Advertisement

- Hong Kong

- /

- Hospitality

- /

- SEHK:1928

Sands China (SEHK:1928) Rises Amid Macau Optimism as Hong Kong Market Lags—Is Resilience the Key?

Simply Wall St

Reviewed by Sasha Jovanovic

- Earlier today, Macau casino operators experienced gains while broader Hong Kong equities closed lower and overall trading activity reached an eight-week low.

- This divergence highlights the sector-specific optimism surrounding Macau casinos, with Sands China showing resilience despite subdued market sentiment elsewhere.

- We’ll explore how this renewed optimism for Macau’s casino sector influences Sands China’s investment narrative amid a slower Hong Kong market.

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

What Is Sands China's Investment Narrative?

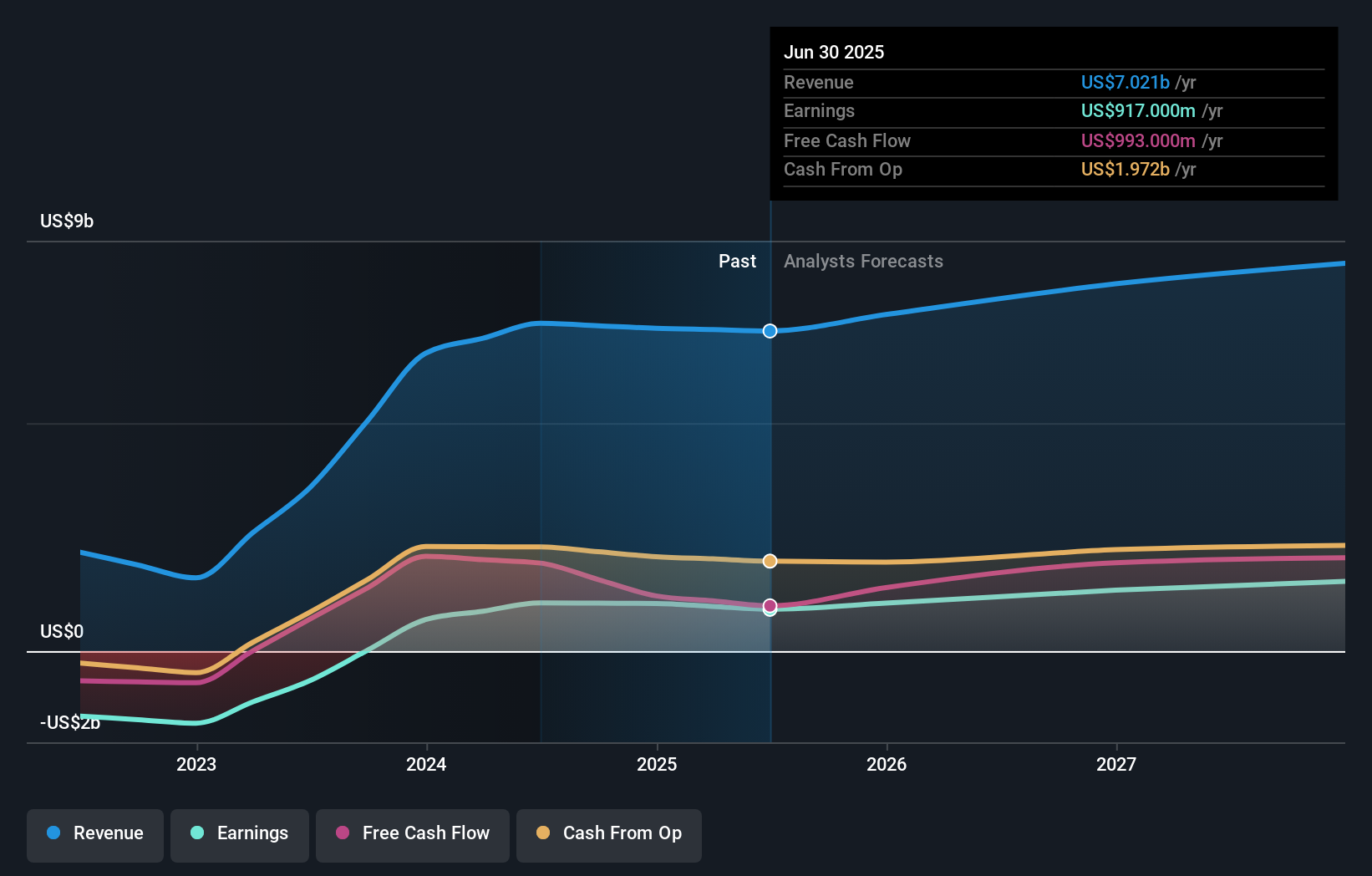

Being a shareholder in Sands China means believing in Macao’s enduring appeal as an international travel and entertainment hub, and in the company’s ability to capture market share among visitors. The recent outperformance of casino operators, including a 2.5% gain in Sands China’s share price despite overall weakness in Hong Kong stocks, reflects short-term optimism linked to visitor demand and sector-specific recovery themes. This sector resilience, however, comes against a backdrop of declining year-over-year earnings, slightly softer revenues, and slower profit growth than the broader Hong Kong market, all of which have been top risks for investors. While the positive price move highlights renewed confidence, it isn’t likely to materially alter the current catalysts, such as further executive changes, partnership expansion, and dividend sustainability, but it does provide a timely reminder of how quickly market sentiment can shift in Macao. On the risk side, investors should remain alert to ongoing high debt levels and premium valuation metrics.

But in contrast to this optimism, high debt levels remain a key risk investors should keep in mind. Sands China's shares have been on the rise but are still potentially undervalued by 31%. Find out what it's worth.Exploring Other Perspectives

Explore 3 other fair value estimates on Sands China - why the stock might be worth just HK$23.72!

Build Your Own Sands China Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Sands China research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Sands China research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Sands China's overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find companies with promising cash flow potential yet trading below their fair value.

- Outshine the giants: these 25 early-stage AI stocks could fund your retirement.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1928

Sands China

Develops, owns, and operates integrated resorts and casinos in Macao.

Moderate growth potential and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

106 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

935 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

142 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative