- Hong Kong

- /

- Real Estate

- /

- SEHK:1516

3 SEHK Stocks That Might Be Undervalued By Up To 26.4%

Reviewed by Simply Wall St

The Hong Kong market has shown resilience amid global economic uncertainties, with the Hang Seng Index gaining 0.85% recently despite broader concerns about deflationary pressures in China. This creates a potentially fertile ground for investors seeking undervalued stocks that could offer significant upside. In such a volatile environment, identifying stocks that are trading below their intrinsic value can be particularly rewarding. Here, we explore three SEHK stocks that might be undervalued by up to 26.4%, offering potential opportunities for discerning investors.

Top 10 Undervalued Stocks Based On Cash Flows In Hong Kong

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Best Pacific International Holdings (SEHK:2111) | HK$2.19 | HK$4.33 | 49.5% |

| Bosideng International Holdings (SEHK:3998) | HK$3.94 | HK$6.73 | 41.4% |

| ANTA Sports Products (SEHK:2020) | HK$68.30 | HK$135.30 | 49.5% |

| BYD Electronic (International) (SEHK:285) | HK$29.15 | HK$53.04 | 45% |

| Shanghai INT Medical Instruments (SEHK:1501) | HK$28.55 | HK$55.95 | 49% |

| Pacific Textiles Holdings (SEHK:1382) | HK$1.62 | HK$2.99 | 45.8% |

| WuXi XDC Cayman (SEHK:2268) | HK$19.20 | HK$37.44 | 48.7% |

| iDreamSky Technology Holdings (SEHK:1119) | HK$2.22 | HK$4.19 | 47% |

| Weimob (SEHK:2013) | HK$1.18 | HK$2.17 | 45.5% |

| MicroPort CardioFlow Medtech (SEHK:2160) | HK$0.75 | HK$1.37 | 45.4% |

Here's a peek at a few of the choices from the screener.

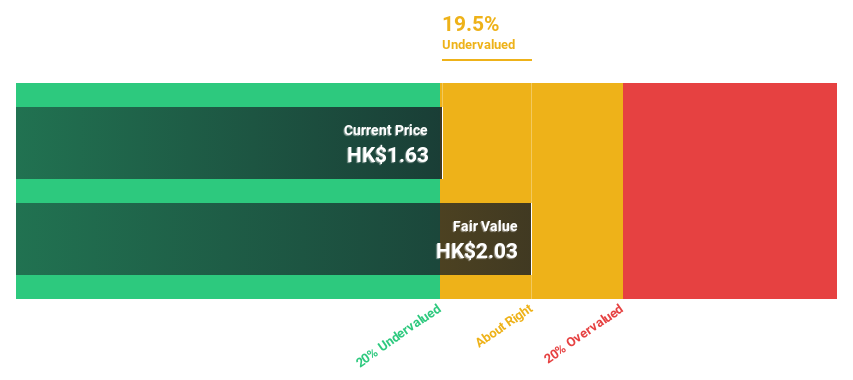

Sunac Services Holdings (SEHK:1516)

Overview: Sunac Services Holdings Limited, with a market cap of HK$5.29 billion, offers property development, cultural tourism city construction and operation, and property management services in the People’s Republic of China.

Operations: The company's revenue segments include Community Living Services (CN¥473.78 million), Value-Added Services to Non-Property Owners (CN¥377.09 million), and Property Management and Operational Services (CN¥6.16 billion).

Estimated Discount To Fair Value: 22.4%

Sunac Services Holdings is trading at HK$1.73, 22.4% below its estimated fair value of HK$2.23, making it potentially undervalued based on cash flows. Despite a dividend yield of 8.98%, the dividend isn't well covered by earnings, raising sustainability concerns. However, earnings are forecast to grow significantly at 60.36% per year and the company is expected to become profitable within three years, outpacing market growth expectations in Hong Kong.

- Our expertly prepared growth report on Sunac Services Holdings implies its future financial outlook may be stronger than recent results.

- Click to explore a detailed breakdown of our findings in Sunac Services Holdings' balance sheet health report.

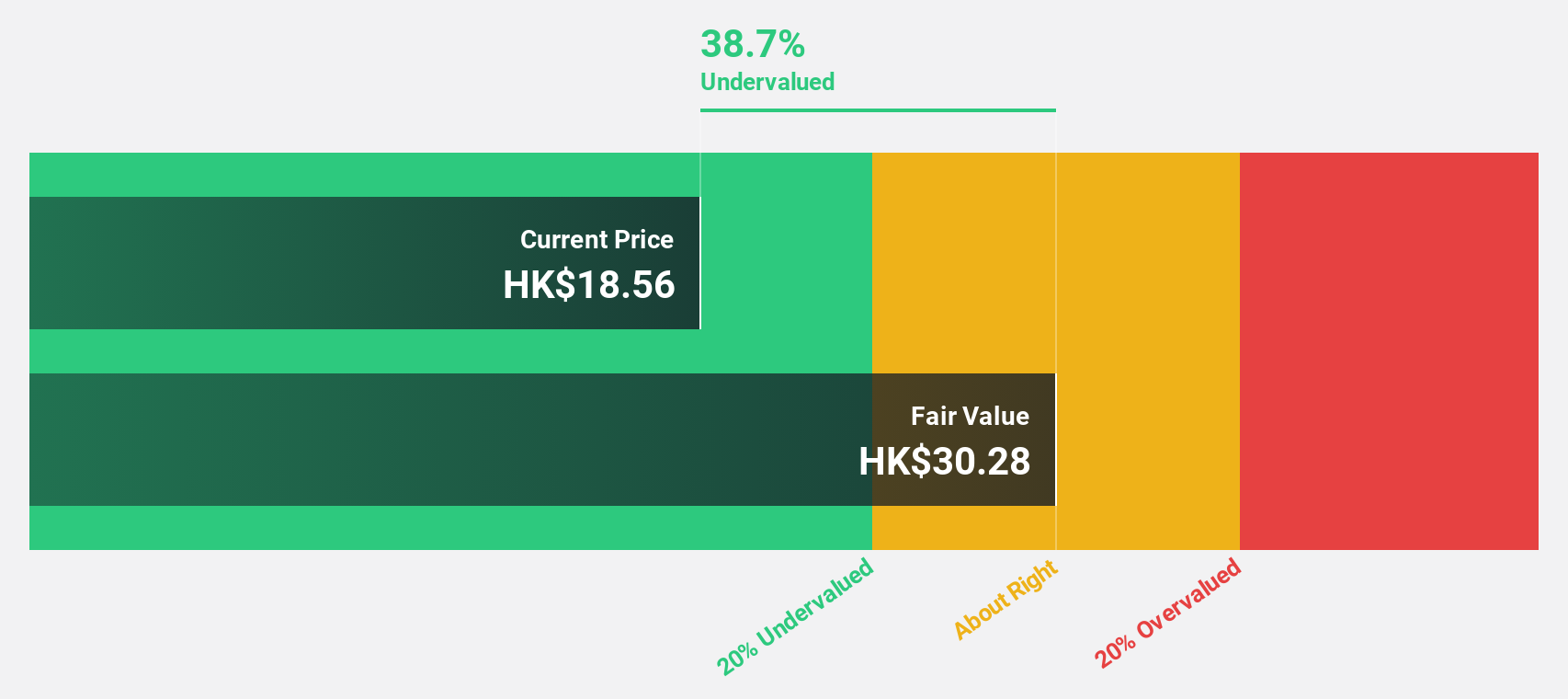

Swire Properties (SEHK:1972)

Overview: Swire Properties Limited, with a market cap of HK$80.15 billion, develops, owns, and operates mixed-use commercial properties in Hong Kong, Mainland China, the United States, and internationally.

Operations: The company's revenue segments include Property Investment (HK$14.39 billion), Hotels (HK$945 million), and Property Trading (HK$119 million).

Estimated Discount To Fair Value: 26.4%

Swire Properties is trading at HK$13.70, 26.4% below its estimated fair value of HK$18.61, indicating it may be undervalued based on cash flows. Despite a dividend yield of 7.66%, the dividend isn't well covered by earnings or free cash flows, raising sustainability concerns. Recent earnings showed a decline in net income to HK$1,796 million from HK$2,223 million year-over-year, impacting profit margins and highlighting the need for careful consideration by investors.

- The analysis detailed in our Swire Properties growth report hints at robust future financial performance.

- Click here to discover the nuances of Swire Properties with our detailed financial health report.

China International Capital (SEHK:3908)

Overview: China International Capital Corporation Limited provides financial services in Mainland China and internationally, with a market cap of HK$105.19 billion.

Operations: The company's revenue segments (in millions of CN¥) are: Investment Banking (3,500), Sales and Trading (4,200), Wealth Management (2,800), Asset Management (1,600).

Estimated Discount To Fair Value: 21.7%

China International Capital Corporation Limited is trading at HK$8.13, 21.7% below its estimated fair value of HK$10.38, suggesting it is undervalued based on cash flows. The company’s earnings are forecast to grow significantly at 20.19% per year over the next three years, outpacing the Hong Kong market's growth rate of 11.3%. Recent announcements include a CNY 3 billion fixed-income offering and a cash dividend distribution of RMB 868 million for its 2023 profits, reflecting solid financial management amidst expected revenue growth challenges.

- Our earnings growth report unveils the potential for significant increases in China International Capital's future results.

- Delve into the full analysis health report here for a deeper understanding of China International Capital.

Key Takeaways

- Discover the full array of 34 Undervalued SEHK Stocks Based On Cash Flows right here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1516

Sunac Services Holdings

An investment holding company, provides property development, cultural tourism city construction and operation, and property management services in the People’s Republic of China.

Flawless balance sheet with reasonable growth potential.