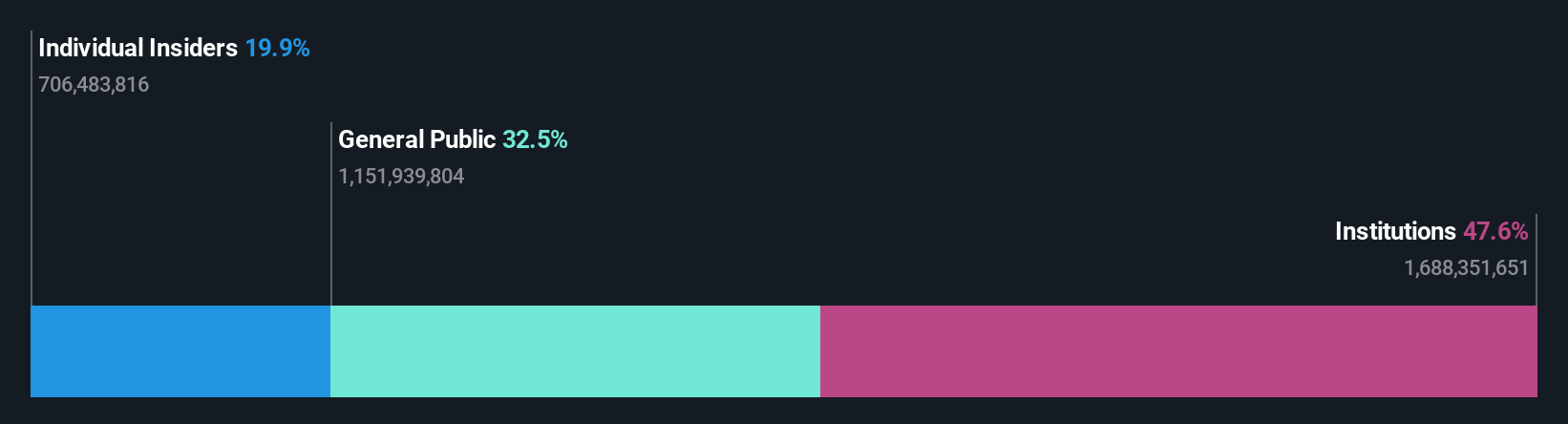

Bairong (SEHK:6608)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Bairong Inc. is a provider of cloud-based AI turnkey services in China, with a market capitalization of approximately HK$4.39 billion.

Operations: The company generates revenue primarily from data processing services, amounting to CN¥2.68 billion.

Insider Ownership: 19.1%

Earnings Growth Forecast: 21.1% p.a.

Bairong Inc. is experiencing robust earnings growth, with a 42.1% increase over the past year and an expected annual profit growth rate of 21.1%, outpacing the Hong Kong market average. Despite slower revenue growth forecasts at 15.8%, it remains above market expectations. The stock is currently valued at 41.1% below its estimated fair value, indicating potential for appreciation according to analysts who predict a substantial rise in stock price by 97.1%. Recent executive changes could influence operational efficiency and customer satisfaction positively.

- Take a closer look at Bairong's potential here in our earnings growth report.

- Insights from our recent valuation report point to the potential undervaluation of Bairong shares in the market.

China Youran Dairy Group (SEHK:9858)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: China Youran Dairy Group Limited operates in the upstream dairy industry in the People's Republic of China, with a market capitalization of approximately HK$4.55 billion.

Operations: The company generates revenue primarily through its Raw Milk Business, which brought in CN¥12.90 billion, and its Comprehensive Ruminant Farming Solutions segment, which contributed CN¥8.09 billion.

Insider Ownership: 14.5%

Earnings Growth Forecast: 73.8% p.a.

China Youran Dairy Group Limited is poised for significant earnings growth, with forecasts suggesting a 73.8% annual increase. Although its revenue growth of 8.4% per year is modest compared to some market leaders, it exceeds the Hong Kong market average of 7.7%. Recent leadership changes, including the appointment of Mr. Yuan Jun as Chairman and President, might streamline decision-making and strategic planning despite deviating from typical corporate governance norms. Analysts are optimistic about the stock's potential, expecting a price increase of 75.8%.

- Dive into the specifics of China Youran Dairy Group here with our thorough growth forecast report.

- Our expertly prepared valuation report China Youran Dairy Group implies its share price may be lower than expected.

Next Steps

- Unlock more gems! Our Fast Growing SEHK Companies With High Insider Ownership screener has unearthed 51 more companies for you to explore.Click here to unveil our expertly curated list of 54 Fast Growing SEHK Companies With High Insider Ownership.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Bairong might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:6608

Flawless balance sheet and undervalued.