Advertisement

3 Growth Companies With High Insider Ownership And Up To 24% Revenue Growth

Simply Wall St

Reviewed by Simply Wall St

As global markets continue to navigate the complexities of rising inflation and interest rate expectations, U.S. stock indexes are climbing toward record highs, with growth stocks outperforming value shares. In this environment, companies that demonstrate robust revenue growth and high insider ownership can be particularly appealing as they often signal strong internal confidence and potential for sustained expansion.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 17.3% | 22.8% |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 50.1% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 26.2% |

| Propel Holdings (TSX:PRL) | 36.5% | 38.7% |

| Pricol (NSEI:PRICOLLTD) | 25.4% | 25.2% |

| On Holding (NYSE:ONON) | 19.1% | 29.7% |

| Kingstone Companies (NasdaqCM:KINS) | 20.8% | 24.9% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 119.4% |

| Fulin Precision (SZSE:300432) | 13.6% | 71% |

| Findi (ASX:FND) | 35.8% | 111.4% |

Let's review some notable picks from our screened stocks.

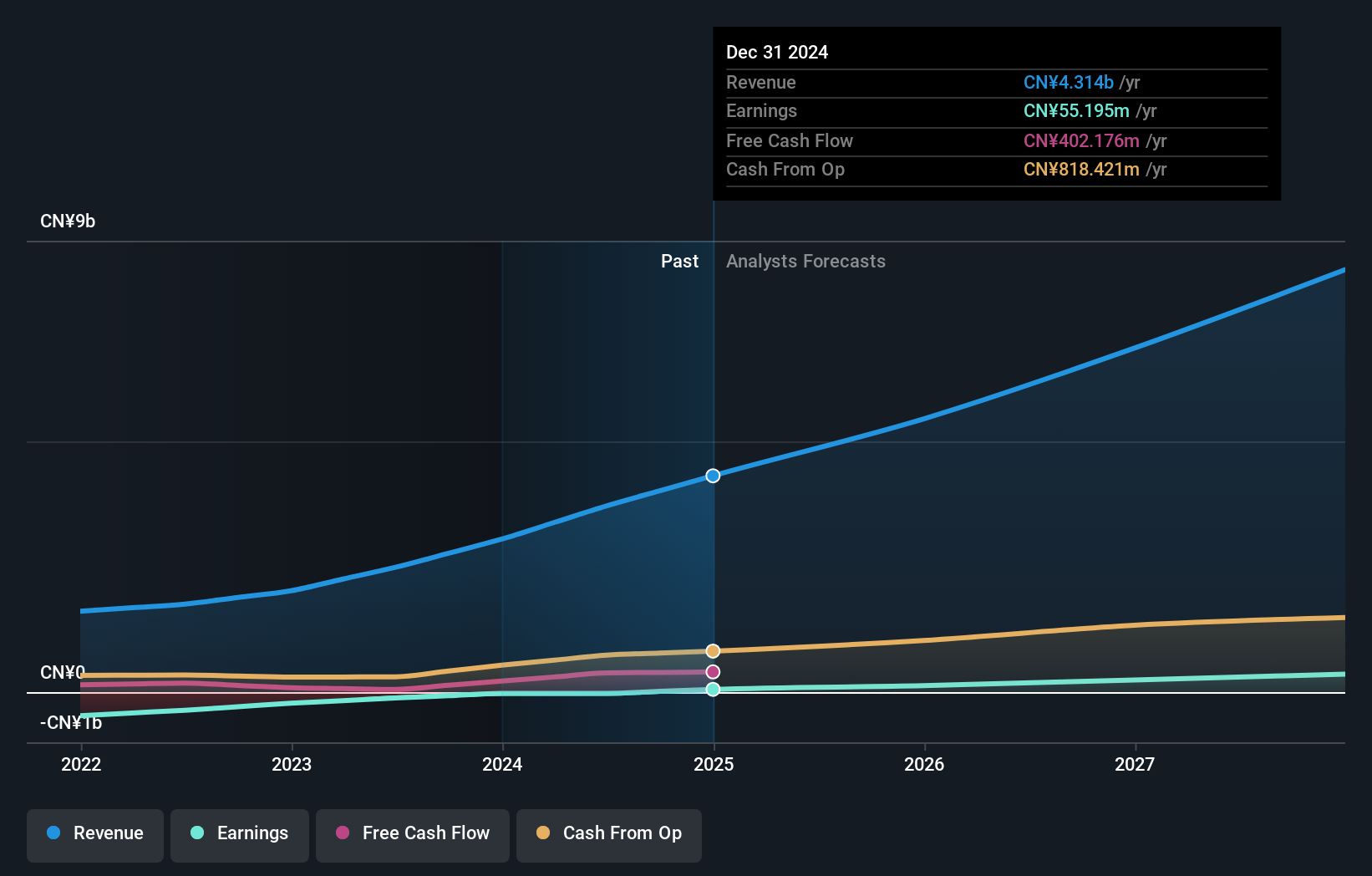

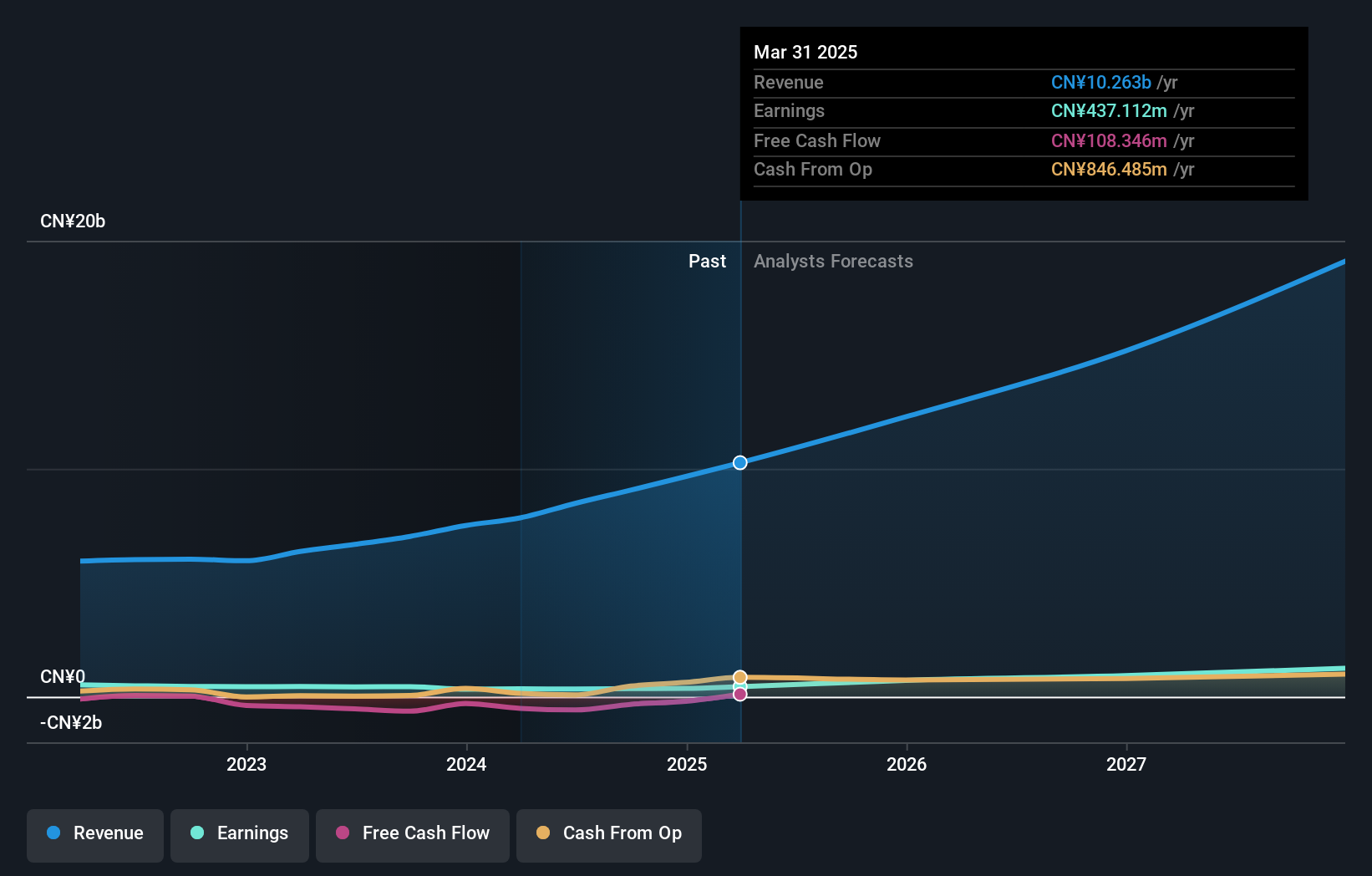

DPC Dash (SEHK:1405)

Simply Wall St Growth Rating: ★★★★★☆

Overview: DPC Dash Ltd operates a chain of fast-food restaurants in the People's Republic of China and has a market cap of HK$10.94 billion.

Operations: The company's revenue is primarily derived from its fast-food restaurant operations in the People’s Republic of China, amounting to CN¥3.72 billion.

Insider Ownership: 38.1%

Revenue Growth Forecast: 24.9% p.a.

DPC Dash is forecast to achieve profitability within three years, with expected revenue growth of 24.9% annually, surpassing the Hong Kong market's average. Despite trading at 28% below estimated fair value, its return on equity is projected to remain low at 8.4%. Recent board changes saw Ms. Bin Yu appointed as an independent non-executive director and chairperson of the Audit and Risk Committee, enhancing governance with her extensive financial expertise.

- Take a closer look at DPC Dash's potential here in our earnings growth report.

- Insights from our recent valuation report point to the potential overvaluation of DPC Dash shares in the market.

Shenzhen H&T Intelligent ControlLtd (SZSE:002402)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shenzhen H&T Intelligent Control Co.Ltd, along with its subsidiaries, engages in the research, development, manufacturing, sales, and marketing of intelligent controller products both in China and internationally; it has a market cap of CN¥18.11 billion.

Operations: Shenzhen H&T Intelligent Control Co.Ltd generates revenue through the research, development, manufacturing, sales, and marketing of intelligent controller products across domestic and international markets.

Insider Ownership: 16.2%

Revenue Growth Forecast: 22.2% p.a.

Shenzhen H&T Intelligent Control Ltd. is expected to see significant earnings growth of 36.9% annually, outpacing the Chinese market average. However, profit margins have declined from 6.3% to 3.9%. Revenue growth is forecast at 22.2%, also above market rates, though return on equity remains low at an estimated 13.8%. The company has completed a share buyback of over CNY100 million, and a shareholder meeting will address stock repurchase and capital changes in January 2025.

- Dive into the specifics of Shenzhen H&T Intelligent ControlLtd here with our thorough growth forecast report.

- According our valuation report, there's an indication that Shenzhen H&T Intelligent ControlLtd's share price might be on the expensive side.

Guangdong Shenling Environmental Systems (SZSE:301018)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Guangdong Shenling Environmental Systems Co., Ltd. (SZSE:301018) operates in the environmental systems industry and has a market cap of CN¥10.16 billion.

Operations: Guangdong Shenling Environmental Systems Co., Ltd. (SZSE:301018) operates in the environmental systems industry with a market cap of CN¥10.16 billion, though specific revenue segments are not provided in the available data.

Insider Ownership: 38.7%

Revenue Growth Forecast: 20.6% p.a.

Guangdong Shenling Environmental Systems is poised for significant growth, with earnings forecast to increase by 39.64% annually, surpassing the Chinese market average. Despite this, profit margins have decreased from 7.1% to 3.8%, and return on equity is projected at a modest 9.7%. Revenue growth is expected at 20.6%, exceeding market rates. Recently, Zhang Yu acquired a 5% stake for approximately CNY320 million, highlighting substantial insider interest in the company’s future prospects.

- Unlock comprehensive insights into our analysis of Guangdong Shenling Environmental Systems stock in this growth report.

- The valuation report we've compiled suggests that Guangdong Shenling Environmental Systems' current price could be inflated.

Key Takeaways

- Click this link to deep-dive into the 1462 companies within our Fast Growing Companies With High Insider Ownership screener.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:301018

Guangdong Shenling Environmental Systems

Guangdong Shenling Environmental Systems Co., Ltd.

High growth potential with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|32.0% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|21.7% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|0.5% overvalued

DA

Community Contributor