Advertisement

Does China 33 Media Group Limited (HKG:8087) Need To Issue More Shares?

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

As the HK$98m market cap China 33 Media Group Limited (HKG:8087) released another year of negative earnings, investors may be on edge waiting for breakeven. The single most important question to ask when you’re investing in a loss-making company is – will it need to raise cash again, and if so, when? This is because new equity from additional capital raising can thin out the value of current shareholders’ stake in the company. Given that China 33 Media Group is spending more money than it earns, it will need to fund its expenses via external sources of capital. China 33 Media Group may need to come to market again, but the question is, when? Below, I’ve analysed the most recent financial data to help answer this question.

View our latest analysis for China 33 Media Group

What is cash burn?

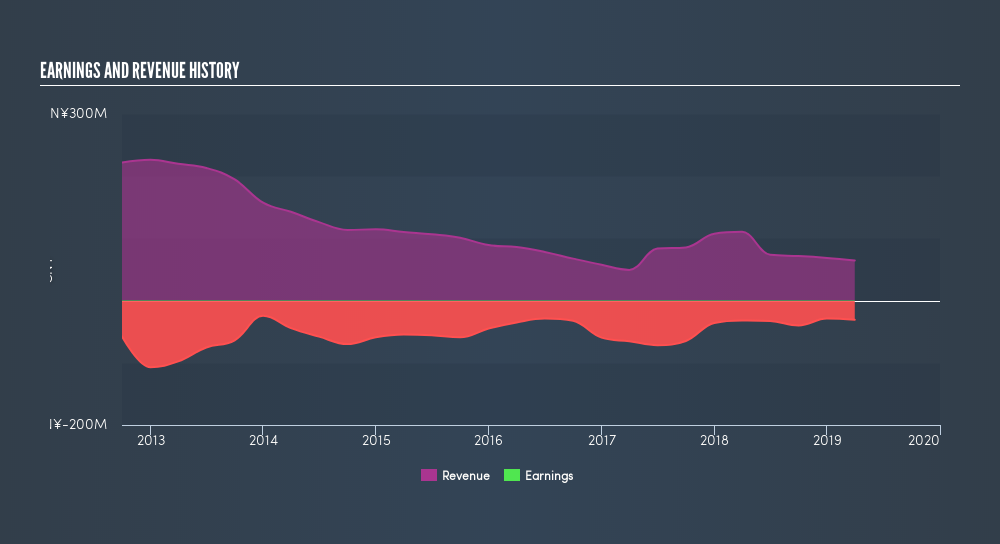

Currently, China 33 Media Group has CN¥35m in cash holdings and producing negative free cash flow of -CN¥3.9m. The riskiest factor facing investors of China 33 Media Group is the potential for the company to run out of cash without the ability to raise more money. China 33 Media Group operates in the publishing industry, which delivered positive earnings in the past year. This means, on average, its industry peers are profitable. China 33 Media Group runs the risk of running down its cash supply too fast, or falling behind its profitable peers by investing too little.

When will China 33 Media Group need to raise more cash?

We can measure China 33 Media Group's ongoing cash expenditure requirements by looking at free cash flow, which I define as cash flow from operations minus fixed capital investment, is a measure of how much cash a company generates/loses each year.

Free cash outflows grew by 90% over the past year, up sharply on the prior year. But according to my analysis, given the current level of cash reserves, China 33 Media Group can continue to spend at the current rate and should not need to raise further capital for a few years. Even though this is analysis is fairly basic, and China 33 Media Group still can cut its overhead in the near future, or borrow money instead of raising new equity capital, this analysis still gives us an idea of the company’s timeline and when things will have to start changing, since its current operation is unsustainable.

Next Steps:

Although China 33 Media Group’s cash burn is growing at a double-digit rate, investors can breathe easy knowing it probably won’t be raising money any time soon. Shareholders may be pleased to know this as it signals that the company still has a strong cash reserve, as well as less likelihood of share dilution from new capital raising. Keep in mind that cash burn is only one side of the coin. I recommend also looking at China 33 Media Group’s revenues in order to forecast when the company will become breakeven and start producing profits for shareholders. I admit this is a fairly basic analysis for 8087's financial health. Other important fundamentals need to be considered as well. I recommend you continue to research China 33 Media Group to get a better picture of the company by looking at:- Historical Performance: What has 8087's returns been like over the past? Go into more detail in the past track record analysis and take a look at the free visual representations of our analysis for more clarity.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on China 33 Media Group’s board and the CEO’s back ground.

- Other High-Performing Stocks: If you believe you should cushion your portfolio with something less risky, scroll through our free list of these great stocks here.

NB: Figures in this article are calculated using data from the trailing twelve months from 31 March 2019. This may not be consistent with full year annual report figures. Operating expenses include only SG&A and one-year R&D.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About SEHK:8087

China 33 Media Group

An investment holding company, provides advertising services in Hong Kong and the People’s Republic of China.

Excellent balance sheet slight.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|33.3% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|23.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|8.5% overvalued

DA

Community Contributor