Advertisement

- Hong Kong

- /

- Hospitality

- /

- SEHK:8096

Here's Why We Think Tasty Concepts Holding Limited's (HKG:8096) CEO Compensation Looks Fair

Key Insights

- Tasty Concepts Holding to hold its Annual General Meeting on 20th of September

- Total pay for CEO Chandler Tang includes HK$859.0k salary

- The overall pay is 60% below the industry average

- Tasty Concepts Holding's EPS grew by 58% over the past three years while total shareholder loss over the past three years was 82%

Shareholders may be wondering what CEO Chandler Tang plans to do to improve the less than great performance at Tasty Concepts Holding Limited (HKG:8096) recently. One way they can exercise their influence on management is through voting on resolutions, such as executive remuneration at the next AGM, coming up on 20th of September. It has been shown that setting appropriate executive remuneration incentivises the management to act in the interests of shareholders. We think CEO compensation looks appropriate given the data we have put together.

See our latest analysis for Tasty Concepts Holding

Comparing Tasty Concepts Holding Limited's CEO Compensation With The Industry

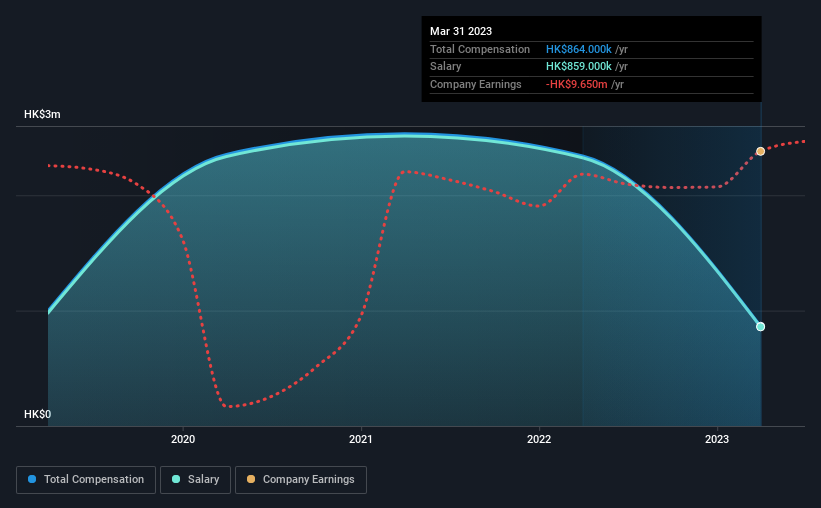

At the time of writing, our data shows that Tasty Concepts Holding Limited has a market capitalization of HK$12m, and reported total annual CEO compensation of HK$864k for the year to March 2023. That's a notable decrease of 63% on last year. We note that the salary portion, which stands at HK$859.0k constitutes the majority of total compensation received by the CEO.

On comparing similar-sized companies in the Hong Kong Hospitality industry with market capitalizations below HK$1.6b, we found that the median total CEO compensation was HK$2.2m. That is to say, Chandler Tang is paid under the industry median.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | HK$859k | HK$2.3m | 99% |

| Other | HK$5.0k | HK$15k | 1% |

| Total Compensation | HK$864k | HK$2.3m | 100% |

On an industry level, around 83% of total compensation represents salary and 17% is other remuneration. Tasty Concepts Holding pays a high salary, concentrating more on this aspect of compensation in comparison to non-salary pay. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at Tasty Concepts Holding Limited's Growth Numbers

Tasty Concepts Holding Limited has seen its earnings per share (EPS) increase by 58% a year over the past three years. In the last year, its revenue is up 23%.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. It's also good to see decent revenue growth in the last year, suggesting the business is healthy and growing. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Tasty Concepts Holding Limited Been A Good Investment?

Few Tasty Concepts Holding Limited shareholders would feel satisfied with the return of -82% over three years. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

Chandler receives almost all of their compensation through a salary. The loss to shareholders over the past three years is certainly concerning. The share price trend has diverged with the robust growth in EPS however, suggesting there may be other factors that could be driving the price performance. A key focus for the board and management will be how to align the share price with fundamentals. In the upcoming AGM, shareholders will get the opportunity to discuss these concerns with the board and assess if the board's plan is likely to improve company performance.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. That's why we did our research, and identified 2 warning signs for Tasty Concepts Holding (of which 1 is concerning!) that you should know about in order to have a holistic understanding of the stock.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

Valuation is complex, but we're here to simplify it.

Discover if Tasty Concepts Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:8096

Tasty Concepts Holding

Engages in the operation of restaurants in Hong Kong and Macau.

Adequate balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor