Stock Analysis

Q Technology Group Leads Three SEHK Stocks Considered Below Estimated Value

Reviewed by Simply Wall St

Amidst a general slowdown in the Hong Kong market, with the Hang Seng Index experiencing a 1.5% decline last week, investors are keenly watching for opportunities that may arise from this downturn. In such times, identifying stocks that are considered undervalued could provide potential avenues for value investment, especially when broader market trends suggest cautious trading behavior.

Top 10 Undervalued Stocks Based On Cash Flows In Hong Kong

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| China Resources Mixc Lifestyle Services (SEHK:1209) | HK$25.65 | HK$48.68 | 47.3% |

| China Cinda Asset Management (SEHK:1359) | HK$0.68 | HK$1.29 | 47.3% |

| Zijin Mining Group (SEHK:2899) | HK$16.92 | HK$31.50 | 46.3% |

| United Energy Group (SEHK:467) | HK$0.315 | HK$0.57 | 44.7% |

| WuXi XDC Cayman (SEHK:2268) | HK$16.20 | HK$31.98 | 49.3% |

| Super Hi International Holding (SEHK:9658) | HK$13.96 | HK$26.09 | 46.5% |

| Genscript Biotech (SEHK:1548) | HK$8.85 | HK$15.99 | 44.6% |

| Vobile Group (SEHK:3738) | HK$1.18 | HK$2.32 | 49.2% |

| Melco International Development (SEHK:200) | HK$5.37 | HK$10.40 | 48.4% |

| Zylox-Tonbridge Medical Technology (SEHK:2190) | HK$10.86 | HK$21.67 | 49.9% |

Below we spotlight a couple of our favorites from our exclusive screener

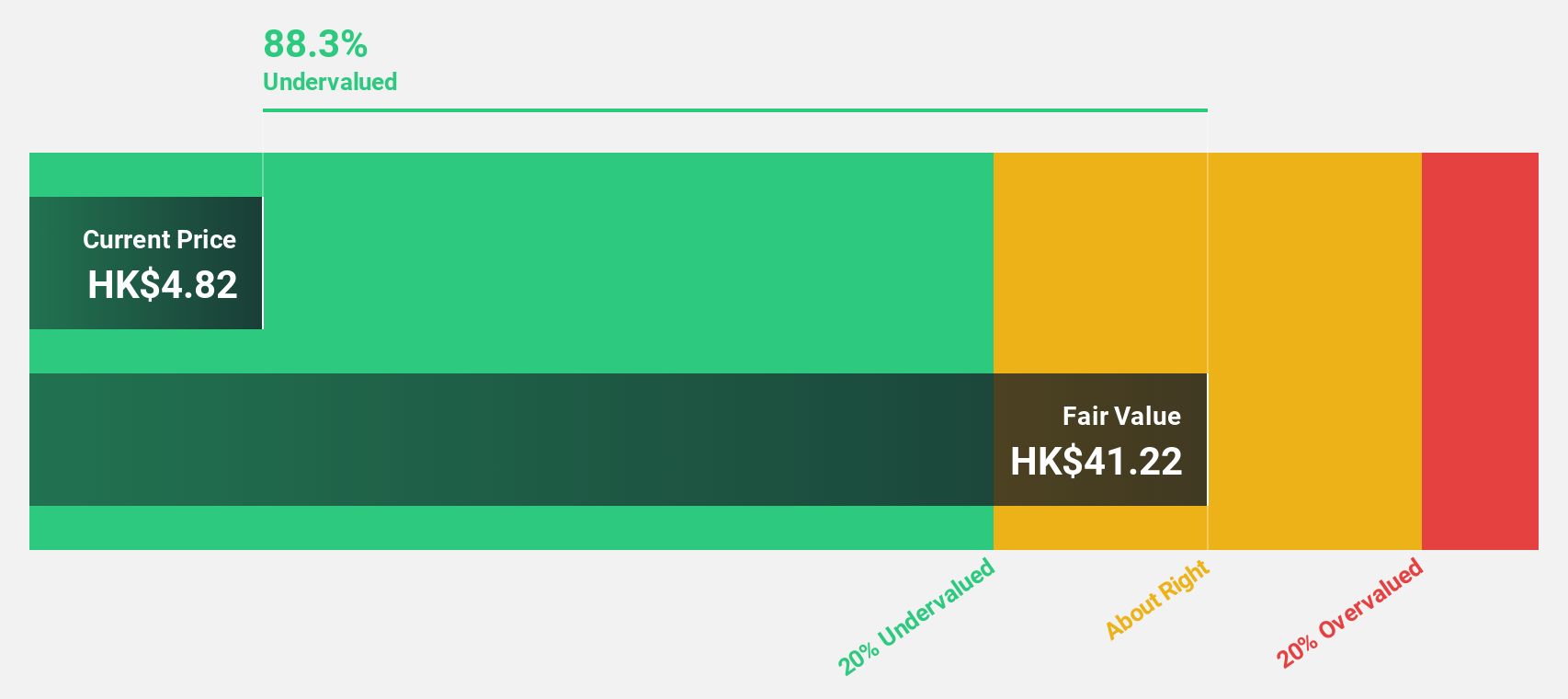

Q Technology (Group) (SEHK:1478)

Overview: Q Technology (Group) Company Limited is an investment holding company specializing in the design, research and development, manufacturing, and sale of camera and fingerprint recognition modules across Mainland China, Hong Kong, India, and other international markets, with a market capitalization of approximately HK$4.87 billion.

Operations: The company generates revenue primarily through the sale of camera modules and fingerprint recognition modules, totaling CN¥11.57 billion and CN¥0.78 billion respectively.

Estimated Discount To Fair Value: 44.3%

Q Technology (Group) is currently trading at HK$4.11, significantly below the estimated fair value of HK$7.38, indicating a substantial undervaluation based on cash flows. Despite this, challenges persist with a slight decline in profit margins year-over-year and low forecasted Return on Equity at 8.8%. However, the company's earnings are expected to grow by 33% annually over the next three years, outpacing both its revenue growth and the broader Hong Kong market's growth rates. Recent sales data show robust volume in camera and fingerprint recognition modules, underscoring strong operational activities.

- According our earnings growth report, there's an indication that Q Technology (Group) might be ready to expand.

- Click here to discover the nuances of Q Technology (Group) with our detailed financial health report.

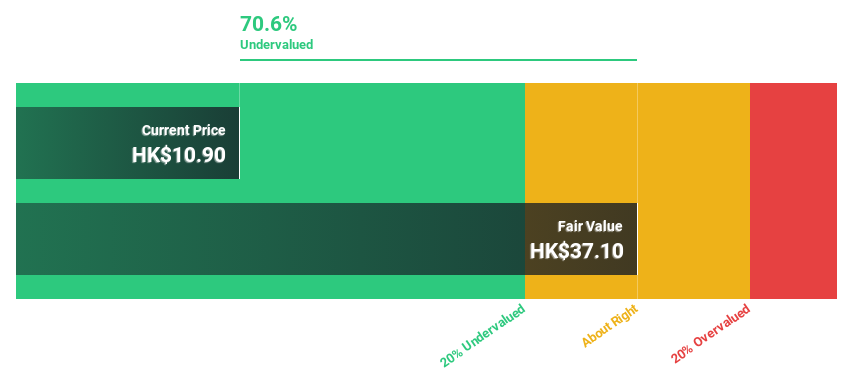

Melco International Development (SEHK:200)

Overview: Melco International Development Limited is an investment holding company operating in the leisure and entertainment sectors in Macau, the Philippines, and Cyprus, with a market capitalization of approximately HK$8.12 billion.

Operations: The company generates revenue primarily from its casino and hospitality segment, amounting to HK$29.55 billion.

Estimated Discount To Fair Value: 48.4%

Melco International Development is currently priced at HK$5.37, well below the calculated fair value of HK$10.4, reflecting a significant undervaluation based on discounted cash flows. The company's revenue growth rate at 11.7% annually is projected to surpass the Hong Kong market average of 7.7%. Additionally, earnings are expected to increase by a very large margin annually over the next three years, with an anticipated high Return on Equity of 34.8% in three years' time.

- Our growth report here indicates Melco International Development may be poised for an improving outlook.

- Click here and access our complete balance sheet health report to understand the dynamics of Melco International Development.

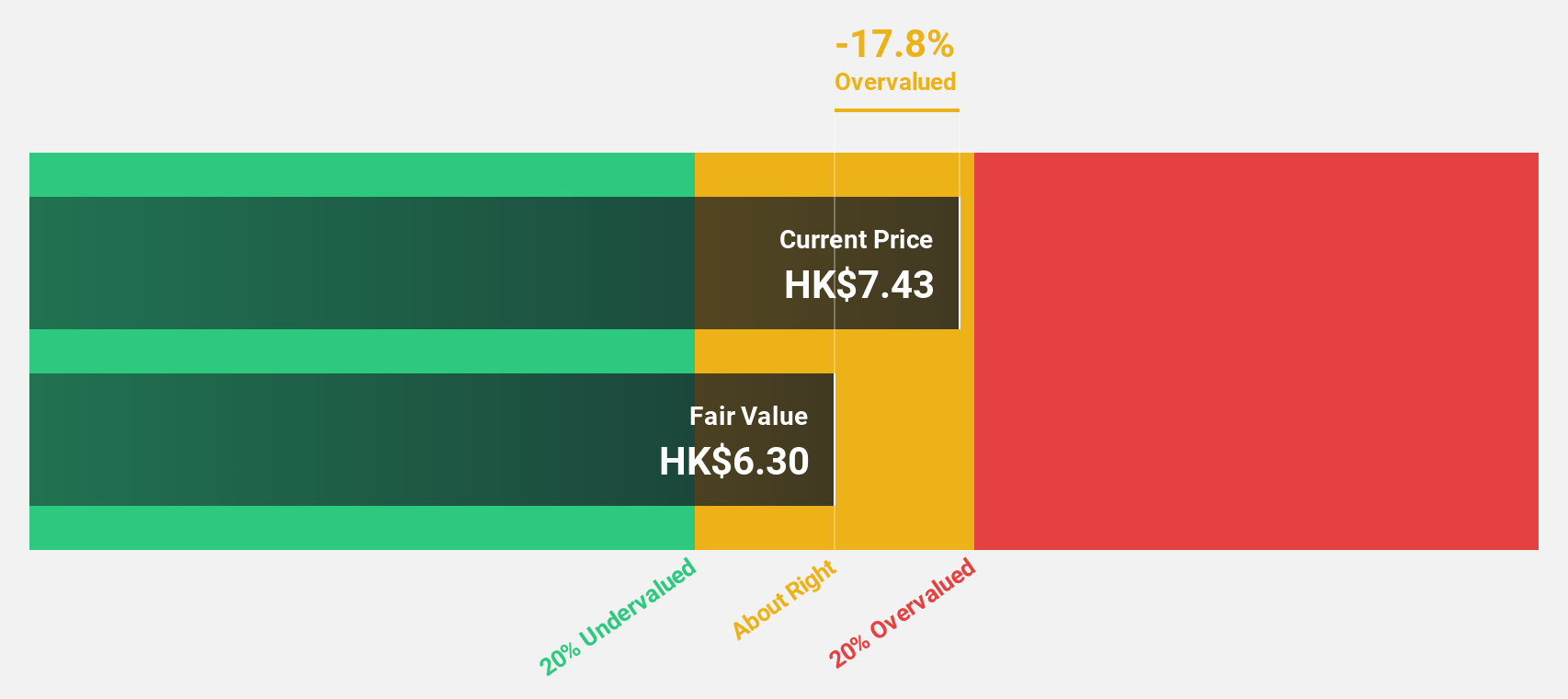

Kingdee International Software Group (SEHK:268)

Overview: Kingdee International Software Group Company Limited operates primarily in the enterprise resource planning sector and has a market capitalization of approximately HK$27.07 billion.

Operations: The company's revenue is generated primarily from two segments: Cloud Service Business, which contributes CN¥4.50 billion, and ERP Business and Others at CN¥1.17 billion.

Estimated Discount To Fair Value: 13.5%

Kingdee International Software Group, trading at HK$7.55, is perceived as undervalued with its price 13.5% below the estimated fair value of HK$8.73 based on discounted cash flows. Recent share repurchases could enhance shareholder value by potentially increasing earnings per share and net asset value. Despite a revenue growth forecast slower than the market at 14.3% annually compared to the market's 20%, earnings are expected to grow significantly by 46.54% annually over the next three years, although its future Return on Equity is projected to be low at 6.2%.

- Our expertly prepared growth report on Kingdee International Software Group implies its future financial outlook may be stronger than recent results.

- Get an in-depth perspective on Kingdee International Software Group's balance sheet by reading our health report here.

Taking Advantage

- Take a closer look at our Undervalued SEHK Stocks Based On Cash Flows list of 42 companies by clicking here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're helping make it simple.

Find out whether Kingdee International Software Group is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:268

Kingdee International Software Group

An investment holding company, engages in the enterprise resource planning business.

Reasonable growth potential with adequate balance sheet.