Advertisement

Assessing Innovent Biologics (SEHK:1801) Valuation Following Strong Share Price Momentum

Simply Wall St

Reviewed by Simply Wall St

Innovent Biologics (SEHK:1801) shares have shown some movement recently, drawing the attention of investors interested in the biotech space. With steady revenue and net income growth over the past year, there are clear factors to watch in this situation.

See our latest analysis for Innovent Biologics.

With a share price sitting at HK$92.0, Innovent Biologics has seen impressive momentum this year, as shown by a 159.15% year-to-date share price return and a 147.98% total shareholder return over the past twelve months. While recent days brought a fresh 5.44% gain, this follows a multi-year rally that highlights the market’s renewed optimism about the company’s growth outlook.

If strong moves in biotech have your attention, it is a perfect time to check out our dedicated list of innovators through the See the full list for free..

With the share price now approaching analyst targets, the key question becomes whether Innovent Biologics still has room to climb or if the market has already accounted for all of its future growth. Could there still be a real buying opportunity ahead?

Price-to-Earnings of 127.1x: Is it justified?

With Innovent Biologics trading at a price-to-earnings ratio of 127.1x, investors are currently paying a steep premium compared to both the broader market and its sector peers. The last close price of HK$92.0 highlights just how much optimism is priced in, given the company’s recent move into profitability.

The price-to-earnings (P/E) ratio gauges how much investors are willing to pay today for a company's earnings. In biotech, a high P/E may signal strong expectations around breakthrough drugs, pipeline success, or aggressive growth projections. However, the market’s current multiple suggests expectations are much higher than standard industry levels.

Relative to the Asian Biotechs industry average P/E of 38.9x and peer average of 44.8x, Innovent’s 127.1x ratio stands out as extremely high. Our analysis puts its fair P/E ratio at 35.2x, a level the market could move toward if sentiment changes.

Explore the SWS fair ratio for Innovent Biologics

Result: Price-to-Earnings of 127.1x (OVERVALUED)

However, risks remain, as profit growth could slow or a setback in clinical trials may dampen investor enthusiasm for Innovent’s lofty valuation.

Find out about the key risks to this Innovent Biologics narrative.

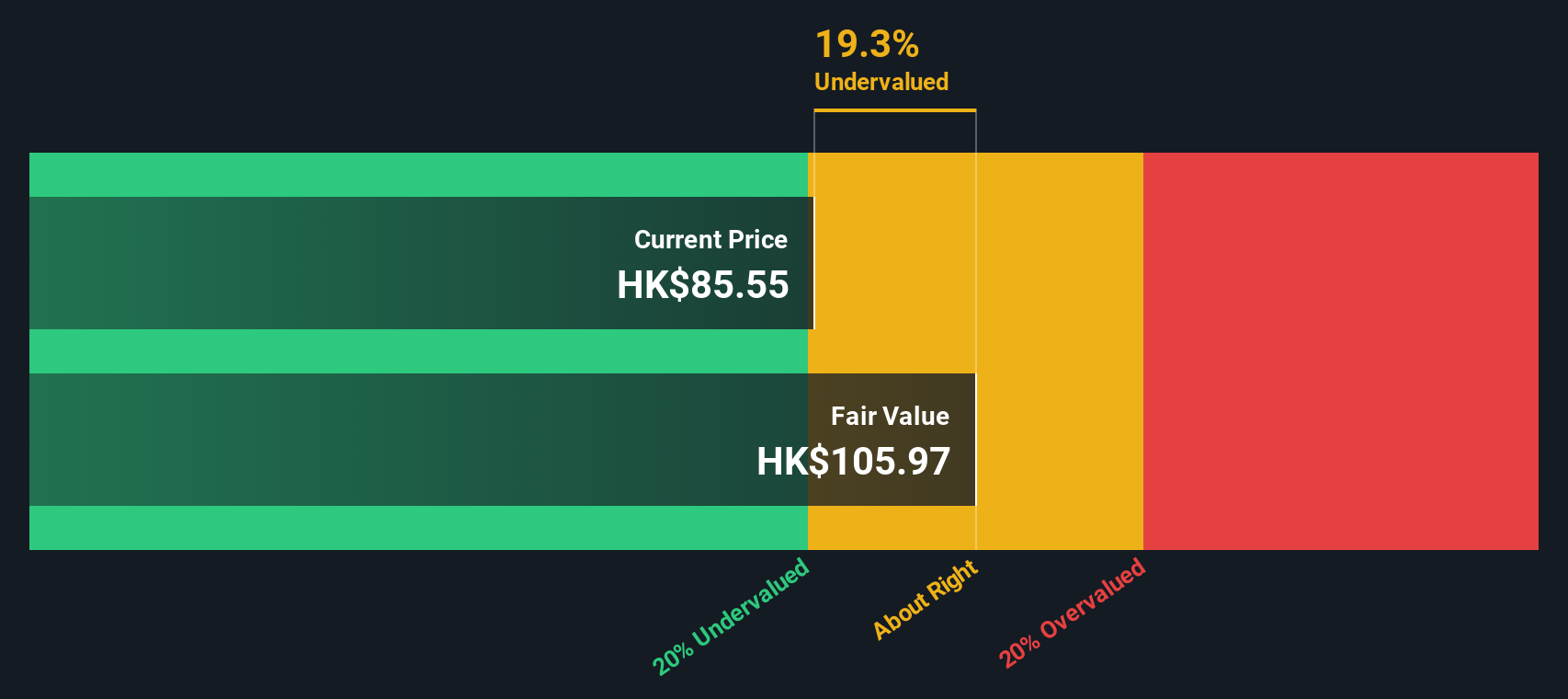

Another View: Discounted Cash Flow Model Offers a Different Perspective

While the current share price appears expensive on earnings multiples, our DCF model points to a different possibility. The SWS DCF model estimates Innovent Biologics' fair value at HK$123.16, which is about 25 percent higher than the current price. Could the company in fact be undervalued instead?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Innovent Biologics for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 917 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Innovent Biologics Narrative

If you have a different view on Innovent Biologics, or enjoy digging into the numbers yourself, you can easily put together your own interpretation in just a few minutes. Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Innovent Biologics.

Looking for more investment ideas?

Give yourself a real edge on your next investment by tapping into fresh opportunities you might not have seen yet. Remember, missing out now could mean passing up your next portfolio win.

- Capitalize on tech trends today by checking out these 26 AI penny stocks which are set to transform artificial intelligence, automation, and data analytics in the coming decade.

- Secure reliable potential income as you review these 15 dividend stocks with yields > 3% that offer attractive yields over 3 percent, perfect for boosting your returns.

- Seize your chance for growth with these 917 undervalued stocks based on cash flows that may be flying under the radar based on their cash flows and fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1801

Innovent Biologics

A biopharmaceutical company, engages in the research and development of antibody and protein medicine products in the People’s Republic of China, the United States, and internationally.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor