Advertisement

- Hong Kong

- /

- Food and Staples Retail

- /

- SEHK:1797

We Think Koolearn Technology Holding (HKG:1797) Needs To Drive Business Growth Carefully

Just because a business does not make any money, does not mean that the stock will go down. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. Having said that, unprofitable companies are risky because they could potentially burn through all their cash and become distressed.

So, the natural question for Koolearn Technology Holding (HKG:1797) shareholders is whether they should be concerned by its rate of cash burn. In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. Let's start with an examination of the business' cash, relative to its cash burn.

View our latest analysis for Koolearn Technology Holding

How Long Is Koolearn Technology Holding's Cash Runway?

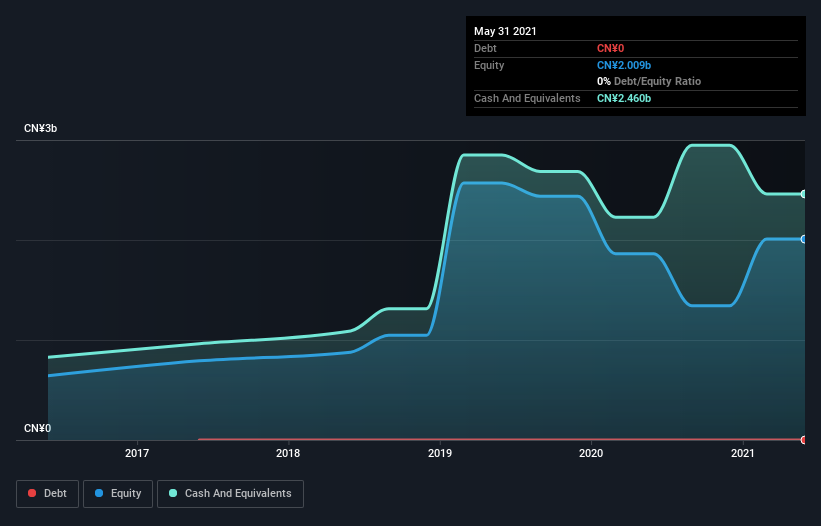

A company's cash runway is calculated by dividing its cash hoard by its cash burn. As at May 2021, Koolearn Technology Holding had cash of CN¥2.5b and no debt. Looking at the last year, the company burnt through CN¥1.0b. So it had a cash runway of about 2.4 years from May 2021. That's decent, giving the company a couple years to develop its business. We should note, however, that if we extrapolate recent trends in its cash burn, then its cash runway would get a lot longer. The image below shows how its cash balance has been changing over the last few years.

How Well Is Koolearn Technology Holding Growing?

Koolearn Technology Holding boosted investment sharply in the last year, with cash burn ramping by 72%. On the bright side, at least operating revenue was up 31% over the same period, giving some cause for hope. On balance, we'd say the company is improving over time. Clearly, however, the crucial factor is whether the company will grow its business going forward. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

How Easily Can Koolearn Technology Holding Raise Cash?

Koolearn Technology Holding seems to be in a fairly good position, in terms of cash burn, but we still think it's worthwhile considering how easily it could raise more money if it wanted to. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. Many companies end up issuing new shares to fund future growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Koolearn Technology Holding's cash burn of CN¥1.0b is about 26% of its CN¥3.9b market capitalisation. That's fairly notable cash burn, so if the company had to sell shares to cover the cost of another year's operations, shareholders would suffer some costly dilution.

So, Should We Worry About Koolearn Technology Holding's Cash Burn?

Even though its increasing cash burn makes us a little nervous, we are compelled to mention that we thought Koolearn Technology Holding's cash runway was relatively promising. Cash burning companies are always on the riskier side of things, but after considering all of the factors discussed in this short piece, we're not too worried about its rate of cash burn. An in-depth examination of risks revealed 3 warning signs for Koolearn Technology Holding that readers should think about before committing capital to this stock.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

Valuation is complex, but we're here to simplify it.

Discover if East Buy Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1797

East Buy Holding

An investment holding company, engages in the livestreaming e-commerce business in the People's Republic of China.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|30.2% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|44.5% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|40.8% undervalued

AG

Community Contributor