Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:1030

Analysts' Revenue Estimates For Seazen Group Limited (HKG:1030) Are Surging Higher

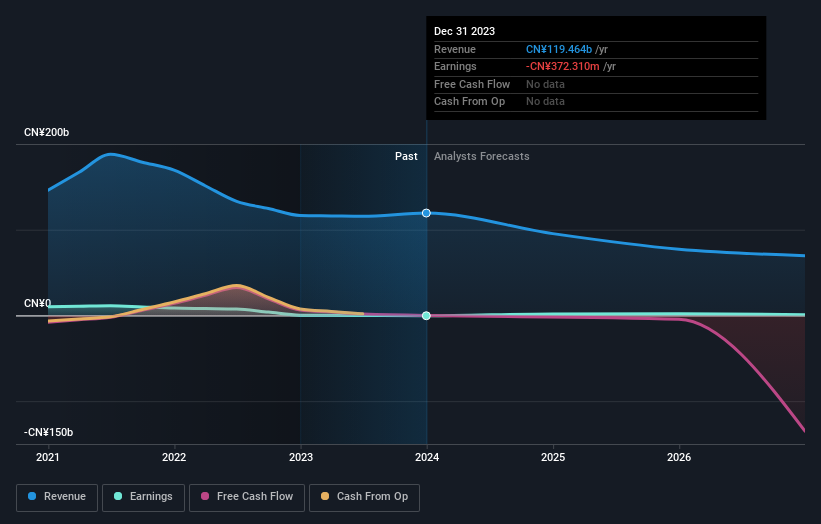

Celebrations may be in order for Seazen Group Limited (HKG:1030) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. The revenue forecast for this year has experienced a facelift, with analysts now much more optimistic on its sales pipeline.

After the upgrade, the consensus from Seazen Group's seven analysts is for revenues of CN¥95b in 2024, which would reflect a disturbing 20% decline in sales compared to the last year of performance. The losses are expected to disappear over the next year or so, with forecasts for a profit of CN¥0.33 per share this year. Previously, the analysts had been modelling revenues of CN¥86b and earnings per share (EPS) of CN¥0.31 in 2024. The most recent forecasts are noticeably more optimistic, with a nice increase in revenue estimates and a lift to earnings per share as well.

Check out our latest analysis for Seazen Group

Despite these upgrades, the consensus price target fell 8.5% to CN¥1.19, perhaps signalling that the uplift in performance is not expected to last. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on Seazen Group, with the most bullish analyst valuing it at CN¥1.73 and the most bearish at CN¥0.74 per share. This is a fairly broad spread of estimates, suggesting that the analysts are forecasting a wide range of possible outcomes for the business.

Of course, another way to look at these forecasts is to place them into context against the industry itself. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 20% by the end of 2024. This indicates a significant reduction from annual growth of 13% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 5.2% per year. It's pretty clear that Seazen Group's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to take away from this upgrade is that analysts upgraded their earnings per share estimates for this year, expecting improving business conditions. Fortunately, they also upgraded their revenue estimates, and are forecasting revenues to grow slower than the wider market. The consensus price target fell measurably, with analysts seemingly not reassured by recent business developments, leading to a lower estimate of Seazen Group's future valuation. Seeing the dramatic upgrade to this year's forecasts, it might be time to take another look at Seazen Group.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. We have estimates - from multiple Seazen Group analysts - going out to 2026, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1030

Seazen Group

Engages in the investment, development, management, and sale of properties in the People’s Republic of China.

Moderate growth potential with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|24.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|13.5% overvalued

DA

Community Contributor