Advertisement

- Hong Kong

- /

- Metals and Mining

- /

- SEHK:601

Rare Earth Magnesium Technology Group Holdings (HKG:601) Use Of Debt Could Be Considered Risky

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Rare Earth Magnesium Technology Group Holdings Limited (HKG:601) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Rare Earth Magnesium Technology Group Holdings

What Is Rare Earth Magnesium Technology Group Holdings's Debt?

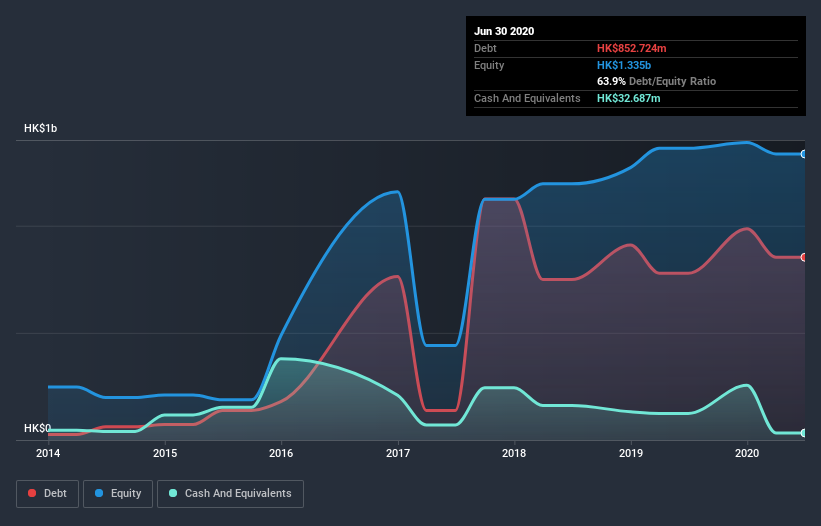

The image below, which you can click on for greater detail, shows that at June 2020 Rare Earth Magnesium Technology Group Holdings had debt of HK$852.7m, up from HK$778.2m in one year. However, it also had HK$32.7m in cash, and so its net debt is HK$820.0m.

A Look At Rare Earth Magnesium Technology Group Holdings's Liabilities

Zooming in on the latest balance sheet data, we can see that Rare Earth Magnesium Technology Group Holdings had liabilities of HK$500.4m due within 12 months and liabilities of HK$546.6m due beyond that. Offsetting this, it had HK$32.7m in cash and HK$196.2m in receivables that were due within 12 months. So it has liabilities totalling HK$818.1m more than its cash and near-term receivables, combined.

When you consider that this deficiency exceeds the company's HK$566.3m market capitalization, you might well be inclined to review the balance sheet intently. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While we wouldn't worry about Rare Earth Magnesium Technology Group Holdings's net debt to EBITDA ratio of 2.9, we think its super-low interest cover of 2.2 times is a sign of high leverage. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. Worse, Rare Earth Magnesium Technology Group Holdings's EBIT was down 50% over the last year. If earnings keep going like that over the long term, it has a snowball's chance in hell of paying off that debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Rare Earth Magnesium Technology Group Holdings's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, Rare Earth Magnesium Technology Group Holdings created free cash flow amounting to 11% of its EBIT, an uninspiring performance. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

On the face of it, Rare Earth Magnesium Technology Group Holdings's level of total liabilities left us tentative about the stock, and its EBIT growth rate was no more enticing than the one empty restaurant on the busiest night of the year. And even its conversion of EBIT to free cash flow fails to inspire much confidence. After considering the datapoints discussed, we think Rare Earth Magnesium Technology Group Holdings has too much debt. While some investors love that sort of risky play, it's certainly not our cup of tea. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. To that end, you should learn about the 4 warning signs we've spotted with Rare Earth Magnesium Technology Group Holdings (including 1 which is doesn't sit too well with us) .

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

When trading Rare Earth Magnesium Technology Group Holdings or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About SEHK:601

Rare Earth Magnesium Technology Group Holdings

An investment holding company, manufactures, trades, and sells magnesium products in Mainland China.

Slight risk and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor