Advertisement

- Hong Kong

- /

- Specialty Stores

- /

- SEHK:1728

This Analyst Just Downgraded Their China ZhengTong Auto Services Holdings Limited (HKG:1728) EPS Forecasts

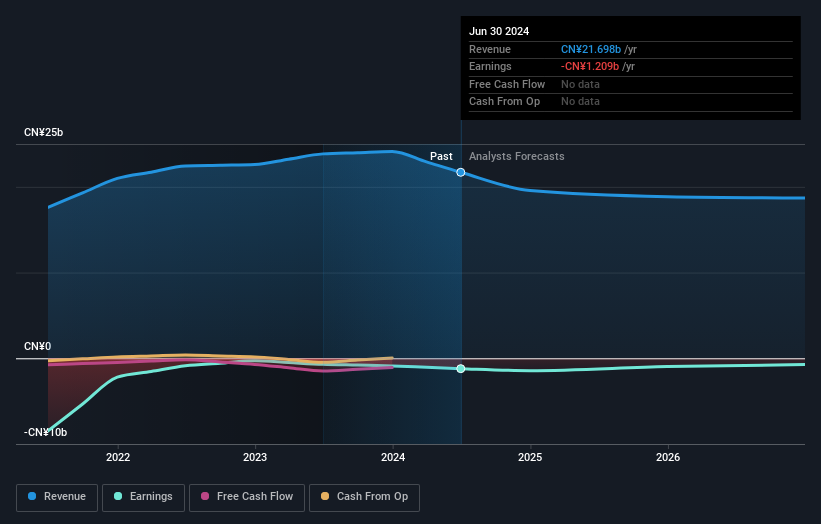

The analyst covering China ZhengTong Auto Services Holdings Limited (HKG:1728) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for this year. Both revenue and earnings per share (EPS) estimates were cut sharply as the analyst factored in the latest outlook for the business, concluding that they were too optimistic previously.

After the downgrade, the consensus from China ZhengTong Auto Services Holdings' one analyst is for revenues of CN¥20b in 2024, which would reflect an uncomfortable 9.8% decline in sales compared to the last year of performance. Losses are supposed to balloon 29% to CN¥0.46 per share. Yet before this consensus update, the analyst had been forecasting revenues of CN¥27b and losses of CN¥0.20 per share in 2024. Ergo, there's been a clear change in sentiment, with the analyst administering a notable cut to this year's revenue estimates, while at the same time increasing their loss per share forecasts.

Check out our latest analysis for China ZhengTong Auto Services Holdings

The consensus price target fell 69% to CN¥0.064, implicitly signalling that lower earnings per share are a leading indicator for China ZhengTong Auto Services Holdings' valuation.

Of course, another way to look at these forecasts is to place them into context against the industry itself. Over the past five years, revenues have declined around 7.7% annually. Worse, forecasts are essentially predicting the decline to accelerate, with the estimate for an annualised 9.8% decline in revenue until the end of 2024. Compare this against analyst estimates for companies in the broader industry, which suggest that revenues (in aggregate) are expected to grow 10% annually. So while a broad number of companies are forecast to grow, unfortunately China ZhengTong Auto Services Holdings is expected to see its sales affected worse than other companies in the industry.

The Bottom Line

The most important thing to take away is that the analyst increased their loss per share estimates for this year. Unfortunately the analyst also downgraded their revenue estimates, and industry data suggests that China ZhengTong Auto Services Holdings' revenues are expected to grow slower than the wider market. After such a stark change in sentiment from the analyst, we'd understand if readers now felt a bit wary of China ZhengTong Auto Services Holdings.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have analyst estimates for China ZhengTong Auto Services Holdings going out as far as 2026, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies backed by insiders.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1728

China ZhengTong Auto Services Holdings

An investment holding company, engages in 4S dealership business, supply chain business, and comprehensive properties business in the People’s Republic of China.

Mediocre balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor