Advertisement

- Hong Kong

- /

- Specialty Stores

- /

- SEHK:6909

It Might Not Be A Great Idea To Buy BetterLife Holding Limited (HKG:6909) For Its Next Dividend

BetterLife Holding Limited (HKG:6909) stock is about to trade ex-dividend in two days. The ex-dividend date is commonly two business days before the record date, which is the cut-off date for shareholders to be present on the company's books to be eligible for a dividend payment. The ex-dividend date is important as the process of settlement involves at least two full business days. So if you miss that date, you would not show up on the company's books on the record date. Meaning, you will need to purchase BetterLife Holding's shares before the 3rd of June to receive the dividend, which will be paid on the 30th of June.

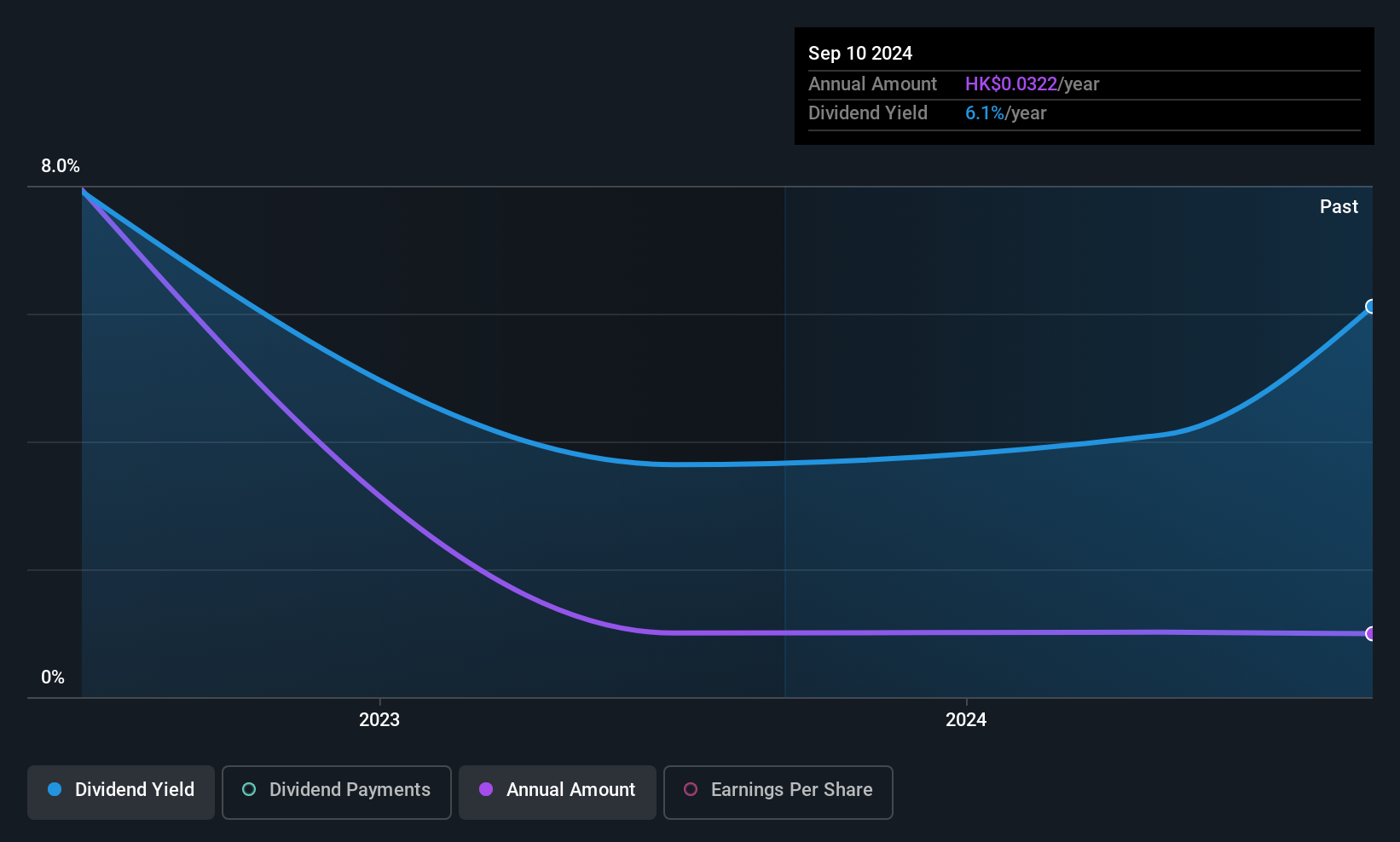

The company's upcoming dividend is CN¥0.02 a share, following on from the last 12 months, when the company distributed a total of CN¥0.04 per share to shareholders. Last year's total dividend payments show that BetterLife Holding has a trailing yield of 8.7% on the current share price of HK$0.50. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! So we need to check whether the dividend payments are covered, and if earnings are growing.

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. BetterLife Holding paid a dividend last year despite being unprofitable. This might be a one-off event, but it's not a sustainable state of affairs in the long run. Considering the lack of profitability, we also need to check if the company generated enough cash flow to cover the dividend payment. If cash earnings don't cover the dividend, the company would have to pay dividends out of cash in the bank, or by borrowing money, neither of which is long-term sustainable. Luckily it paid out just 8.8% of its free cash flow last year.

Check out our latest analysis for BetterLife Holding

Click here to see how much of its profit BetterLife Holding paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

When earnings decline, dividend companies become much harder to analyse and own safely. If earnings fall far enough, the company could be forced to cut its dividend. BetterLife Holding was unprofitable last year and, unfortunately, the general trend suggests its earnings have been in decline over the last five years, making us wonder if the dividend is sustainable at all.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. BetterLife Holding's dividend payments per share have declined at 43% per year on average over the past three years, which is uninspiring. While it's not great that earnings and dividends per share have fallen in recent years, we're encouraged by the fact that management has trimmed the dividend rather than risk over-committing the company in a risky attempt to maintain yields to shareholders.

Get our latest analysis on BetterLife Holding's balance sheet health here.

To Sum It Up

From a dividend perspective, should investors buy or avoid BetterLife Holding? It's hard to get used to BetterLife Holding paying a dividend despite reporting a loss over the past year. At least the dividend was covered by free cash flow, however. It's not an attractive combination from a dividend perspective, and we're inclined to pass on this one for the time being.

With that being said, if you're still considering BetterLife Holding as an investment, you'll find it beneficial to know what risks this stock is facing. Be aware that BetterLife Holding is showing 4 warning signs in our investment analysis, and 1 of those is a bit concerning...

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if BetterLife Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:6909

BetterLife Holding

Provides automobile dealership services with a focus on luxury and ultra-luxury brands in the People’s Republic of China.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor