Advertisement

Does Hung Hing Printing Group (HKG:450) Have A Healthy Balance Sheet?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Hung Hing Printing Group Limited (HKG:450) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Hung Hing Printing Group

What Is Hung Hing Printing Group's Net Debt?

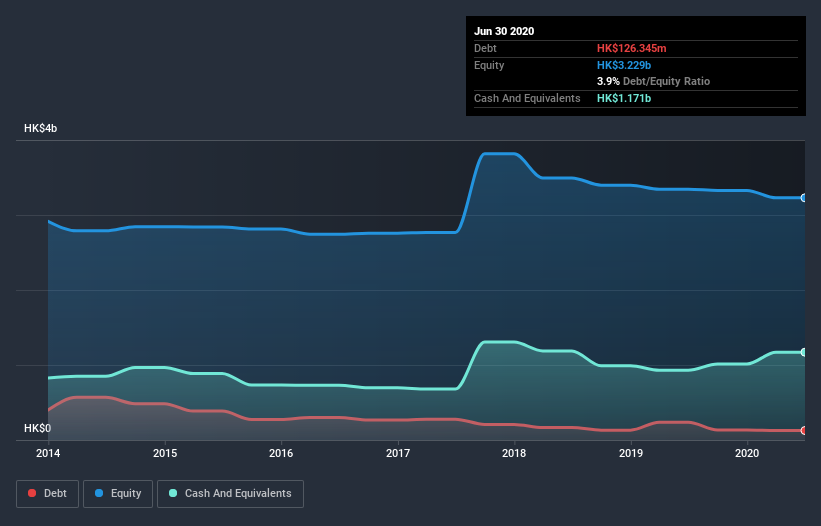

The image below, which you can click on for greater detail, shows that Hung Hing Printing Group had debt of HK$126.3m at the end of June 2020, a reduction from HK$236.7m over a year. But on the other hand it also has HK$1.17b in cash, leading to a HK$1.04b net cash position.

How Healthy Is Hung Hing Printing Group's Balance Sheet?

According to the last reported balance sheet, Hung Hing Printing Group had liabilities of HK$451.0m due within 12 months, and liabilities of HK$189.1m due beyond 12 months. Offsetting these obligations, it had cash of HK$1.17b as well as receivables valued at HK$648.1m due within 12 months. So it can boast HK$1.18b more liquid assets than total liabilities.

This surplus liquidity suggests that Hung Hing Printing Group's balance sheet could take a hit just as well as Homer Simpson's head can take a punch. With this in mind one could posit that its balance sheet is as strong as beautiful a rare rhino. Simply put, the fact that Hung Hing Printing Group has more cash than debt is arguably a good indication that it can manage its debt safely.

It was also good to see that despite losing money on the EBIT line last year, Hung Hing Printing Group turned things around in the last 12 months, delivering and EBIT of HK$41m. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Hung Hing Printing Group will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While Hung Hing Printing Group has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, Hung Hing Printing Group actually produced more free cash flow than EBIT over the last year. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Summing up

While it is always sensible to investigate a company's debt, in this case Hung Hing Printing Group has HK$1.04b in net cash and a strong balance sheet. And it impressed us with free cash flow of HK$250m, being 611% of its EBIT. So is Hung Hing Printing Group's debt a risk? It doesn't seem so to us. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Be aware that Hung Hing Printing Group is showing 2 warning signs in our investment analysis , you should know about...

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

When trading Hung Hing Printing Group or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Hung Hing Printing Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About SEHK:450

Hung Hing Printing Group

An investment holding company, engages in book and package printing, consumer product packaging, corrugated box, and paper trading businesses in the People’s Republic of China, the United States, Hong Kong, the United Kingdom, and internationally.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor