Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:1755

S-Enjoy Service Group Co., Limited (HKG:1755) Surges 25% Yet Its Low P/E Is No Reason For Excitement

The S-Enjoy Service Group Co., Limited (HKG:1755) share price has done very well over the last month, posting an excellent gain of 25%. But the gains over the last month weren't enough to make shareholders whole, as the share price is still down 9.6% in the last twelve months.

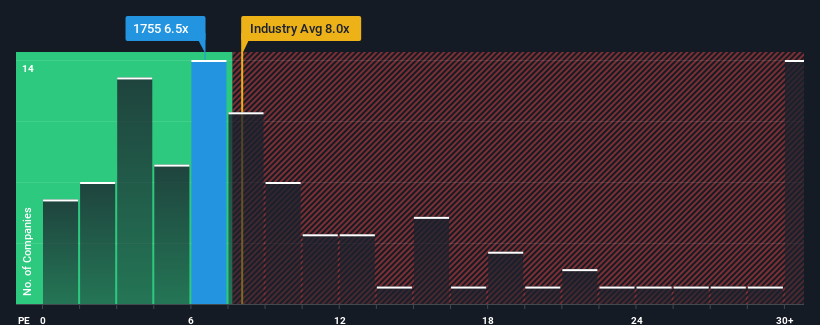

In spite of the firm bounce in price, given about half the companies in Hong Kong have price-to-earnings ratios (or "P/E's") above 10x, you may still consider S-Enjoy Service Group as an attractive investment with its 6.5x P/E ratio. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

While the market has experienced earnings growth lately, S-Enjoy Service Group's earnings have gone into reverse gear, which is not great. It seems that many are expecting the dour earnings performance to persist, which has repressed the P/E. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Check out our latest analysis for S-Enjoy Service Group

Does Growth Match The Low P/E?

There's an inherent assumption that a company should underperform the market for P/E ratios like S-Enjoy Service Group's to be considered reasonable.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 7.9%. As a result, earnings from three years ago have also fallen 22% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Turning to the outlook, the next three years should generate growth of 7.5% per year as estimated by the nine analysts watching the company. With the market predicted to deliver 12% growth each year, the company is positioned for a weaker earnings result.

In light of this, it's understandable that S-Enjoy Service Group's P/E sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Final Word

Despite S-Enjoy Service Group's shares building up a head of steam, its P/E still lags most other companies. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of S-Enjoy Service Group's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Before you settle on your opinion, we've discovered 1 warning sign for S-Enjoy Service Group that you should be aware of.

If you're unsure about the strength of S-Enjoy Service Group's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1755

S-Enjoy Service Group

An investment holding company, provides property management and related value-added services for property developers in the People’s Republic of China.

Flawless balance sheet and undervalued.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor