China Overseas Land & Investment (SEHK:688) is in the spotlight this week following the release of the first price list for Double Coast III in Kai Tak. This move reflects ongoing property development activity and signals future sales momentum for the group.

The release of the Double Coast III price list has clearly caught investors’ attention, as China Overseas Land & Investment’s share price is up 14.8% year-to-date and total shareholder return sits at 10.7% for the past twelve months. While momentum has picked up strongly in 2024, the longer-term picture shows that shareholders are still working their way back from a tougher three-year stretch.

With shares trending higher and the Double Coast III launch making headlines, is China Overseas Land & Investment now undervalued, or has renewed optimism already found its way into the price? Is there a buying opportunity here, or has the market already priced in future growth?

Advertisement

Price-to-Earnings of 10x: Is it justified?

China Overseas Land & Investment is currently trading at a price-to-earnings (P/E) ratio of 10x, below its peer average and the broader Hong Kong market. This suggests shares could be undervalued based on this metric.

The P/E ratio measures how much investors are willing to pay per dollar of current earnings. It is a crucial indicator for property developers, where future earnings growth can be inconsistent or linked to cyclical trends. For China Overseas Land & Investment, a lower P/E may indicate the market is discounting its earnings prospects or overlooking the company’s underlying strengths.

Compared to the Hong Kong Real Estate industry average of 13.6x and the peer average of 16.8x, 10x stands out as attractively low. Using regression-based fair value analysis, the estimated fair P/E ratio for the company is 16.4x. This highlights significant upside if the market re-rates the stock toward this level.

However, persistent negative three-year returns and cyclicality in property demand could still weigh on future prospects and could challenge the bullish outlook.

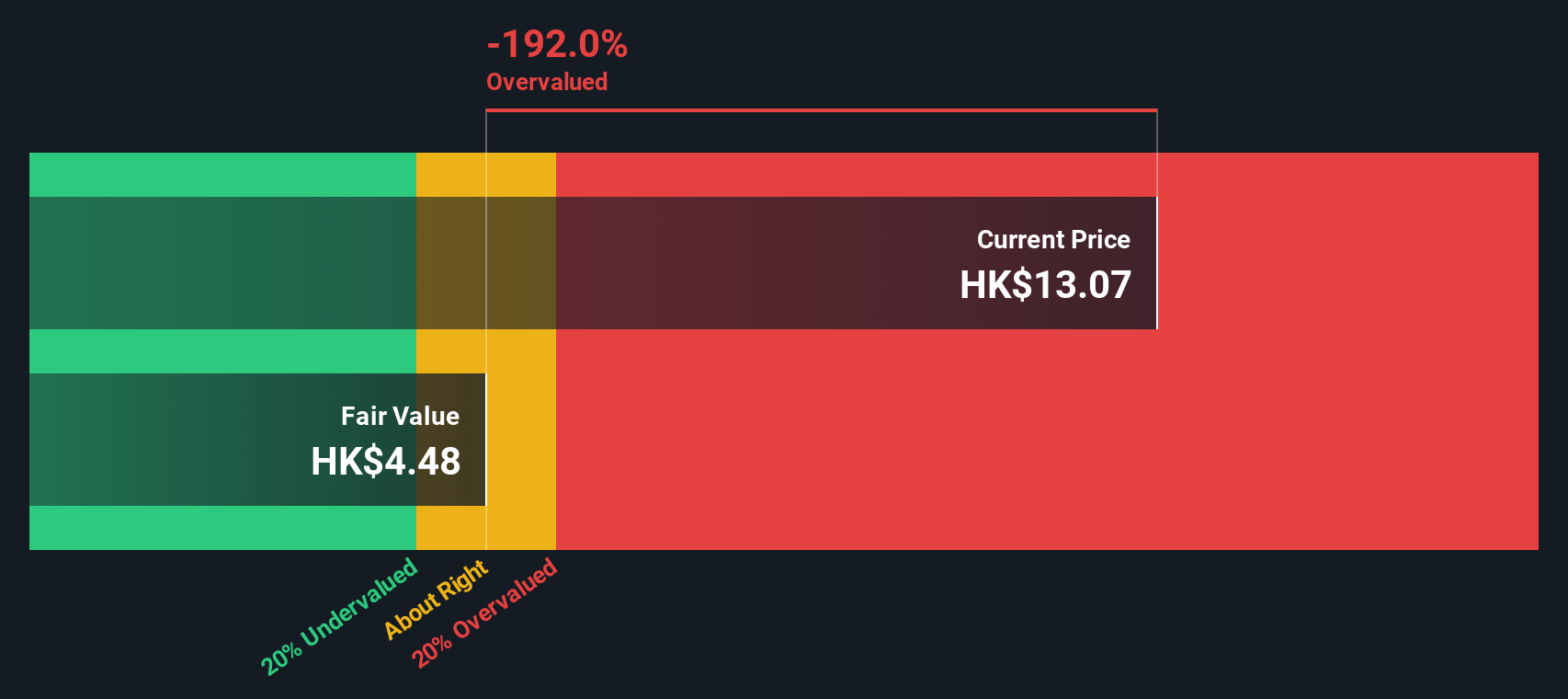

Another View: DCF Model Suggests a Different Story

While the price-to-earnings ratio paints China Overseas Land & Investment as undervalued, our DCF model tells a much less optimistic story. According to this approach, the stock is trading well above its fair value. This suggests the current price might be overestimating long-term cash flows. Does this mean risk is lurking beneath recent momentum?

Build Your Own China Overseas Land & Investment Narrative

If you have a different perspective or want to dig deeper, you can quickly build your own view on the stock using our tools: Do it your way.

A great starting point for your China Overseas Land & Investment research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

There's a world of opportunity beyond just one stock. Now is your chance to scout out what else is making waves and position yourself ahead of the crowd. Check out these hand-picked ways you can take action with market-leading trends today:

Get ahead of the curve in tech by investigating these 26 AI penny stocks leveraging artificial intelligence to gain a competitive edge in their industries.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies

An investment holding company, engages in the property development, commercial property operations, and other businesses in the People’s Republic of China and the United Kingdom.