Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:3616

Ever Reach Group (Holdings) (HKG:3616) Takes On Some Risk With Its Use Of Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Ever Reach Group (Holdings) Company Limited (HKG:3616) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Ever Reach Group (Holdings)

What Is Ever Reach Group (Holdings)'s Debt?

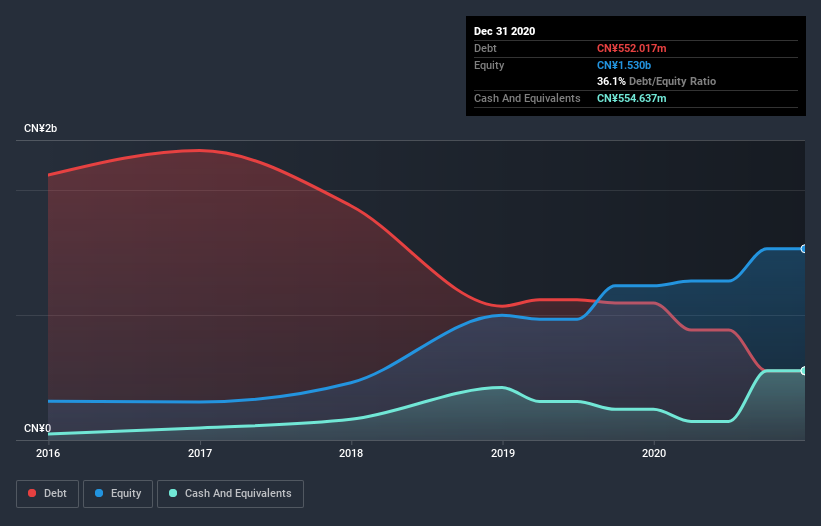

The image below, which you can click on for greater detail, shows that Ever Reach Group (Holdings) had debt of CN¥552.0m at the end of December 2020, a reduction from CN¥1.10b over a year. However, its balance sheet shows it holds CN¥554.6m in cash, so it actually has CN¥2.62m net cash.

How Strong Is Ever Reach Group (Holdings)'s Balance Sheet?

We can see from the most recent balance sheet that Ever Reach Group (Holdings) had liabilities of CN¥6.70b falling due within a year, and liabilities of CN¥276.4m due beyond that. Offsetting these obligations, it had cash of CN¥554.6m as well as receivables valued at CN¥281.6m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥6.14b.

The deficiency here weighs heavily on the CN¥1.37b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we definitely think shareholders need to watch this one closely. After all, Ever Reach Group (Holdings) would likely require a major re-capitalisation if it had to pay its creditors today. Given that Ever Reach Group (Holdings) has more cash than debt, we're pretty confident it can handle its debt, despite the fact that it has a lot of liabilities in total.

But the bad news is that Ever Reach Group (Holdings) has seen its EBIT plunge 14% in the last twelve months. If that rate of decline in earnings continues, the company could find itself in a tight spot. There's no doubt that we learn most about debt from the balance sheet. But it is Ever Reach Group (Holdings)'s earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. Ever Reach Group (Holdings) may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. In the last three years, Ever Reach Group (Holdings)'s free cash flow amounted to 26% of its EBIT, less than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Summing up

While Ever Reach Group (Holdings) does have more liabilities than liquid assets, it also has net cash of CN¥2.62m. Despite its cash we think that Ever Reach Group (Holdings) seems to struggle to handle its total liabilities, so we are wary of the stock. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For example - Ever Reach Group (Holdings) has 1 warning sign we think you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you decide to trade Ever Reach Group (Holdings), use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Ever Reach Group (Holdings) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:3616

Ever Reach Group (Holdings)

An investment holding company, engages in the property development and investment activities in the People’s Republic of China.

Slight risk with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|20.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor