Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:1218

Shareholders May Be More Conservative With Easyknit International Holdings Limited's (HKG:1218) CEO Compensation For Now

Key Insights

- Easyknit International Holdings to hold its Annual General Meeting on 21st of August

- Salary of HK$2.29m is part of CEO Candy Koon's total remuneration

- The overall pay is 42% above the industry average

- Easyknit International Holdings' three-year loss to shareholders was 58% while its EPS was down 74% over the past three years

The underwhelming share price performance of Easyknit International Holdings Limited (HKG:1218) in the past three years would have disappointed many shareholders. Per share earnings growth is also lacking, despite revenue growth. The AGM coming up on 21st of August will be an opportunity for shareholders to have their concerns addressed by the board and for them to exercise their influence on management through voting on resolutions such as executive remuneration. Here's our take on why we think shareholders might be hesitant about approving a raise at the moment.

Check out our latest analysis for Easyknit International Holdings

How Does Total Compensation For Candy Koon Compare With Other Companies In The Industry?

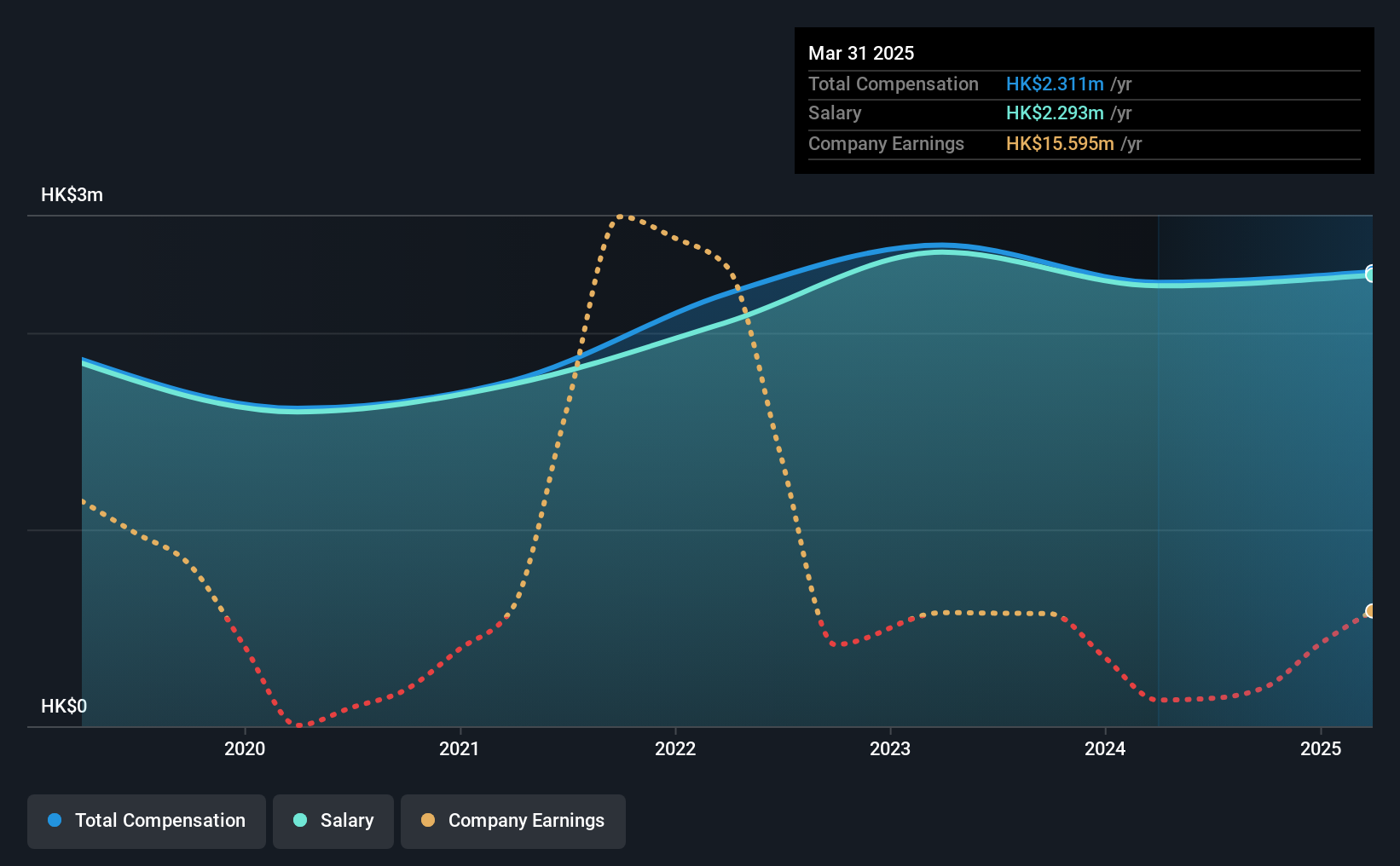

Our data indicates that Easyknit International Holdings Limited has a market capitalization of HK$118m, and total annual CEO compensation was reported as HK$2.3m for the year to March 2025. This means that the compensation hasn't changed much from last year. In particular, the salary of HK$2.29m, makes up a huge portion of the total compensation being paid to the CEO.

For comparison, other companies in the Hong Kong Real Estate industry with market capitalizations below HK$1.6b, reported a median total CEO compensation of HK$1.6m. This suggests that Candy Koon is paid more than the median for the industry.

| Component | 2025 | 2024 | Proportion (2025) |

| Salary | HK$2.3m | HK$2.2m | 99% |

| Other | HK$18k | HK$18k | 1% |

| Total Compensation | HK$2.3m | HK$2.3m | 100% |

Speaking on an industry level, nearly 84% of total compensation represents salary, while the remainder of 16% is other remuneration. Easyknit International Holdings pays a high salary, concentrating more on this aspect of compensation in comparison to non-salary pay. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Easyknit International Holdings Limited's Growth Numbers

Over the last three years, Easyknit International Holdings Limited has shrunk its earnings per share by 74% per year. In the last year, its revenue is up 149%.

Investors would be a bit wary of companies that have lower EPS On the other hand, the strong revenue growth suggests the business is growing. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Easyknit International Holdings Limited Been A Good Investment?

Few Easyknit International Holdings Limited shareholders would feel satisfied with the return of -58% over three years. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

To Conclude...

Easyknit International Holdings pays its CEO a majority of compensation through a salary. The company's earnings haven't grown and possibly because of that, the stock has performed poorly, resulting in a loss for the company's shareholders. Shareholders will get the chance at the upcoming AGM to question the board on key matters, such as CEO remuneration or any other issues they might have and revisit their investment thesis with regards to the company.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. We did our research and spotted 3 warning signs for Easyknit International Holdings that investors should look into moving forward.

Switching gears from Easyknit International Holdings, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Valuation is complex, but we're here to simplify it.

Discover if Easyknit International Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1218

Easyknit International Holdings

An investment holding company, engages in the investment and development of properties in Hong Kong and Singapore.

Slight risk with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor