- Hong Kong

- /

- Oil and Gas

- /

- SEHK:1138

COSCO SHIPPING Energy Transportation Co., Ltd. (HKG:1138) On An Uptrend: Could Fundamentals Be Driving The Stock?

COSCO SHIPPING Energy Transportation's (HKG:1138) stock is up by 3.9% over the past month. As most would know, long-term fundamentals have a strong correlation with market price movements, so we decided to look at the company's key financial indicators today to determine if they have any role to play in the recent price movement. Specifically, we decided to study COSCO SHIPPING Energy Transportation's ROE in this article.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. Put another way, it reveals the company's success at turning shareholder investments into profits.

View our latest analysis for COSCO SHIPPING Energy Transportation

How Do You Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for COSCO SHIPPING Energy Transportation is:

13% = CN¥4.9b ÷ CN¥37b (Based on the trailing twelve months to September 2023).

The 'return' is the profit over the last twelve months. So, this means that for every HK$1 of its shareholder's investments, the company generates a profit of HK$0.13.

Why Is ROE Important For Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

A Side By Side comparison of COSCO SHIPPING Energy Transportation's Earnings Growth And 13% ROE

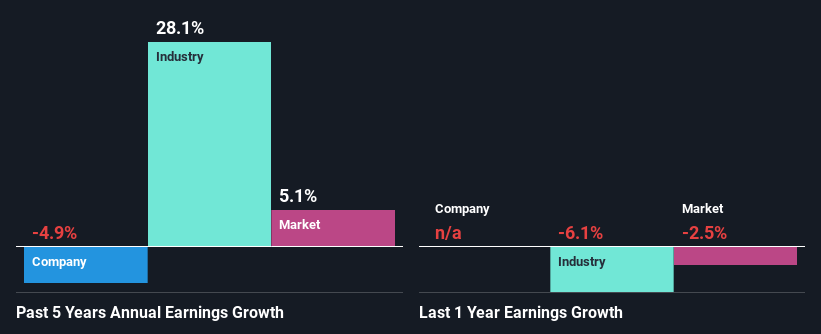

To begin with, COSCO SHIPPING Energy Transportation seems to have a respectable ROE. And on comparing with the industry, we found that the the average industry ROE is similar at 11%. For this reason, COSCO SHIPPING Energy Transportation's five year net income decline of 4.9% raises the question as to why the decent ROE didn't translate into growth. Based on this, we feel that there might be other reasons which haven't been discussed so far in this article that could be hampering the company's growth. Such as, the company pays out a huge portion of its earnings as dividends, or is faced with competitive pressures.

So, as a next step, we compared COSCO SHIPPING Energy Transportation's performance against the industry and were disappointed to discover that while the company has been shrinking its earnings, the industry has been growing its earnings at a rate of 28% over the last few years.

Earnings growth is a huge factor in stock valuation. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. Doing so will help them establish if the stock's future looks promising or ominous. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if COSCO SHIPPING Energy Transportation is trading on a high P/E or a low P/E, relative to its industry.

Is COSCO SHIPPING Energy Transportation Making Efficient Use Of Its Profits?

Looking at its three-year median payout ratio of 28% (or a retention ratio of 72%) which is pretty normal, COSCO SHIPPING Energy Transportation's declining earnings is rather baffling as one would expect to see a fair bit of growth when a company is retaining a good portion of its profits. It looks like there might be some other reasons to explain the lack in that respect. For example, the business could be in decline.

Additionally, COSCO SHIPPING Energy Transportation has paid dividends over a period of eight years, which means that the company's management is rather focused on keeping up its dividend payments, regardless of the shrinking earnings. Upon studying the latest analysts' consensus data, we found that the company is expected to keep paying out approximately 29% of its profits over the next three years. Regardless, the future ROE for COSCO SHIPPING Energy Transportation is predicted to rise to 19% despite there being not much change expected in its payout ratio.

Summary

On the whole, we do feel that COSCO SHIPPING Energy Transportation has some positive attributes. Although, we are disappointed to see a lack of growth in earnings even in spite of a high ROE and and a high reinvestment rate. We believe that there might be some outside factors that could be having a negative impact on the business. That being so, the latest industry analyst forecasts show that the analysts are expecting to see a huge improvement in the company's earnings growth rate. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1138

COSCO SHIPPING Energy Transportation

An investment holding company, engages in the shipment of oil, liquefied natural gas (LNG), and chemicals along the coast of the People’s Republic of China and internationally.

Solid track record and good value.