Pop Mart International Group (SEHK:9992) has been on investors’ radar recently as the stock’s upward drift catches attention, but there is no single event driving the movement. Sometimes, it is these quieter stretches that prompt the big questions: are we seeing a signal from the market, or is this just part of a broader trend? When a stock nudges higher without dramatic news announcements, it can reveal just as much about market sentiment as a blockbuster headline.

So, where does this leave Pop Mart International Group in the bigger picture? Over the past year, shares have gained 5%, a result that is not flashy but shows progress, while the recent month has been stronger, up nearly 4%. Recent annual revenue and net income growth above 24% and 26%, respectively, suggest solid fundamental momentum may be taking hold even as short-term weekly swings come and go.

With investors already seeing some positive moves, the critical question now is whether the stock’s current price leaves room for further upside or if the market’s latest gains are already factoring in all the expected growth.

Advertisement

Price-to-Earnings of 51.6x: Is it justified?

By the price-to-earnings (P/E) ratio, Pop Mart International Group appears expensive compared to its specialty retail peers and the broader Hong Kong industry average. Pop Mart's P/E is sitting at 51.6x, while the sector's average is just 14x.

The P/E ratio is a common valuation metric that illustrates how much investors are willing to pay for each dollar of a company’s earnings. In specialty retail, where growth can be rapid but competition is fierce, a high multiple often signals that investors expect outstanding future growth or profitability.

Pop Mart's elevated P/E suggests that the market is pricing in future expansion and ongoing momentum, possibly based on the company’s strong revenue and profit growth. However, compared to industry norms, the current multiple may be tough to justify unless the company's high growth rates can be sustained over the long term.

However, risks such as intensifying competition or unexpected shifts in consumer demand could challenge Pop Mart’s growth narrative and could potentially impact future expectations.

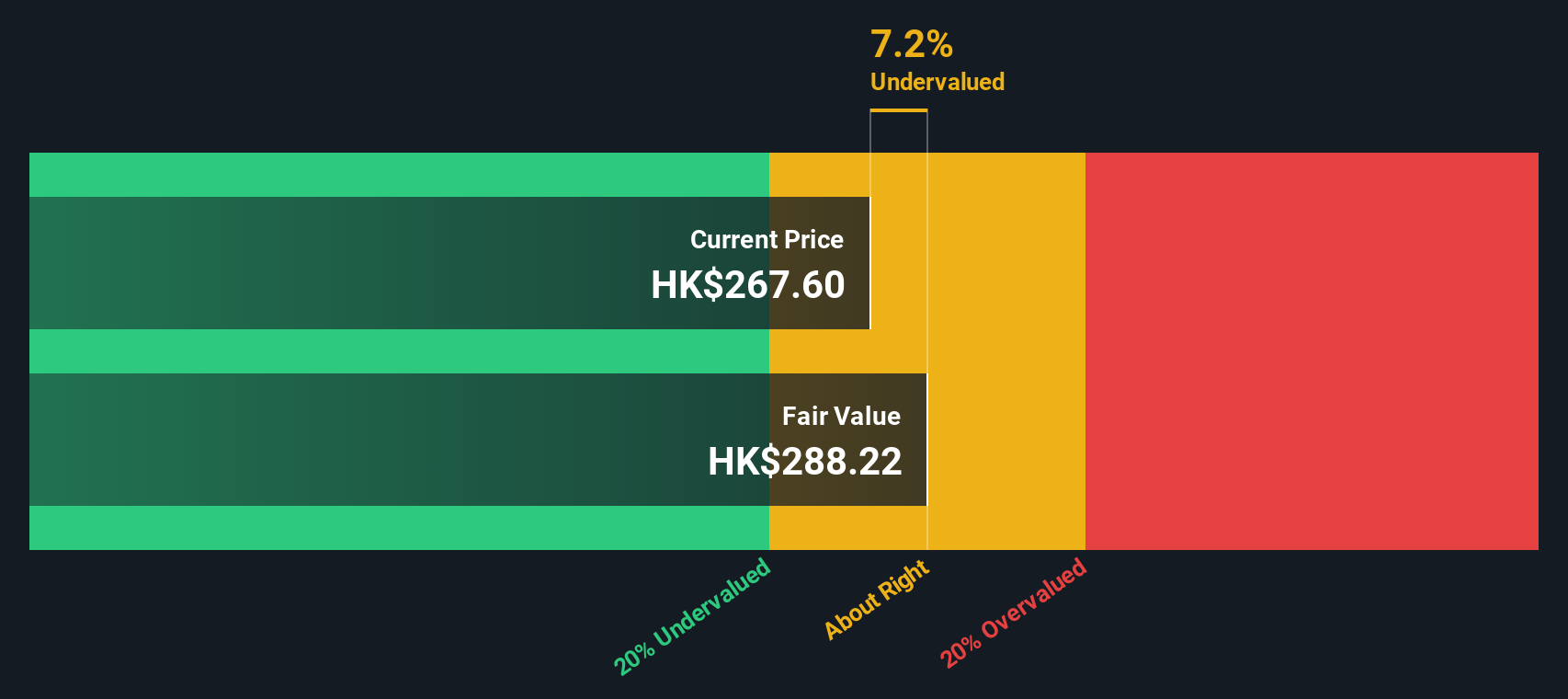

Another View: SWS DCF Model Offers a Second Opinion

Looking at Pop Mart International Group through the lens of our SWS DCF model provides another angle on its valuation. This method suggests the shares are almost in line with their estimated fair value. Does this support the market’s optimism, or is there more beneath the surface?

Build Your Own Pop Mart International Group Narrative

If you have your own viewpoint or want to dive deeper into the numbers, it takes less than three minutes to craft your own perspective. Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Pop Mart International Group.

Looking for More Investment Ideas?

Don't let great opportunities pass you by. Take the next step and find stocks that could transform your portfolio, using Simply Wall Street’s powerful screener tools designed for smart investors like you.

Unlock higher returns with undervalued stocks based on cash flows to see which companies stand out for their genuine growth potential at a compelling price.

Capitalize on the future of medicine by tapping into healthcare AI stocks, where innovative healthcare meets artificial intelligence.

Jump on emerging trends in digital innovation with cryptocurrency and blockchain stocks to spot trailblazers shaping tomorrow’s financial landscape.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

An investment holding company, engages in the design, development, and sale of pop toys in the People’s Republic of China, Hong Kong, Macao, Taiwan, and internationally.