Advertisement

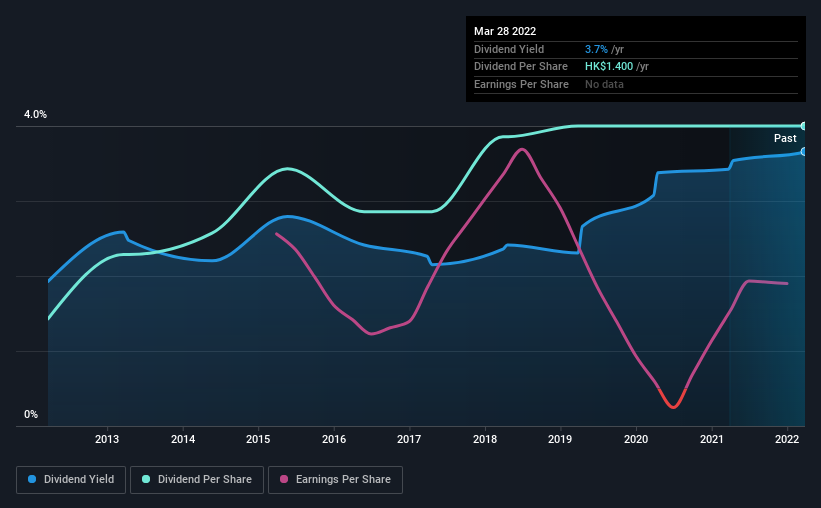

Nanyang Holdings Limited (HKG:212) will pay a dividend of HK$1.40 on the 13th of June. The dividend yield is 3.7% based on this payment, which is a little bit low compared to the other companies in the industry.

View our latest analysis for Nanyang Holdings

Nanyang Holdings' Dividend Is Well Covered By Earnings

It would be nice for the yield to be higher, but we should also check if higher levels of dividend payment would be sustainable. Based on the last payment, Nanyang Holdings was paying only paying out a fraction of earnings, but the payment was a massive 303% of cash flows. A cash payout ratio this high could put the dividend under pressure and force the company to reduce it in the future if it were to run into tough times.

Looking forward, earnings per share could rise by 9.5% over the next year if the trend from the last few years continues. Assuming the dividend continues along recent trends, we think the payout ratio could be 24% by next year, which is in a pretty sustainable range.

Nanyang Holdings Has A Solid Track Record

The company has an extended history of paying stable dividends. The first annual payment during the last 10 years was HK$0.50 in 2012, and the most recent fiscal year payment was HK$1.40. This implies that the company grew its distributions at a yearly rate of about 11% over that duration. So, dividends have been growing pretty quickly, and even more impressively, they haven't experienced any notable falls during this period.

We Could See Nanyang Holdings' Dividend Growing

Investors could be attracted to the stock based on the quality of its payment history. Nanyang Holdings has seen EPS rising for the last five years, at 9.5% per annum. With a decent amount of growth and a low payout ratio, we think this bodes well for Nanyang Holdings' prospects of growing its dividend payments in the future.

Our Thoughts On Nanyang Holdings' Dividend

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about Nanyang Holdings' payments, as there could be some issues with sustaining them into the future. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. We would be a touch cautious of relying on this stock primarily for the dividend income.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Case in point: We've spotted 3 warning signs for Nanyang Holdings (of which 1 is a bit unpleasant!) you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Nanyang Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:212

Nanyang Holdings

An investment holding company, engages in the property investment and trading businesses in Hong Kong, the United States, Europe, Taiwan, and internationally.

Flawless balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor