Advertisement

- Hong Kong

- /

- Medical Equipment

- /

- SEHK:2252

A Look at Shanghai MedBot (SEHK:2252)'s Valuation Following Board Restructuring and New Governance Committees

Simply Wall St

Reviewed by Simply Wall St

Shanghai MicroPort MedBot (Group) (SEHK:2252) held its Extraordinary General Meeting, approving substantial changes in its board structure and announcing new committees focused on strategy, audit, remuneration, and nominations. These actions reflect a clear effort to reinforce leadership and oversight.

See our latest analysis for Shanghai MicroPort MedBot (Group).

The wave of board and governance changes at Shanghai MicroPort MedBot (Group) has arrived alongside remarkable price action. After a strong rally that saw the share price more than double year-to-date, recent momentum has cooled with a 30-day share price decline of 18.06%. Even so, the one-year total shareholder return still stands at 130.77%. Short-term volatility might be causing some investors to take stock, but the long-term trend remains impressive. This suggests the story around growth potential and risk perceptions is still taking shape.

If the company’s rapid transformation has you thinking about what else is possible in the healthcare sector, it’s a good time to explore See the full list for free.

As shares cool off after a meteoric rise and the company unveils sweeping governance reforms, investors must ask whether Shanghai MicroPort MedBot is now trading below its true value or if the market has already factored in all the growth ahead.

Price-to-Book of 39.4x: Is it justified?

Shanghai MicroPort MedBot (Group) is currently trading at a price-to-book ratio of 39.4, considerably higher than its peers and industry benchmarks. The latest close of HK$22.5 reflects the premium being placed on the company, but leaves little room for error if expectations are not met.

The price-to-book ratio measures what investors are willing to pay for each dollar of net assets. In the medical equipment sector, this can signal investor confidence in long-term growth potential, innovation, or brand strength. However, such a high reading often suggests the market anticipates a breakthrough in profitability or future earnings that is not yet reflected in the current financials.

Compared to the Hong Kong Medical Equipment industry average of just 1.6x and a peer group average of 3.1x, Shanghai MicroPort MedBot’s valuation stands out as extremely expensive. Unless future returns and growth assumptions are delivered, this gap may prove difficult to justify.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Book of 39.4x (OVERVALUED)

However, continued net losses and uncertainty in achieving rapid revenue growth could undermine current optimism if market expectations are not met soon.

Find out about the key risks to this Shanghai MicroPort MedBot (Group) narrative.

Another View: What Does the SWS DCF Model Say?

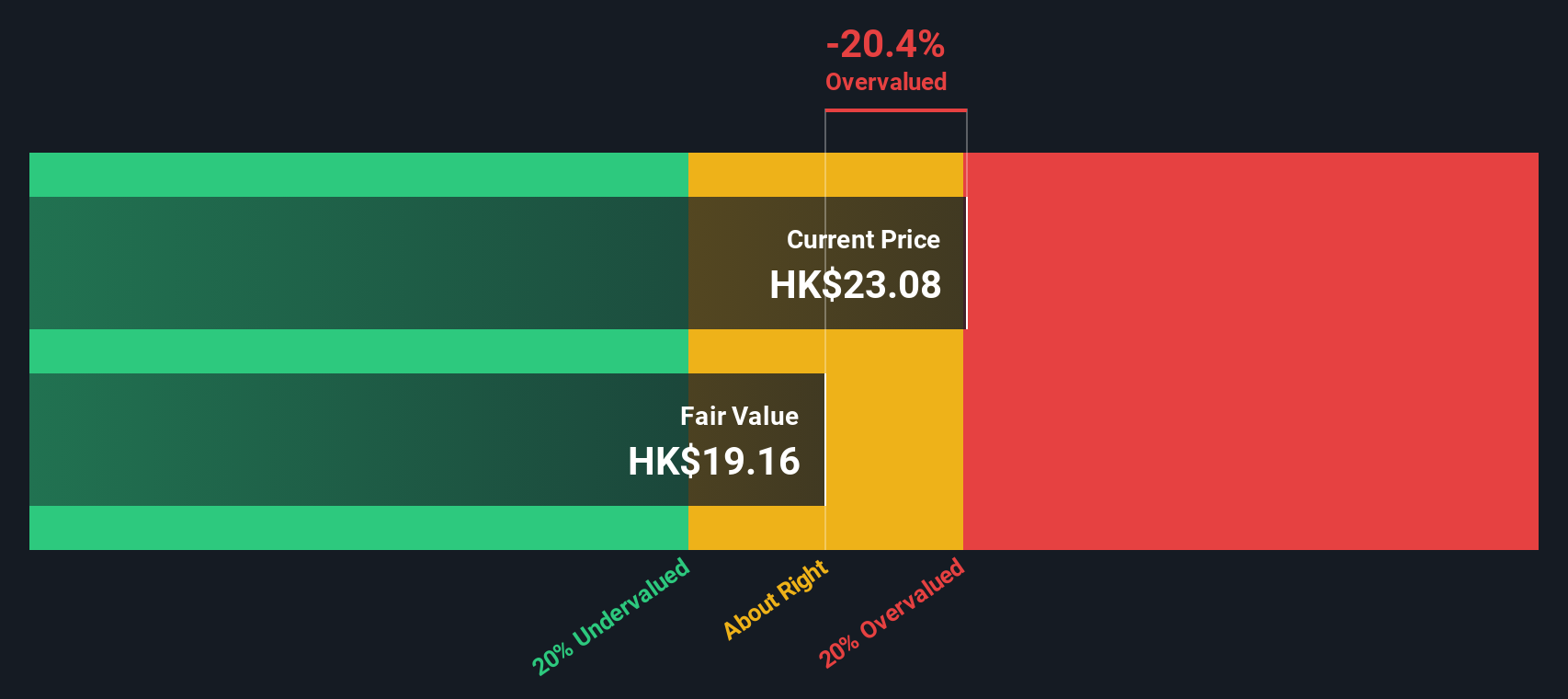

Taking a different approach, our DCF model estimates Shanghai MicroPort MedBot’s fair value at HK$19.15, compared to the current market price of HK$22.5. This suggests the stock may be trading above its intrinsic value. Could the market’s optimism be running ahead of reality, or is there more to the story?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Shanghai MicroPort MedBot (Group) for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 917 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Shanghai MicroPort MedBot (Group) Narrative

If our assessment does not fully align with your view or you would rather take a hands-on approach, it is easy to review the key figures and develop your own perspective in just a few minutes. Do it your way

A great starting point for your Shanghai MicroPort MedBot (Group) research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Stay ahead of the curve and spark your portfolio with unique opportunities using the Simply Wall Street Screener. There is no reason to limit yourself to just one story when so many market winners are waiting to be spotted.

- Uncover high-potential, low-priced stocks by checking out these 3564 penny stocks with strong financials that show strong financial performance and growth potential.

- Capitalize on the AI boom by focusing on innovation leaders through these 25 AI penny stocks that could shape the next tech revolution.

- Make every dollar work smarter by targeting these 917 undervalued stocks based on cash flows to find compelling opportunities overlooked by the market.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:2252

Shanghai MicroPort MedBot (Group)

Shanghai MicroPort MedBot (Group) Co., Ltd.

Exceptional growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

933 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative