Advertisement

Shenzhen Neptunus Interlong Bio-technique Company Limited's (HKG:8329) Share Price Is Matching Sentiment Around Its Earnings

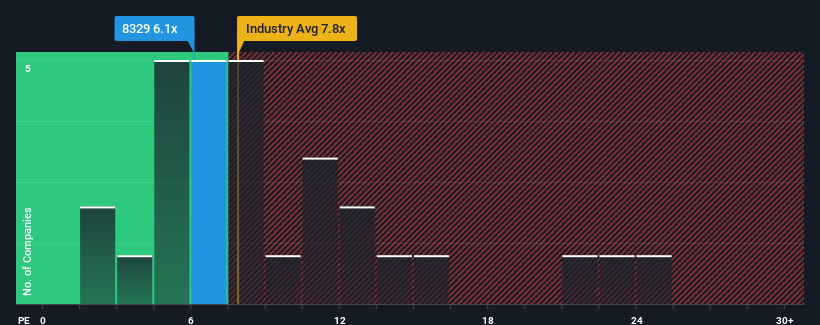

Shenzhen Neptunus Interlong Bio-technique Company Limited's (HKG:8329) price-to-earnings (or "P/E") ratio of 6.1x might make it look like a buy right now compared to the market in Hong Kong, where around half of the companies have P/E ratios above 9x and even P/E's above 18x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

For example, consider that Shenzhen Neptunus Interlong Bio-technique's financial performance has been poor lately as its earnings have been in decline. One possibility is that the P/E is low because investors think the company won't do enough to avoid underperforming the broader market in the near future. However, if this doesn't eventuate then existing shareholders may be feeling optimistic about the future direction of the share price.

View our latest analysis for Shenzhen Neptunus Interlong Bio-technique

Is There Any Growth For Shenzhen Neptunus Interlong Bio-technique?

The only time you'd be truly comfortable seeing a P/E as low as Shenzhen Neptunus Interlong Bio-technique's is when the company's growth is on track to lag the market.

Retrospectively, the last year delivered a frustrating 50% decrease to the company's bottom line. This means it has also seen a slide in earnings over the longer-term as EPS is down 15% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Comparing that to the market, which is predicted to deliver 22% growth in the next 12 months, the company's downward momentum based on recent medium-term earnings results is a sobering picture.

In light of this, it's understandable that Shenzhen Neptunus Interlong Bio-technique's P/E would sit below the majority of other companies. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

What We Can Learn From Shenzhen Neptunus Interlong Bio-technique's P/E?

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Shenzhen Neptunus Interlong Bio-technique revealed its shrinking earnings over the medium-term are contributing to its low P/E, given the market is set to grow. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. If recent medium-term earnings trends continue, it's hard to see the share price moving strongly in either direction in the near future under these circumstances.

It is also worth noting that we have found 4 warning signs for Shenzhen Neptunus Interlong Bio-technique (1 is a bit concerning!) that you need to take into consideration.

Of course, you might also be able to find a better stock than Shenzhen Neptunus Interlong Bio-technique. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:8329

Shenzhen Neptunus Interlong Bio-technique

Engages in the research and development, manufacturing, and selling of medicines and medical devices in the People’s Republic of China.

Excellent balance sheet with moderate risk.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.6% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.6% undervalued

GM

Community Contributor