Advertisement

Does TOT BIOPHARM International (HKG:1875) Have A Healthy Balance Sheet?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies TOT BIOPHARM International Company Limited (HKG:1875) makes use of debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

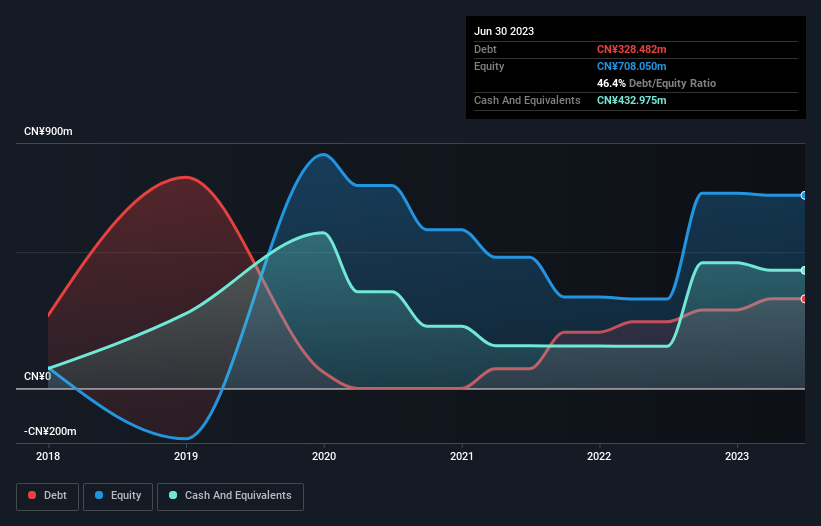

See our latest analysis for TOT BIOPHARM International

How Much Debt Does TOT BIOPHARM International Carry?

As you can see below, at the end of June 2023, TOT BIOPHARM International had CN¥328.5m of debt, up from CN¥244.8m a year ago. Click the image for more detail. But on the other hand it also has CN¥433.0m in cash, leading to a CN¥104.5m net cash position.

A Look At TOT BIOPHARM International's Liabilities

Zooming in on the latest balance sheet data, we can see that TOT BIOPHARM International had liabilities of CN¥312.6m due within 12 months and liabilities of CN¥343.9m due beyond that. Offsetting these obligations, it had cash of CN¥433.0m as well as receivables valued at CN¥86.9m due within 12 months. So its liabilities total CN¥136.6m more than the combination of its cash and short-term receivables.

Since publicly traded TOT BIOPHARM International shares are worth a total of CN¥1.40b, it seems unlikely that this level of liabilities would be a major threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. Despite its noteworthy liabilities, TOT BIOPHARM International boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if TOT BIOPHARM International can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year TOT BIOPHARM International wasn't profitable at an EBIT level, but managed to grow its revenue by 150%, to CN¥588m. So there's no doubt that shareholders are cheering for growth

So How Risky Is TOT BIOPHARM International?

Statistically speaking companies that lose money are riskier than those that make money. And the fact is that over the last twelve months TOT BIOPHARM International lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of CN¥214m and booked a CN¥49m accounting loss. However, it has net cash of CN¥104.5m, so it has a bit of time before it will need more capital. Importantly, TOT BIOPHARM International's revenue growth is hot to trot. High growth pre-profit companies may well be risky, but they can also offer great rewards. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 1 warning sign with TOT BIOPHARM International , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if BioDlink International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1875

BioDlink International

An investment holding company, engages in the research and development, manufacturing, and marketing of anti-tumor drugs in Mainland China and internationally.

Excellent balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|31.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|44.7% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$174.00|35.8% undervalued

AG

Community Contributor