Advertisement

- Hong Kong

- /

- Entertainment

- /

- SEHK:2660

Zengame Technology Holding (HKG:2660) Has A Rock Solid Balance Sheet

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Zengame Technology Holding Limited (HKG:2660) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Zengame Technology Holding

How Much Debt Does Zengame Technology Holding Carry?

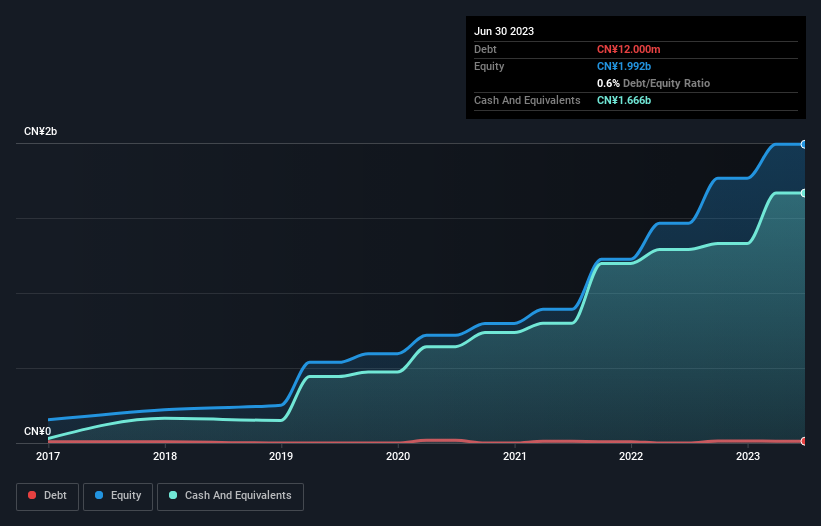

As you can see below, at the end of June 2023, Zengame Technology Holding had CN¥12.0m of debt, up from none a year ago. Click the image for more detail. However, it does have CN¥1.67b in cash offsetting this, leading to net cash of CN¥1.65b.

How Healthy Is Zengame Technology Holding's Balance Sheet?

According to the last reported balance sheet, Zengame Technology Holding had liabilities of CN¥464.5m due within 12 months, and liabilities of CN¥2.21m due beyond 12 months. Offsetting these obligations, it had cash of CN¥1.67b as well as receivables valued at CN¥179.3m due within 12 months. So it can boast CN¥1.38b more liquid assets than total liabilities.

This surplus liquidity suggests that Zengame Technology Holding's balance sheet could take a hit just as well as Homer Simpson's head can take a punch. Having regard to this fact, we think its balance sheet is as strong as an ox. Simply put, the fact that Zengame Technology Holding has more cash than debt is arguably a good indication that it can manage its debt safely.

In addition to that, we're happy to report that Zengame Technology Holding has boosted its EBIT by 43%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Zengame Technology Holding's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Zengame Technology Holding has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last three years, Zengame Technology Holding generated free cash flow amounting to a very robust 83% of its EBIT, more than we'd expect. That positions it well to pay down debt if desirable to do so.

Summing Up

While it is always sensible to investigate a company's debt, in this case Zengame Technology Holding has CN¥1.65b in net cash and a decent-looking balance sheet. And it impressed us with free cash flow of CN¥726m, being 83% of its EBIT. At the end of the day we're not concerned about Zengame Technology Holding's debt. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. We've identified 2 warning signs with Zengame Technology Holding , and understanding them should be part of your investment process.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if Zengame Technology Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2660

Zengame Technology Holding

An investment holding company, develops and operates mobile games primarily in the People’s Republic of China.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|31.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|44.7% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|40.9% undervalued

AG

Community Contributor