Advertisement

- Hong Kong

- /

- Semiconductors

- /

- SEHK:1305

Wai Chi Holdings Company Limited (HKG:1305) Shares Fly 27% But Investors Aren't Buying For Growth

Wai Chi Holdings Company Limited (HKG:1305) shares have had a really impressive month, gaining 27% after a shaky period beforehand. Notwithstanding the latest gain, the annual share price return of 4.5% isn't as impressive.

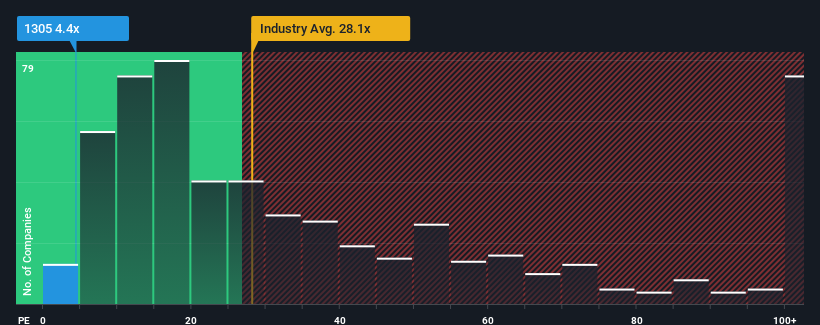

Although its price has surged higher, Wai Chi Holdings' price-to-earnings (or "P/E") ratio of 4.4x might still make it look like a strong buy right now compared to the market in Hong Kong, where around half of the companies have P/E ratios above 12x and even P/E's above 23x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

We've discovered 3 warning signs about Wai Chi Holdings. View them for free.Earnings have risen firmly for Wai Chi Holdings recently, which is pleasing to see. It might be that many expect the respectable earnings performance to degrade substantially, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Wai Chi Holdings

What Are Growth Metrics Telling Us About The Low P/E?

In order to justify its P/E ratio, Wai Chi Holdings would need to produce anemic growth that's substantially trailing the market.

Retrospectively, the last year delivered an exceptional 27% gain to the company's bottom line. Still, incredibly EPS has fallen 11% in total from three years ago, which is quite disappointing. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Weighing that medium-term earnings trajectory against the broader market's one-year forecast for expansion of 18% shows it's an unpleasant look.

With this information, we are not surprised that Wai Chi Holdings is trading at a P/E lower than the market. However, we think shrinking earnings are unlikely to lead to a stable P/E over the longer term, which could set up shareholders for future disappointment. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

The Final Word

Shares in Wai Chi Holdings are going to need a lot more upward momentum to get the company's P/E out of its slump. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Wai Chi Holdings maintains its low P/E on the weakness of its sliding earnings over the medium-term, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. If recent medium-term earnings trends continue, it's hard to see the share price moving strongly in either direction in the near future under these circumstances.

You always need to take note of risks, for example - Wai Chi Holdings has 3 warning signs we think you should be aware of.

If you're unsure about the strength of Wai Chi Holdings' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Wai Chi Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1305

Wai Chi Holdings

An investment holding company, manufactures and trades in light-emitting diode (LED) backlight and LED lighting products to business corporations and public utilities in the People’s Republic of China, Hong Kong, Taiwan, and internationally.

Excellent balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.8% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|22.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.8% overvalued

LI

Community Contributor