Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:432

Pacific Century Premium Developments (HKG:432) Has Debt But No Earnings; Should You Worry?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Pacific Century Premium Developments Limited (HKG:432) makes use of debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Pacific Century Premium Developments

What Is Pacific Century Premium Developments's Net Debt?

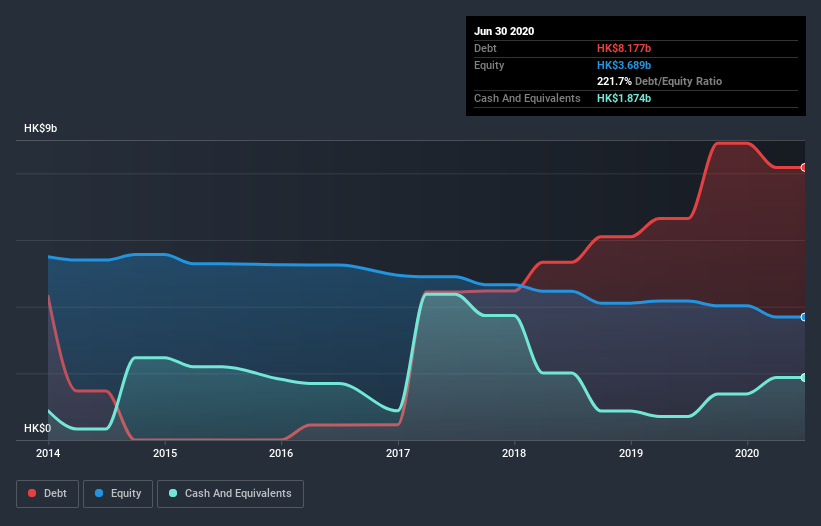

The image below, which you can click on for greater detail, shows that at June 2020 Pacific Century Premium Developments had debt of HK$8.18b, up from HK$6.65b in one year. However, it does have HK$1.87b in cash offsetting this, leading to net debt of about HK$6.30b.

A Look At Pacific Century Premium Developments's Liabilities

The latest balance sheet data shows that Pacific Century Premium Developments had liabilities of HK$2.35b due within a year, and liabilities of HK$7.65b falling due after that. Offsetting this, it had HK$1.87b in cash and HK$17.0m in receivables that were due within 12 months. So its liabilities total HK$8.11b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the HK$1.32b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. At the end of the day, Pacific Century Premium Developments would probably need a major re-capitalization if its creditors were to demand repayment. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Pacific Century Premium Developments will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, Pacific Century Premium Developments reported revenue of HK$2.4b, which is a gain of 597%, although it did not report any earnings before interest and tax. When it comes to revenue growth, that's like nailing the game winning 3-pointer!

Caveat Emptor

Even though Pacific Century Premium Developments managed to grow its top line quite deftly, the cold hard truth is that it is losing money on the EBIT line. Indeed, it lost a very considerable HK$132m at the EBIT level. When you combine this with the very significant balance sheet liabilities mentioned above, we are so wary of it that we are basically at a loss for the right words. Like every long-shot we're sure it has a glossy presentation outlining its blue-sky potential. But the fact is that it incinerated HK$381m of cash in the last twelve months, and has precious few liquid assets in comparison to its liabilities. So we consider this a high risk stock, and we're worried its share price could sink faster than than a dingy with a great white shark attacking it. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Like risks, for instance. Every company has them, and we've spotted 4 warning signs for Pacific Century Premium Developments (of which 2 are potentially serious!) you should know about.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

When trading Pacific Century Premium Developments or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About SEHK:432

Pacific Century Premium Developments

Engages in the development and management of property and infrastructure projects in Hong Kong, Japan, Thailand, and Indonesia.

Mediocre balance sheet and overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor