Advertisement

- Hong Kong

- /

- Energy Services

- /

- SEHK:1938

Returns On Capital Are Showing Encouraging Signs At Chu Kong Petroleum and Natural Gas Steel Pipe Holdings (HKG:1938)

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. Speaking of which, we noticed some great changes in Chu Kong Petroleum and Natural Gas Steel Pipe Holdings' (HKG:1938) returns on capital, so let's have a look.

Return On Capital Employed (ROCE): What Is It?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on Chu Kong Petroleum and Natural Gas Steel Pipe Holdings is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

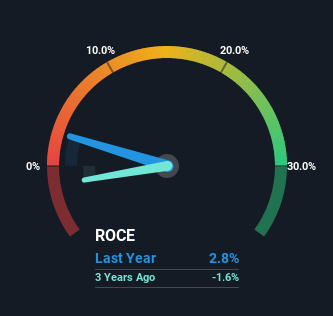

0.028 = CN¥92m ÷ (CN¥7.4b - CN¥4.2b) (Based on the trailing twelve months to June 2022).

Therefore, Chu Kong Petroleum and Natural Gas Steel Pipe Holdings has an ROCE of 2.8%. Ultimately, that's a low return and it under-performs the Energy Services industry average of 7.0%.

See our latest analysis for Chu Kong Petroleum and Natural Gas Steel Pipe Holdings

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating Chu Kong Petroleum and Natural Gas Steel Pipe Holdings' past further, check out this free graph of past earnings, revenue and cash flow.

What The Trend Of ROCE Can Tell Us

We're delighted to see that Chu Kong Petroleum and Natural Gas Steel Pipe Holdings is reaping rewards from its investments and has now broken into profitability. Historically the company was generating losses but as we can see from the latest figures referenced above, they're now earning 2.8% on their capital employed. At first glance, it seems the business is getting more proficient at generating returns, because over the same period, the amount of capital employed has reduced by 35%. Chu Kong Petroleum and Natural Gas Steel Pipe Holdings could be selling under-performing assets since the ROCE is improving.

On a side note, Chu Kong Petroleum and Natural Gas Steel Pipe Holdings' current liabilities are still rather high at 56% of total assets. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

The Key Takeaway

In the end, Chu Kong Petroleum and Natural Gas Steel Pipe Holdings has proven it's capital allocation skills are good with those higher returns from less amount of capital. Although the company may be facing some issues elsewhere since the stock has plunged 85% in the last five years. Still, it's worth doing some further research to see if the trends will continue into the future.

Since virtually every company faces some risks, it's worth knowing what they are, and we've spotted 4 warning signs for Chu Kong Petroleum and Natural Gas Steel Pipe Holdings (of which 1 makes us a bit uncomfortable!) that you should know about.

While Chu Kong Petroleum and Natural Gas Steel Pipe Holdings may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1938

Chu Kong Petroleum and Natural Gas Steel Pipe Holdings

An investment holding company, manufactures and sells longitudinal welded steel pipes in Mainland China, Africa, Europe, the Middle East, rest of Asia, South America, and North America.

Good value with proven track record.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor