Advertisement

- Hong Kong

- /

- Hospitality

- /

- SEHK:573

Tao Heung Holdings (HKG:573) Has Debt But No Earnings; Should You Worry?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Tao Heung Holdings Limited (HKG:573) makes use of debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Tao Heung Holdings

What Is Tao Heung Holdings's Debt?

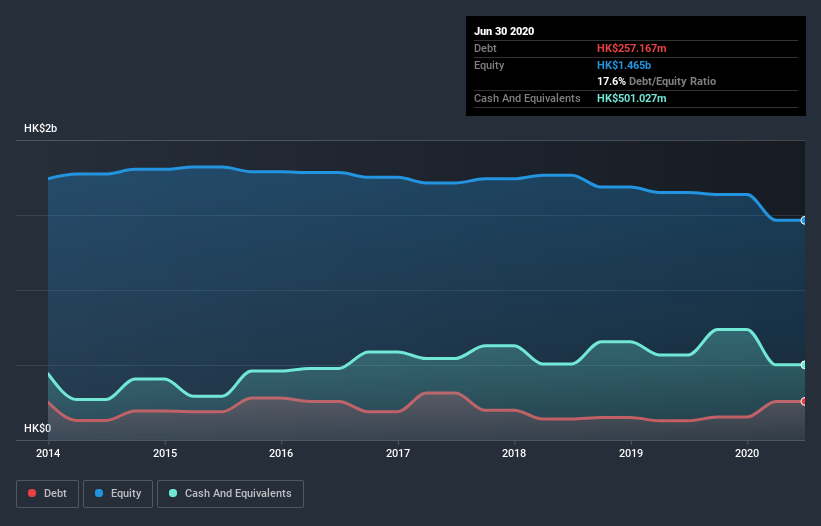

As you can see below, at the end of June 2020, Tao Heung Holdings had HK$257.2m of debt, up from HK$128.7m a year ago. Click the image for more detail. However, it does have HK$501.0m in cash offsetting this, leading to net cash of HK$243.9m.

How Strong Is Tao Heung Holdings's Balance Sheet?

We can see from the most recent balance sheet that Tao Heung Holdings had liabilities of HK$806.1m falling due within a year, and liabilities of HK$564.2m due beyond that. Offsetting this, it had HK$501.0m in cash and HK$50.4m in receivables that were due within 12 months. So it has liabilities totalling HK$818.9m more than its cash and near-term receivables, combined.

This is a mountain of leverage relative to its market capitalization of HK$833.5m. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry. Despite its noteworthy liabilities, Tao Heung Holdings boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Tao Heung Holdings will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, Tao Heung Holdings made a loss at the EBIT level, and saw its revenue drop to HK$3.0b, which is a fall of 26%. That makes us nervous, to say the least.

So How Risky Is Tao Heung Holdings?

While Tao Heung Holdings lost money on an earnings before interest and tax (EBIT) level, it actually generated positive free cash flow HK$225m. So taking that on face value, and considering the net cash situation, we don't think that the stock is too risky in the near term. With revenue growth uninspiring, we'd really need to see some positive EBIT before mustering much enthusiasm for this business. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. To that end, you should be aware of the 1 warning sign we've spotted with Tao Heung Holdings .

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you’re looking to trade Tao Heung Holdings, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Tao Heung Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About SEHK:573

Tao Heung Holdings

An investment holding company, operates a chain of restaurants and bakeries in Hong Kong and Mainland China.

Good value with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor