Stock Analysis

Top 3 Stocks Estimated To Be Undervalued On SEHK In July 2024

Reviewed by Simply Wall St

As global markets navigate through a myriad of economic signals, the Hong Kong market has shown particular resilience amidst regional uncertainties. In July 2024, investors are increasingly turning their attention to value stocks, which may present opportunities for those looking for potentially undervalued assets on the SEHK. In this context, identifying stocks that appear undervalued involves assessing companies with solid fundamentals that are priced below their perceived intrinsic value—an approach that aligns well with current shifts towards more conservative investment strategies in volatile times.

Top 10 Undervalued Stocks Based On Cash Flows In Hong Kong

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Giant Biogene Holding (SEHK:2367) | HK$39.90 | HK$75.98 | 47.5% |

| China Resources Mixc Lifestyle Services (SEHK:1209) | HK$23.90 | HK$47.68 | 49.9% |

| China Cinda Asset Management (SEHK:1359) | HK$0.67 | HK$1.29 | 48.1% |

| Zijin Mining Group (SEHK:2899) | HK$16.32 | HK$32.34 | 49.5% |

| West China Cement (SEHK:2233) | HK$1.11 | HK$2.15 | 48.5% |

| Super Hi International Holding (SEHK:9658) | HK$13.34 | HK$25.84 | 48.4% |

| BYD (SEHK:1211) | HK$243.00 | HK$464.84 | 47.7% |

| Mobvista (SEHK:1860) | HK$2.01 | HK$3.74 | 46.3% |

| Vobile Group (SEHK:3738) | HK$1.24 | HK$2.31 | 46.4% |

| MicroPort Scientific (SEHK:853) | HK$5.20 | HK$9.53 | 45.4% |

We're going to check out a few of the best picks from our screener tool.

Innovent Biologics (SEHK:1801)

Overview: Innovent Biologics, Inc. is a biopharmaceutical company focused on developing and commercializing monoclonal antibodies and other drug assets for oncology, ophthalmology, autoimmune, and cardiovascular and metabolic diseases in China, with a market capitalization of approximately HK$66.03 billion.

Operations: Innovent Biologics generates revenue primarily from its biotechnology segment, totaling CN¥6.21 billion.

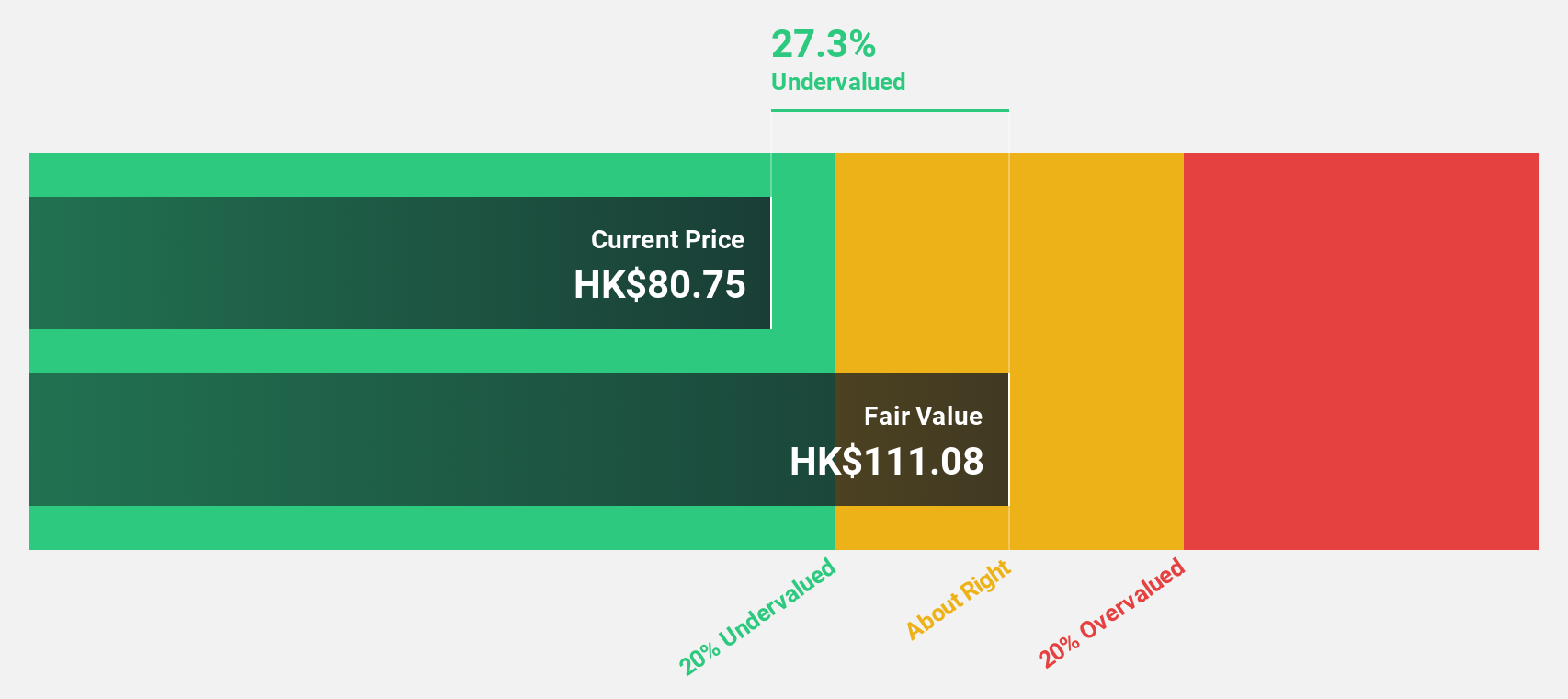

Estimated Discount To Fair Value: 34.6%

Innovent Biologics, a key player in the biopharmaceutical space in Hong Kong, appears undervalued based on its cash flows and recent strategic moves. The company's collaboration with IASO Bio enhances its position by divesting rights to FUCASO® while acquiring an 18% stake in IASO Bio, potentially boosting future cash inflows. Despite robust revenue growth forecasts (21.2% per year), Innovent trades at HK$40.55, significantly below the estimated fair value of HK$61.99, suggesting more than 20% undervaluation. Recent clinical advancements and strategic equity investments underscore its potential for improved financial health and market positioning.

- Our comprehensive growth report raises the possibility that Innovent Biologics is poised for substantial financial growth.

- Click to explore a detailed breakdown of our findings in Innovent Biologics' balance sheet health report.

Weimob (SEHK:2013)

Overview: Weimob Inc. is an investment holding company operating in the People's Republic of China, offering digital commerce and media services with a market capitalization of approximately HK$4.31 billion.

Operations: The company generates revenue primarily through Subscription Solutions (CN¥1.35 billion) and Merchant Solutions (CN¥878.28 million).

