Advertisement

- Hong Kong

- /

- Basic Materials

- /

- SEHK:1847

These 4 Measures Indicate That YCIH Green High-Performance Concrete (HKG:1847) Is Using Debt Safely

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that YCIH Green High-Performance Concrete Company Limited (HKG:1847) does use debt in its business. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for YCIH Green High-Performance Concrete

What Is YCIH Green High-Performance Concrete's Debt?

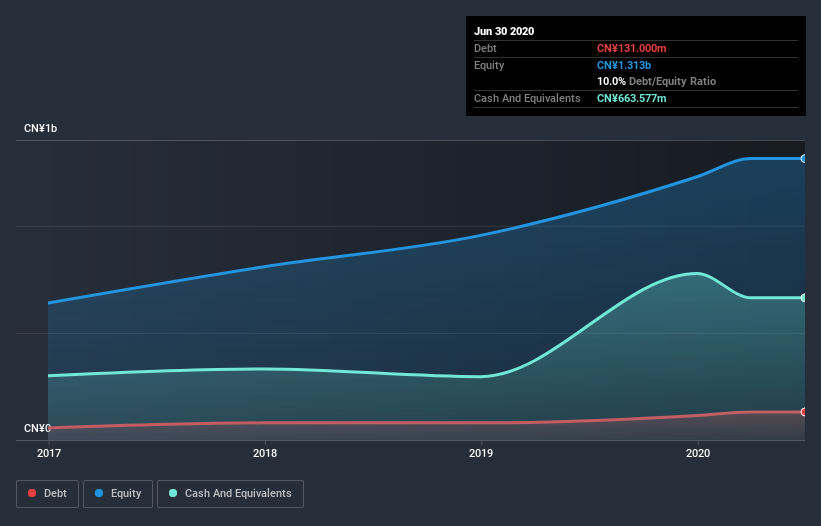

The image below, which you can click on for greater detail, shows that at June 2020 YCIH Green High-Performance Concrete had debt of CN¥131.0m, up from CN¥80.0m in one year. But on the other hand it also has CN¥663.6m in cash, leading to a CN¥532.6m net cash position.

A Look At YCIH Green High-Performance Concrete's Liabilities

We can see from the most recent balance sheet that YCIH Green High-Performance Concrete had liabilities of CN¥2.80b falling due within a year, and liabilities of CN¥20.6m due beyond that. Offsetting these obligations, it had cash of CN¥663.6m as well as receivables valued at CN¥3.16b due within 12 months. So it can boast CN¥997.7m more liquid assets than total liabilities.

This excess liquidity is a great indication that YCIH Green High-Performance Concrete's balance sheet is just as strong as racists are weak. On this basis we think its balance sheet is strong like a sleek panther or even a proud lion. Succinctly put, YCIH Green High-Performance Concrete boasts net cash, so it's fair to say it does not have a heavy debt load!

Also positive, YCIH Green High-Performance Concrete grew its EBIT by 20% in the last year, and that should make it easier to pay down debt, going forward. There's no doubt that we learn most about debt from the balance sheet. But it is YCIH Green High-Performance Concrete's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While YCIH Green High-Performance Concrete has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the most recent three years, YCIH Green High-Performance Concrete recorded free cash flow worth 66% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing up

While we empathize with investors who find debt concerning, the bottom line is that YCIH Green High-Performance Concrete has net cash of CN¥532.6m and plenty of liquid assets. And we liked the look of last year's 20% year-on-year EBIT growth. When it comes to YCIH Green High-Performance Concrete's debt, we sufficiently relaxed that our mind turns to the jacuzzi. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Consider risks, for instance. Every company has them, and we've spotted 2 warning signs for YCIH Green High-Performance Concrete you should know about.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

When trading YCIH Green High-Performance Concrete or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About SEHK:1847

YCIH Green High-Performance Concrete

Operates as a ready-mixed concrete producer in the People's Republic of China.

Mediocre balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor