SEHK Growth Companies With High Insider Ownership And Up To 34% Revenue Growth

Reviewed by Simply Wall St

In recent weeks, the Hong Kong market has faced challenges, with the Hang Seng Index experiencing a notable decline amid concerns over U.S. interest rates and local economic pressures. Despite these headwinds, certain growth companies in Hong Kong continue to attract attention due to their robust insider ownership and impressive revenue growth. In times of market volatility, stocks with high insider ownership can be appealing as they often signal confidence from those who know the company best—its leaders and founders. This alignment of interests between shareholders and management is particularly valuable when navigating uncertain economic landscapes.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

| Name | Insider Ownership | Earnings Growth |

| iDreamSky Technology Holdings (SEHK:1119) | 20.1% | 104.1% |

| New Horizon Health (SEHK:6606) | 16.6% | 61% |

| Fenbi (SEHK:2469) | 32.1% | 43% |

| Adicon Holdings (SEHK:9860) | 22.3% | 29.6% |

| DPC Dash (SEHK:1405) | 38.2% | 89.7% |

| Zylox-Tonbridge Medical Technology (SEHK:2190) | 18.5% | 79.3% |

| Tian Tu Capital (SEHK:1973) | 34% | 70.5% |

| Beijing Airdoc Technology (SEHK:2251) | 27.2% | 83.9% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 15.7% | 100.1% |

| Ocumension Therapeutics (SEHK:1477) | 17.7% | 93.7% |

Let's take a closer look at a couple of our picks from the screened companies.

iDreamSky Technology Holdings (SEHK:1119)

Simply Wall St Growth Rating: ★★★★★★

Overview: iDreamSky Technology Holdings Limited is an investment holding company that operates a digital entertainment platform, publishing games through mobile apps and websites in the People’s Republic of China, with a market cap of HK$4.93 billion.

Operations: The company generates CN¥1.92 billion from its Game and Information Services segment, which includes SaaS and other related services.

Insider Ownership: 20.1%

Revenue Growth Forecast: 27.8% p.a.

iDreamSky Technology Holdings, despite a challenging year with sales dropping to CNY 1.92 billion from CNY 2.59 billion and a reduced net loss of CNY 556.35 million, shows promising growth prospects. It's trading at a significant discount of 23.5% below its estimated fair value and is expected to become profitable within three years, with revenue growth forecasted at an impressive rate of 27.8% per year—well above the Hong Kong market average. Insider activities also reflect confidence as there has been more buying than selling in recent months, aligning with strategic expansions like the recent partnership in Saudi Arabia to enhance its gaming sector presence.

- Click here to discover the nuances of iDreamSky Technology Holdings with our detailed analytical future growth report.

- Our valuation report here indicates iDreamSky Technology Holdings may be undervalued.

Dongyue Group (SEHK:189)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Dongyue Group Limited operates as an investment holding company, focusing on the manufacture and distribution of polymers, organic silicone, refrigerants, and other chemical products primarily in the People's Republic of China and internationally, with a market cap of approximately HK$16.998 billion.

Operations: Dongyue Group's revenue is primarily derived from refrigerants (CN¥5.48 billion), organic silicon (CN¥4.86 billion), polymers (CN¥4.55 billion), and dichloromethane PVC along with liquid alkali (CN¥1.21 billion).

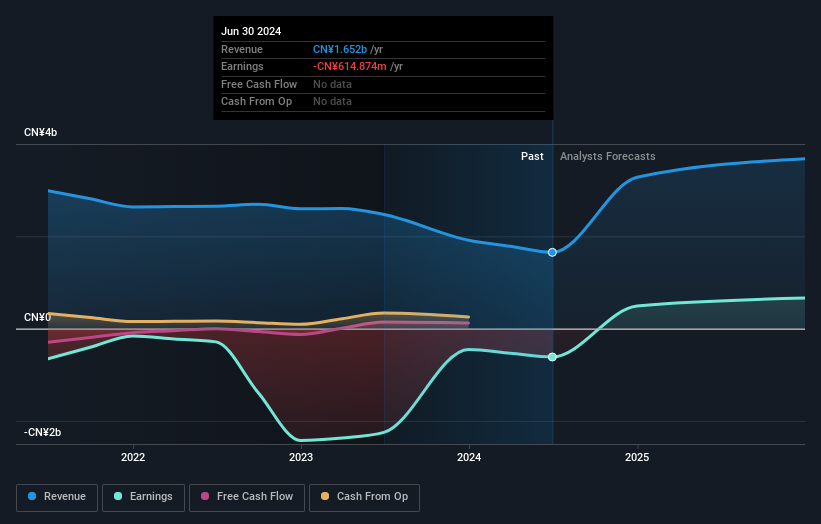

Insider Ownership: 15.4%

Revenue Growth Forecast: 15.4% p.a.

Dongyue Group, with significant insider ownership, faces challenges despite promising growth prospects. The company's earnings are expected to grow by 35.7% annually, outpacing the Hong Kong market's 12% average. However, recent financial performance shows a sharp decline in net income from CNY 3.86 billion to CNY 707.79 million year-over-year due to falling product prices and higher raw material costs. Recent executive changes could signal strategic shifts but also introduce uncertainty about future leadership stability and direction.

- Click here and access our complete growth analysis report to understand the dynamics of Dongyue Group.

- Our expertly prepared valuation report Dongyue Group implies its share price may be too high.

CanSino Biologics (SEHK:6185)

Simply Wall St Growth Rating: ★★★★★☆

Overview: CanSino Biologics Inc. is a company based in the People's Republic of China that focuses on developing, manufacturing, and commercializing vaccines, with a market capitalization of approximately HK$9.22 billion.

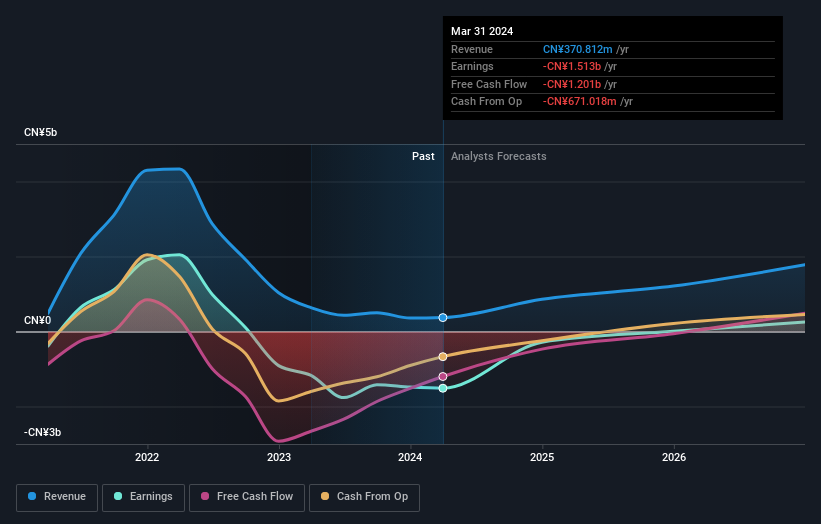

Operations: The company's revenue primarily stems from the research and development of vaccine products for human use, generating CN¥370.81 million.

Insider Ownership: 27.9%

Revenue Growth Forecast: 34.3% p.a.

CanSino Biologics, a Hong Kong-based growth company with high insider ownership, is navigating a challenging financial landscape with a net loss widening to CNY 170.1 million in Q1 2024 from CNY 139.55 million the previous year. Despite this, the company is making significant strides in vaccine development, recently receiving approvals for clinical trials of its Hib and PBPV vaccines, which show promise for broad immunological protection. Revenue grew to CNY 114.28 million, and CanSino's pipeline advancements could enhance its market position if successful commercialization follows.

- Get an in-depth perspective on CanSino Biologics' performance by reading our analyst estimates report here.

- Our comprehensive valuation report raises the possibility that CanSino Biologics is priced higher than what may be justified by its financials.

Turning Ideas Into Actions

- Explore the 52 names from our Fast Growing SEHK Companies With High Insider Ownership screener here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:6185

CanSino Biologics

Develops, manufactures, and commercializes vaccines in the People’s Republic of China.

High growth potential and good value.