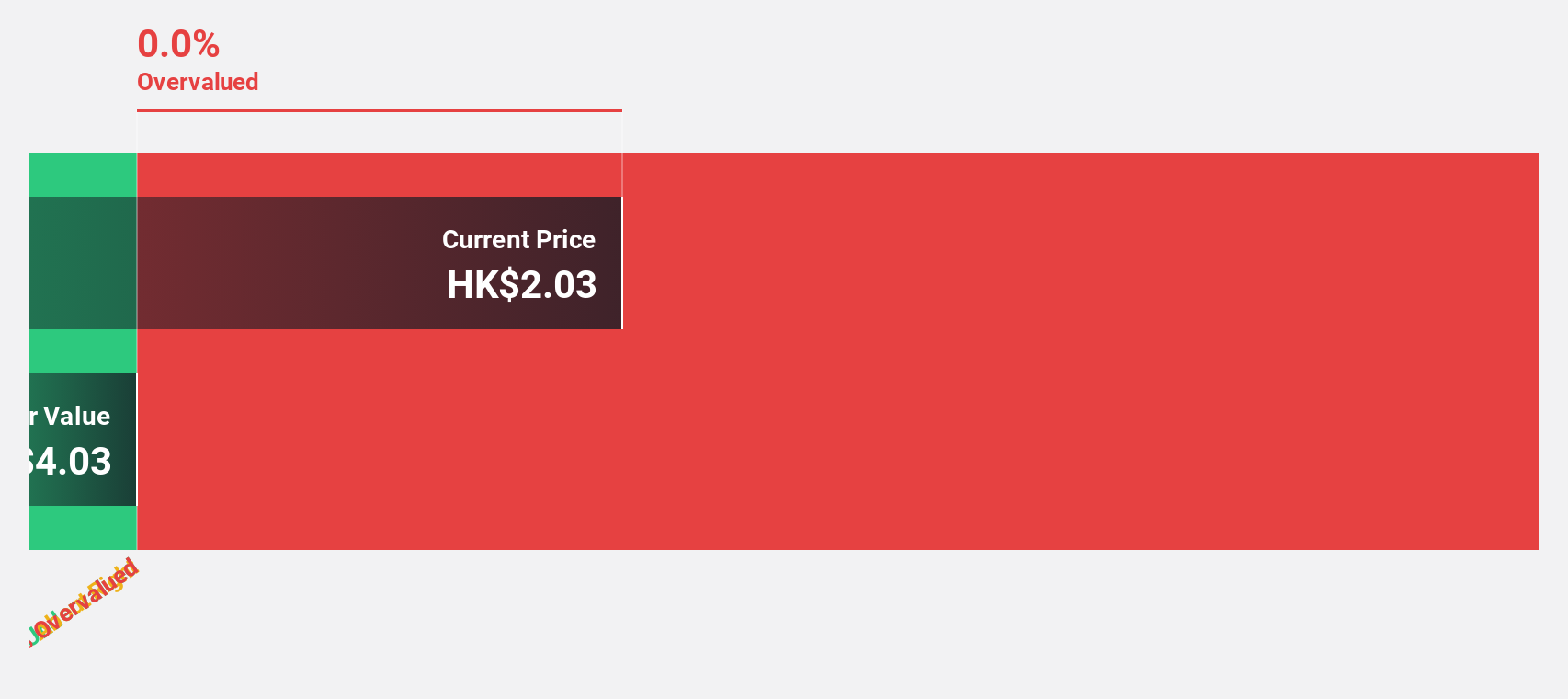

Estimated Discount To Fair Value: 30.5%

Weimob Inc., currently trading at HK$1.4, is considered highly undervalued based on discounted cash flow analysis, with a fair value estimated at HK$2.01. Despite recent shareholder dilution from a follow-on equity offering raising HK$313.01 million, the company is expected to become profitable within three years, showing promising growth forecasts in both revenue (12.2% per year) and earnings (109.92% per year). However, its forecasted Return on Equity remains low at 7.4%.

- Our growth report here indicates Weimob may be poised for an improving outlook.

- Click here to discover the nuances of Weimob with our detailed financial health report.

Pop Mart International Group (SEHK:9992)

Overview: Pop Mart International Group Limited is an investment holding company that specializes in the design, development, and sale of pop toys both in the People’s Republic of China and internationally, with a market capitalization of approximately HK$55.10 billion.

Operations: The company generates revenue primarily from the sale of designer toys, totaling CN¥6.30 billion.

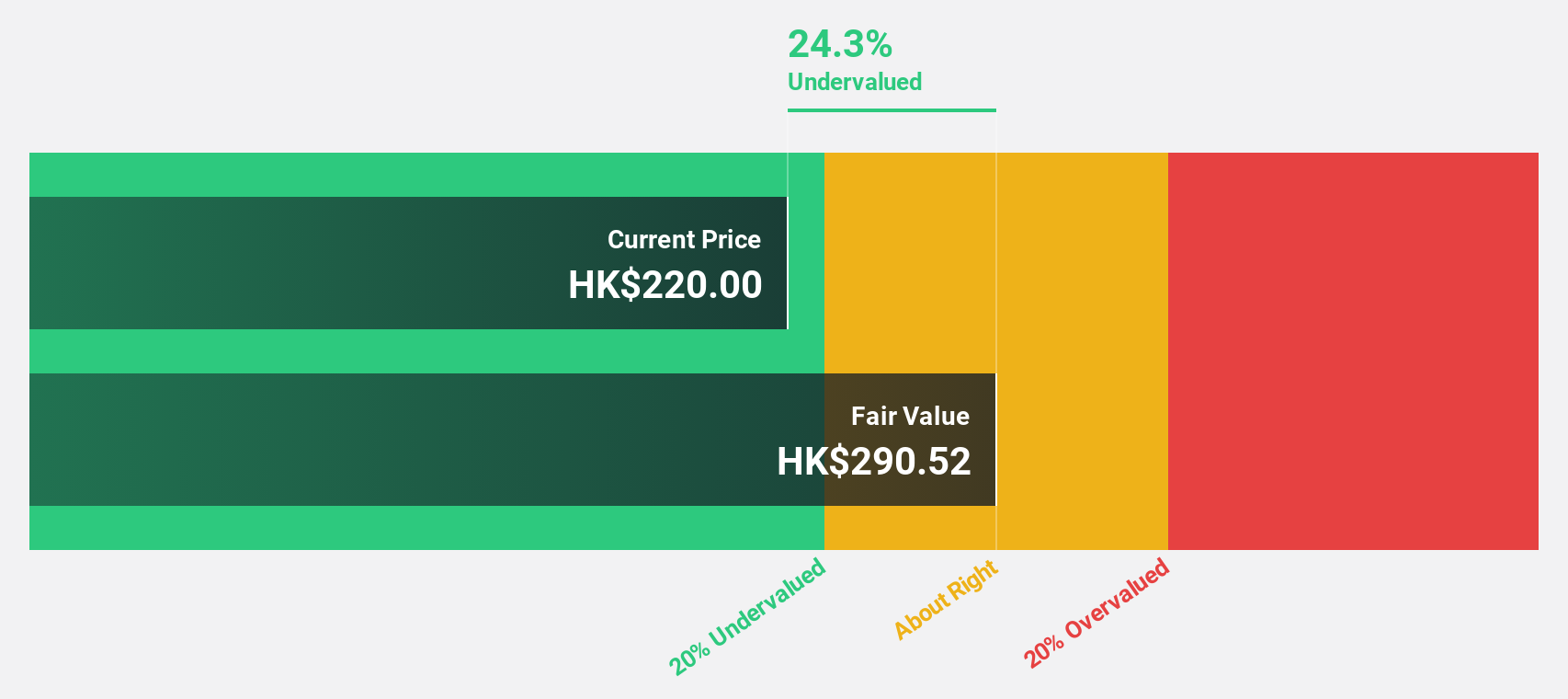

Estimated Discount To Fair Value: 10.2%

Pop Mart International Group, priced at HK$41.6, trades below its calculated fair value of HK$46.34, indicating potential undervaluation. With earnings expected to rise by 25.9% annually and revenue growth forecasted at 22.5% per year—both significantly outpacing the Hong Kong market averages—its financial outlook appears robust. Recent expansion into the European market with a new store in Amsterdam highlights its strategic growth initiatives, potentially enhancing future cash flows and market presence.

- The analysis detailed in our Pop Mart International Group growth report hints at robust future financial performance.

- Take a closer look at Pop Mart International Group's balance sheet health here in our report.

Taking Advantage

- Embark on your investment journey to our 41 Undervalued SEHK Stocks Based On Cash Flows selection here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Weimob might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:2013

Weimob

An investment holding company, provides digital commerce and media services in the People’s Republic of China.

Excellent balance sheet and good value.