Advertisement

- Hong Kong

- /

- Retail Distributors

- /

- SEHK:444

Sincere Watch (Hong Kong) Limited's (HKG:444) 30% Price Boost Is Out Of Tune With Revenues

The Sincere Watch (Hong Kong) Limited (HKG:444) share price has done very well over the last month, posting an excellent gain of 30%. But the last month did very little to improve the 59% share price decline over the last year.

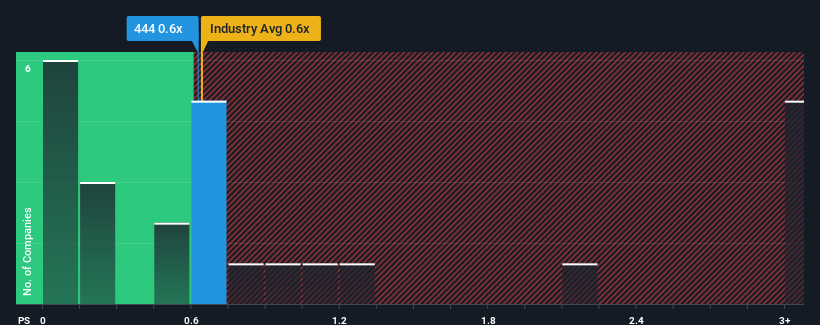

Even after such a large jump in price, you could still be forgiven for feeling indifferent about Sincere Watch (Hong Kong)'s P/S ratio of 0.6x, since the median price-to-sales (or "P/S") ratio for the Retail Distributors industry in Hong Kong is about the same. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Check out our latest analysis for Sincere Watch (Hong Kong)

How Sincere Watch (Hong Kong) Has Been Performing

Sincere Watch (Hong Kong) has been doing a good job lately as it's been growing revenue at a solid pace. Perhaps the market is expecting future revenue performance to only keep up with the broader industry, which has keeping the P/S in line with expectations. If that doesn't eventuate, then existing shareholders probably aren't too pessimistic about the future direction of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Sincere Watch (Hong Kong) will help you shine a light on its historical performance.Do Revenue Forecasts Match The P/S Ratio?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Sincere Watch (Hong Kong)'s to be considered reasonable.

Retrospectively, the last year delivered an exceptional 28% gain to the company's top line. Still, revenue has fallen 7.9% in total from three years ago, which is quite disappointing. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Weighing that medium-term revenue trajectory against the broader industry's one-year forecast for expansion of 29% shows it's an unpleasant look.

With this information, we find it concerning that Sincere Watch (Hong Kong) is trading at a fairly similar P/S compared to the industry. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh on the share price eventually.

The Bottom Line On Sincere Watch (Hong Kong)'s P/S

Sincere Watch (Hong Kong)'s stock has a lot of momentum behind it lately, which has brought its P/S level with the rest of the industry. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We find it unexpected that Sincere Watch (Hong Kong) trades at a P/S ratio that is comparable to the rest of the industry, despite experiencing declining revenues during the medium-term, while the industry as a whole is expected to grow. Even though it matches the industry, we're uncomfortable with the current P/S ratio, as this dismal revenue performance is unlikely to support a more positive sentiment for long. Unless the the circumstances surrounding the recent medium-term improve, it wouldn't be wrong to expect a a difficult period ahead for the company's shareholders.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for Sincere Watch (Hong Kong) (1 is concerning) you should be aware of.

If these risks are making you reconsider your opinion on Sincere Watch (Hong Kong), explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:444

Sincere Watch (Hong Kong)

An investment holding company, distributes branded luxury watches, timepieces, and accessories in Hong Kong, Macau, Taiwan, Korea, the People’s Republic of China, and internationally.

Moderate risk and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

80 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

91 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative